Understanding Colorado Bankruptcy Exemptions in Detail

If you're thinking about filing bankruptcy in Colorado, one of the most important building blocks to understand is how Colorado bankruptcy exemptions work. These laws define which types and amounts of property the state treats as protected in a bankruptcy case. In practical terms, exemptions shape how your case is structured, how much value is available to creditors, and how much of your day-to-day life you can preserve while you get a fresh start.

Colorado Bankruptcy Exemptions — At a Glance

- Colorado Uses Its Own System: Colorado has “opted out” of the federal exemption scheme. When you file, you use Colorado bankruptcy exemptions in the Colorado Revised Statutes, plus a few specialized federal protections (like tax-qualified retirement plans).

- Homestead Protection: The bankruptcy homestead exemption Colorado law provides generally protects up to $250,000 of equity in a qualifying primary residence, or $350,000 if the owner, spouse, or a dependent is 60 or older or disabled. Married couples cannot double the homestead cap in a joint case.

- Vehicles and Recreational Vehicles: Most filers can protect up to $15,000 in combined equity in up to two vehicles (or $25,000 if elderly or disabled). Motor homes, travel trailers, and similar RVs are excluded from the standard motor vehicle exemption and may require a homestead or other strategy if they function as a residence.

- Personal Property Baselines: Key personal property caps include about $6,000 in household goods, $2,000 in clothing, $2,500 in jewelry, and $2,000 in books and family pictures per debtor, with many amounts effectively doubled when both spouses have an ownership interest and file together.

- Strong Tools of the Trade Protection:Colorado's tools-of-the-trade exemption can protect up to roughly $60,000 in tools and equipment for your primary occupation and $20,000 for a secondary occupation—crucial for small business owners, tradespeople, and professionals who need to keep working after bankruptcy.

- Retirement and Benefits Safeguards: Most tax-qualified retirement accounts (401(k), 403(b), pensions, IRAs) are strongly protected under a combination of Colorado law and federal bankruptcy law, and many public benefits (Social Security, unemployment) are effectively off-limits to ordinary creditors when properly traced.

- No True Wildcard Exemption: Colorado does not have a general wildcard exemption. Instead, you must match each asset to the most appropriate category—homestead, motor vehicle, tools of the trade, bank accounts, etc.—and build your plan around those targeted bankruptcy exemptions in Colorado.

- Joint Filers: When You Can and Can't Double: Many personal property and vehicle exemptions can be effectively doubled when both spouses are debtors and own an interest in the property. The homestead exemption, by contrast, applies per residence—not per spouse—and cannot be stacked in a typical joint case.

- Appraisals and Accurate Values Matter: When an asset is close to an exemption limit—especially a house or high-value vehicle—a professional appraisal or solid market data is often worth the cost. Trustees are far less likely to successfully challenge a documented, good-faith valuation than a casual guess.

- Attorney Guidance Is Your Best “Exemption Insurance”: The more assets you have, the more important it is to get legal advice before filing. A Colorado bankruptcy attorney can help you apply bankruptcy exemptions Colorado law provides in a way that protects the property that matters most while avoiding avoidable trustee fights.

For example, the bankruptcy homestead exemption Colorado law provides can protect a portion of the equity in your home. For homeowners facing serious financial stress, this protection can be the lifeline that lets you keep a roof over your head while you work through the bankruptcy process.

The rules for bankruptcy exemptions in Colorado are not the same as the federal bankruptcy exemptions. Colorado requires residents to use its own state exemption system, which makes it especially important to understand how Colorado law treats your home, car, wages, retirement accounts, and other property.

Whether you're a Colorado resident just starting to research your options or a professional trying to understand the details of bankruptcy exemptions Colorado law offers, knowing these rules up front can help you plan, reduce stress, and protect as much of your property as possible during a difficult time.

Overview of Colorado Bankruptcy Exemptions

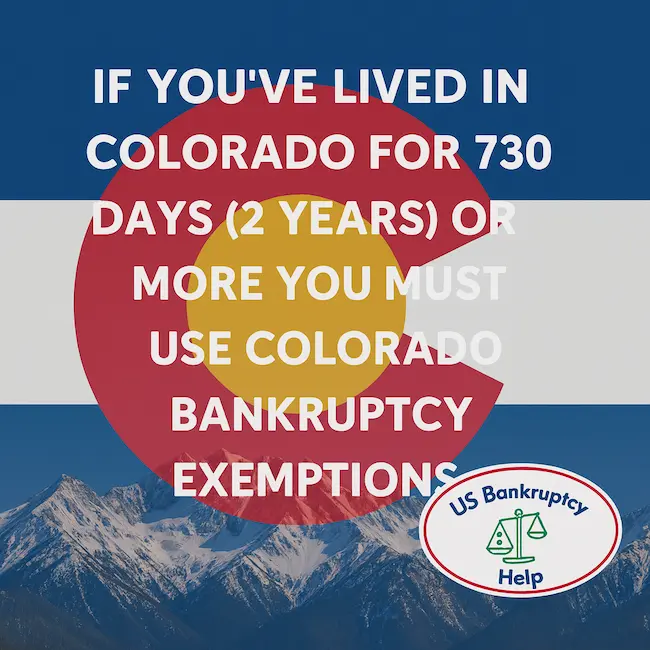

Colorado has opted out of the federal bankruptcy exemption system. Instead, Colorado bankruptcy exemptions come primarily from the Colorado Revised Statutes, including the personal property and wage protections in Title 13, Article 54, and the homestead protections in Title 38, Article 41. These statutes spell out what kinds of property are protected and the dollar limits that apply. If you have been a resident of Colorado for 730 days or more (2 years), you must use Colorado exemptions.

In practical terms, bankruptcy exemptions in Colorado can protect equity in your home, vehicles, household goods, tools you use for work, retirement accounts, and certain benefits and insurance. Each category has its own limits, and some increase if you are older, disabled, or filing jointly with a spouse. The numbers are adjusted from time to time by the Colorado legislature, so it is important to work from current law when planning a case.

Below is a summary of several key bankruptcy exemptions Colorado law provides as of the most recent updates. The table is a starting point only—actual planning should always compare your situation to the current statute language.

| Exemption Category | Colorado State Exemption | Key Statute |

|---|---|---|

| Homestead (Primary Residence) | Colorado's bankruptcy homestead exemption Colorado law protects equity in your principal residence (including many mobile homes and manufactured homes). In general, an individual can protect up to $250,000 in equity, and up to $350,000 if the homeowner, spouse, or a dependent is 60 or older or disabled. Sale proceeds are typically protected for a limited period if they are rolled into a new homestead as required by statute. Homestead amounts cannot be doubled by married couples filing jointly. | Colo. Rev. Stat. § 38-41-201, 2022 Colo. Sess. Laws ch. 86 (HB 22-1137) |

| Motor Vehicle | Colorado protects equity in up to two motor vehicles or bicycles. As of the most recent update, an individual can generally exempt up to $15,000 in combined vehicle equity, increasing to $25,000 if the filer is 60 or older or disabled (or has a qualifying disabled dependent). In a joint filing, many vehicle exemptions can be stacked for jointly owned vehicles. A work vehicle may also qualify under the tools-of-the-trade exemption in some situations. | Colo. Rev. Stat. § 13-54-102(1) |

| Household Goods, Clothing, Jewelry, Books | Colorado's personal property exemptions cover day-to-day belongings. Recent summaries of the statute indicate that an individual may protect up to $6,000 in household goods (furniture, appliances, basic electronics), about $2,000 in clothing, up to $2,500 in jewelry and similar items, and approximately $2,000 in family pictures and books, plus a modest amount of food and fuel. Many of these limits can be doubled in a joint case when both spouses have an ownership interest. | Colo. Rev. Stat. § 13-54-102(1) |

| Tools of the Trade / Work Equipment | If you rely on tools, equipment, or inventory to earn a living, Colorado provides a very robust tools-of-the-trade exemption. Current summaries indicate protection up to approximately $60,000 in tools and equipment used in your primary occupation, and up to $20,000 for tools used in a secondary occupation, with an additional allowance for a professional library. This exemption can be crucial for tradespeople, small business owners, and professionals who need to keep working after bankruptcy. | Colo. Rev. Stat. § 13-54-102(1) |

| Retirement Accounts & Pensions | Most tax-qualified retirement plans and pensions receive very strong protection in Colorado. Many 401(k)s, 403(b)s, traditional and Roth IRAs, and government or public employee pensions are exempt under a combination of Colorado law and federal bankruptcy law, up to the federal caps for IRAs. In most consumer cases, properly structured retirement accounts are fully protected, as long as funds remain in the account. | Colo. Rev. Stat. § 13-54-102(1), 11 U.S.C. § 522(b)(3)(C), (d)(12) |

| Wages & Certain Public Benefits | Colorado limits how much of your paycheck can be garnished and protects a significant portion of your disposable earnings, typically leaving at least 80% of disposable wages exempt in many situations. Social Security benefits, unemployment compensation, and several other public benefits are generally protected by a combination of state and federal law, both inside and outside bankruptcy. | Colo. Rev. Stat. § 13-54-104, 15 U.S.C. §§ 1671–1677 |

| Insurance, Personal Injury & Other Protections | Colorado law and federal law also protect certain insurance-related interests and compensation. Depending on the policy and statute, portions of life insurance cash value, disability benefits, and personal injury recoveries may be exempt, especially when they are meant to support the debtor or dependents. The specifics are very fact-dependent and should be reviewed against the current statute language. | Colo. Rev. Stat. § 13-54-102(1) |

Colorado opts out of the federal bankruptcy exemption scheme. These summaries are meant to give a practical overview of how Colorado bankruptcy exemptions work in real cases. They are not a substitute for reading the current statute or getting legal advice. Because the Colorado legislature periodically adjusts exemption amounts, anyone considering bankruptcy should confirm the latest figures before filing.

The Bankruptcy Homestead Exemption in Colorado

For most homeowners, the bankruptcy homestead exemption Colorado law provides is the single most important part of the exemption system. The homestead exemption is what protects equity in your primary residence when you file bankruptcy. In real life, that often means the difference between keeping your home and having to sell it to pay creditors.

Under current Colorado law, an eligible homeowner can generally protect up to $250,000in equity in a qualifying home. If the owner, the owner's spouse, or a dependent is 60 or older or disabled, the protection increases to $350,000. The homestead can cover a traditional house, a condominium, a mobile home, a manufactured home, or similar property used as your principal residence. In many cases, sale proceeds are also protected for a limited time if they are handled the way the statute requires.

As with other Colorado bankruptcy exemptions, the homestead exemption doesn't erase mortgages or tax liens, and it doesn't guarantee that every homeowner will keep their property in every situation. What it does do is create a powerful shield around a defined amount of home equity so that ordinary unsecured creditors cannot force a sale just to reach that value.

Because this exemption is so important, it's worth slowing down and making sure you and your attorney apply it correctly. Misunderstanding how your equity is calculated—or how ownership and occupancy rules work—can create unpleasant surprises later in a case.

Key aspects of the Colorado homestead exemption include:

| Key Aspect | Details |

|---|---|

| Standard Homestead Protection | The standard bankruptcy homestead exemption Colorado provides generally protects up to $250,000 in equity in a qualifying primary residence, as set out in Colo. Rev. Stat. § 38-41-201(1)(a). |

| Enhanced Protection (Age or Disability) | The enhanced homestead allows protection of up to $350,000in equity if the owner, the owner's spouse, or a dependent is elderly (60 or older) or disabled, under Colo. Rev. Stat. § 38-41-201(1)(b). |

| Types of Homes Covered | Broad coverage applies to many types of homes used as your principal residence, including certain mobile and manufactured homes, as long as they meet the statute's requirements. Mobile and manufactured home homesteads are addressed in Colo. Rev. Stat. § 38-41-201.6. |

Joint Filers Cannot Stack the CO Bankruptcy Homestead Exemption

One important detail for couples to understand is that Colorado treats the homestead as a single protected residence, not as a separate exemption for each spouse. In a typical joint bankruptcy case, spouses do not get to double thebankruptcy homestead exemption Colorado provides. Instead, the same homestead cap applies—up to $250,000 in equity, or up to $350,000 if the age or disability requirements are met—regardless of whether one spouse or both spouses file together.

Understanding how the homestead fits into your overall bankruptcy exemptions in Colorado is vital. A careful review of your property value, mortgage balance, and eligibility for the enhanced homestead can provide a great deal of peace of mind before you file and help you and your lawyer design a strategy that protects as much of your home equity as the law allows.

Personal Property Bankruptcy Exemptions in Colorado

In addition to the homestead exemption, Colorado offers a detailed set of protections for personal property. These Colorado bankruptcy exemptions are what keep everyday items—furniture, clothing, basic electronics, family photos—from being stripped away when you file. For most people, this is what makes a “fresh start” feel livable instead of bare-bones.

The key rules appear in Colorado Revised Statutes section 13-54-102(1). As of the most recent updates, Colorado law allows exemptions for clothing, household goods, jewelry, and family books and pictures at specific dollar limits. Many of these protections apply per debtor, which means some amounts can be doubled in a joint case when both spouses have an ownership interest in the property.

Essential for daily life, these goods range from furniture and small home appliances to heirloom jewelry and family photos. Protecting them helps prevent significant lifestyle disruptions while you work through a bankruptcy case.

| Exemption Category | Colorado Exemption (Individual / Notes) | Key Statute |

|---|---|---|

| Household Goods & Furnishings | Household goods owned and used by the debtor or the debtor's dependents are generally exempt up to $6,000 in value. This category includes common items such as furniture, appliances, dishes, and basic home electronics used in the residence. In a joint case, each spouse may usually claim a separate household goods exemption to the extent they each have an ownership interest. | Colo. Rev. Stat. § 13-54-102(1)(e) |

| Jewelry & Articles of Adornment | Watches, jewelry, and other articles of adornment of the debtor and each dependent are exempt up to $2,500 in value. This is often where engagement rings, wedding bands, and other personal jewelry are listed and valued in a bankruptcy case. | Colo. Rev. Stat. § 13-54-102(1)(b) |

| Books, Family Pictures & Library | The debtor's library, family pictures, and school books for the debtor and dependents are generally exempt up to $2,000in value, so long as the items are not part of the debtor's stock in trade. This is the provision that protects family photo collections, kids' school books, and similar personal items that have relatively modest resale value but significant emotional value. | Colo. Rev. Stat. § 13-54-102(1)(c) |

| Clothing / Wearing Apparel | Necessary wearing apparel for the debtor and each dependent is exempt up to $2,000 in value. This covers ordinary clothing, not luxury fashion inventory or items held primarily for resale. | Colo. Rev. Stat. § 13-54-102(1)(a) |

Preserving personal property is a fundamental piece of any bankruptcy strategy. Accurate valuations, a realistic used-market value, and careful matching of each item to the correct bankruptcy exemptions in Coloradocan make a meaningful difference in how much you keep and how smoothly your case proceeds.

Colorado Motor Vehicle Bankruptcy Exemption

Vehicles often represent a crucial asset for Colorado families. Getting to work, school, medical appointments, and childcare usually depends on having a reliable car. That is why the motor vehicle exemption is such an important part of the overall Colorado bankruptcy exemptions framework.

Under current Colorado law, a debtor can generally protect equity in up to two motor vehicles or bicycles. As of the most recent updates, the standard exemption allows protection of up to $15,000in total vehicle equity. If the debtor, the debtor's spouse, or a dependent is elderly (60 or older) or disabled, the protected amount increases to $25,000. These limits come from Colorado Revised Statutes section 13-54-102(1)(j).

The exemption applies to your equityin the vehicle, not the full market value. Equity is the vehicle's reasonable fair market value minus any loan balance. A leased vehicle typically has no equity to protect, because you do not own the car. Certain recreational vehicles—such as snowmobiles, ATVs, golf carts, boats and other watercraft, travel trailers, tent trailers, and motor homes—are excluded from this particular exemption under Colorado law.

| Exemption Aspect | Details | Key Statute |

|---|---|---|

| Standard Motor Vehicle Protection | Protects equity in up to two motor vehicles or bicycles kept and used by the debtor, up to a combined total of $15,000 in equity. Equity is generally calculated as fair market value minus any auto loan balance. | Colo. Rev. Stat. § 13-54-102(1)(j)(I) |

| Enhanced Protection (Age or Disability) | If the debtor, the debtor's spouse, or a dependent is elderly (60 or older) or disabled, the total protected equity in up to two vehicles or bicycles increases to $25,000. | Colo. Rev. Stat. § 13-54-102(1)(j)(II) |

| Excluded Vehicles | The motor vehicle exemption does not apply to certain recreational or specialty vehicles, including snowmobiles, all-terrain vehicles, golf carts, boats and other watercraft, travel trailers, tent trailers, and motor homes. | Colo. Rev. Stat. § 13-54-102(1)(j)(III) |

Joint Filers and the Colorado Motor Vehicle Exemption

In a joint bankruptcy case, the motor vehicle exemption is generally available to each debtor separately. That means spouses can often protect more total vehicle equity than a single filer, as long as each spouse actually has an ownership interest in the car or cars being claimed. For example, if four vehicles are jointly owned and the combined equity in each spouse's share stays within that spouse's $15,000 (or $25,000) cap, it may be possible to protect all of the equity across those vehicles. What spouses cannot do is stack both exemptions on top of just one person's ownership interest in a vehicle that only one of them owns.

Used thoughtfully, the motor vehicle exemption can allow you to keep reliable transportation while still obtaining a fresh start in bankruptcy. Careful valuation of your vehicles and accurate use of the bankruptcy exemptions in Colorado are essential, especially if you are close to or slightly above the exemption limits.

Colorado Does Not Have a Wildcard Bankruptcy Exemption

Many people ask whether there is a wildcard exemption in Colorado that can be used on any property they choose. Under current Colorado law, there is no true wildcard exemption like the one available under the federal exemption system. Instead, Colorado relies on more targeted Colorado bankruptcy exemptionsfor specific categories such as household goods, vehicles, tools of the trade, and certain financial assets.

In practice, this means Colorado filers need to match each asset to the most appropriate exemption category rather than relying on a single flexible wildcard. With careful planning, many of the items people hope to protect with a wildcard can still be covered under the existing bankruptcy exemptions in Colorado, but it requires a closer look at how each asset is classified.

Money, Public Benefits, Wages, and Insurance Exemptions in Colorado

Colorado law and federal law work together to protect a wide range of monetary assets and benefits in bankruptcy. These Colorado bankruptcy exemptions are designed to keep basic income streams and safety nets in place so that a person can realistically recover after filing.

Many public benefits, such as Social Security and unemployment compensation, are protected by statute and are generally off-limits to ordinary creditors. Colorado also limits how much of your wages can be garnished and provides targeted protections for money in bank accounts, disability benefits, and the cash value of certain life insurance policies. Understanding how these protections fit into your overall bankruptcy exemptions in Colorado is critical when planning a case.

| Category | Colorado / Federal Protection | Key Authority |

|---|---|---|

| Social Security Benefits | Social Security retirement, SSDI, and SSI benefits are generally protected from most creditors under federal law and remain protected in bankruptcy in the vast majority of consumer cases, especially when they can be traced in a bank account. In practice, trustees and creditors usually treat these benefits as fully exempt or excluded from the bankruptcy estate. | 42 U.S.C. § 407; Colo. Rev. Stat. § 13-54-102(1) (cross-references to protected benefits) |

| Unemployment & Certain Public Assistance | Colorado unemployment insurance benefits and many public assistance payments are exempt from levy and execution. As a result, ordinary creditors generally cannot garnish these benefits, and they are typically treated as exempt in bankruptcy, subject to exceptions for things like support obligations or fraud-related overpayments. | Colo. Rev. Stat. § 8-80-103; Colo. Rev. Stat. § 26-2-131; Colo. Rev. Stat. § 13-54-102(1) |

| Wages / Earnings | For most consumer debts, Colorado limits wage garnishment to the lesser of 20% of disposable earnings for a week or the amount by which disposable earnings exceed 40 timesthe federal or state minimum hourly wage, whichever is greater. This means that at least about 80% of a typical worker's disposable earnings are protected from ordinary garnishment, with different (often higher) limits applying to child support, certain fraud-related debts, and tax obligations. | Colo. Rev. Stat. § 13-54-104(2)(a) |

| Money in Bank / Depository Accounts | Colorado provides a specific exemption for funds in depository accounts. A debtor may generally protect up to $2,500cumulative in checking and savings accounts in the debtor's name. In addition, amounts in the same accounts that are separately exempt (for example, Social Security or unemployment benefits) remain protected if they can be reasonably traced, with commingling handled under the statutory tracing rules. | Colo. Rev. Stat. § 13-54-102(1)(w), (6) |

| Life Insurance Cash Value | The cash surrender value of life insurance policies or certificates that have been owned by the debtor for a continuous, unexpired period of at least forty-eight months is exempt up to $250,000, so long as the policy meets the statutory requirements. Increases in cash value from “extraordinary moneys”—amounts paid in above contractual requirements—during the forty-eight months before a writ or execution are notexempt. Proceeds paid to a named beneficiary upon the insured's death are generally exempt as to the insured’s creditors, but may be reachable for the beneficiary's own debts. | Colo. Rev. Stat. § 13-54-102(1)(l) |

| Disability Benefits & Related Protections | Public or private disability benefits are exempt up to $5,000 per month; any amount above that is subject to garnishment under the wage-garnishment rules. Professionally prescribed health aids are fully exempt, and workers' compensation benefits are separately protected under Colorado law. In addition, certain tax refunds tied to earned income tax credits and child tax credits are fully exempt. | Colo. Rev. Stat. § 13-54-102(1)(v), (1)(p), (1)(o); Colo. Rev. Stat. § 8-42-124 |

Taken together, these money, benefit, and insurance protections form a critical safety net. They help ensure that filing bankruptcy does not cut off your basic income sources or wipe out essential financial cushions. Thoughtful use of these exemptions—especially careful tracing of benefits in bank accounts and accurate disclosure of life insurance and disability income—can make a major difference in the outcome of a Colorado bankruptcy case.

Bankruptcy Exemptions Colorado: Retirement Accounts and Pensions

Retirement savings are among the most strongly protected assets in a Colorado bankruptcy case. Both Colorado law and federal bankruptcy law treat properly structured retirement plans as long-term, protected funds. In practical terms, most tax-qualified retirement accounts and pensions are either fully exempt or protected up to very generous limits.

Under Colorado law, property, including funds, held in or payable from a wide range of retirement and pension vehicles is exempt from attachment and execution. Colorado Revised Statutes section 13-54-102(1)(s) protects funds in or payable from pension or retirement plans, deferred compensation plans, and many tax-qualified arrangements, including employer plans governed by federal law and individual accounts like IRAs and Roth IRAs.

On top of that, the Bankruptcy Code itself provides an additional layer of protection for tax-exempt retirement funds through 11 U.S.C. § 522(b)(3)(C) and § 522(d)(12), with a separate dollar cap that applies only to certain individual retirement accounts under 11 U.S.C. § 522(n). For most Colorado consumers with typical 401(k)s and IRAs, these combined protections mean that retirement savings remain untouched in bankruptcy, as long as the funds stay in a qualifying retirement account.

| Retirement / Pension Type | Protection in Bankruptcy | Key Authority |

|---|---|---|

| Employer Pensions & ERISA-Qualified Plans | Most employer-sponsored retirement plans—such as traditional defined-benefit pensions, 401(k), 403(b), and similar tax-qualified plans—are treated as exempt retirement funds. Colorado exempts property held in or payable from these plans, and federal law separately protects tax-exempt retirement funds. In practice, these accounts are usually fully exempt in consumer cases, subject to limited exceptions for things like domestic support obligations. | Colo. Rev. Stat. § 13-54-102(1)(s); 11 U.S.C. § 522(b)(3)(C) |

| Traditional & Roth IRAs | Individual retirement accounts (traditional IRAs and Roth IRAs) are expressly included in Colorado's retirement exemption. In addition, federal bankruptcy law protects tax-exempt retirement funds in IRAs, with an aggregate dollar cap that applies only at the federal level. As of the most recent federal adjustment, the cap on IRA and Roth IRA funds under 11 U.S.C. § 522(n) is in the range that far exceeds the balances in most consumer cases. For most Colorado filers, properly maintained IRAs and Roth IRAs end up fully protected. | Colo. Rev. Stat. § 13-54-102(1)(s); 11 U.S.C. § 522(b)(3)(C), (d)(12), (n) |

| Government & Public Employee Retirement Plans | Colorado and federal law provide strong protection for public employee pensions and retirement plans, including state and local government retirement systems and certain federal pensions. These plans are generally treated as exempt while the funds remain in the retirement system and are often further protected by specialized nonbankruptcy statutes. | Colo. Rev. Stat. § 13-54-102(1)(s); related public pension statutes; 11 U.S.C. § 522(b)(3)(C) |

| Health Savings Accounts (HSAs) | Colorado's retirement exemption also expressly covers health savings accounts (HSAs) listed in section 13-54-102(1)(s). While HSAs are typically used for medical expenses rather than retirement income, they are treated as exempt property under Colorado law to the extent they meet the statutory definition. | Colo. Rev. Stat. § 13-54-102(1)(s) |

| Deferred Compensation & Similar Plans | Property held in or payable from qualifying deferred compensation plans is exempt under Colorado law. This can include certain 457 plans and other employer-arranged deferral vehicles, as long as they meet the statutory criteria and retain their tax-advantaged status. | Colo. Rev. Stat. § 13-54-102(1)(s); 11 U.S.C. § 522(b)(3)(C) |

One important nuance is that these exemptions primarily protect funds while they remain in the retirement plan. Once large distributions are taken out and deposited into ordinary bank accounts, they may lose some or all of their retirement-specific protection and instead be evaluated under the normal cash and bank account exemptions. Coordinating the timing of any withdrawals with the available bankruptcy exemptions in Colorado and federal retirement protections is therefore a critical part of pre-filing planning.

CO Bankruptcy Exemptions: Life Insurance and Annuities

Life insurance policies and certain annuity contracts can be important parts of a family's long-term financial planning, and Colorado law gives them special treatment in bankruptcy. At the same time, the rules are not entirely straightforward. Colorado's life insurance exemption in Colo. Rev. Stat. § 13-54-102(1)(l)has detailed conditions, and there is case law interpreting how those conditions apply in real cases.

In general, Colorado protects the cash surrender value of qualifying life insurance policies that have been owned by the debtor for at least forty-eight continuous months. As of the most recent version of the statute, the exemption covers cash value up to $250,000 for writs or executions issued against the insured, but does not protect increases in cash value attributable to “extraordinary moneys” contributed within the forty-eight months before the writ or execution. “Extraordinary moneys” are contributions or loan payments in excess of what the policy contractually requires.

The statute also distinguishes between the cash value while the insured is living and the proceeds paid on the insured's death. Proceeds paid to a designated beneficiary are generally exempt as to the insured's creditors, but that protection does not extend to the beneficiary's own creditors, and special rules apply if the estate is named as beneficiary. Annuity contracts may be evaluated under the same paragraph, under other Colorado insurance statutes, or under the separate retirement exemption depending on how the annuity is structured and used.

Key Colorado Life Insurance Exemption Rules

| Exemption Aspect | Details | Key Statute |

|---|---|---|

| Cash Surrender Value | Cash surrender value of qualifying life insurance policies can be exempt up to $250,000 if the policy has been owned by the debtor for a continuous, unexpired period of at least forty-eight months. Increases in value from “extraordinary moneys” paid into the policy during the forty-eight months before attachment or execution are not exempt. This is aimed at preventing last-minute sheltering of large sums in insurance products. | Colo. Rev. Stat. § 13-54-102(1)(l)(I)(A) |

| Death Benefits / Proceeds | Proceeds payable to a named beneficiary upon the insured's death are generally exempt, without a dollar cap, from writs or execution issued against the insured. However, this protection does not shield the proceeds from the beneficiary's own creditors, and no exemption applies when the insured's estate is the beneficiary. The interaction between beneficiary designations and creditor claims is often fact-specific. | Colo. Rev. Stat. § 13-54-102(1)(l)(I)(B), (II), (III) |

| Annuities and Related Contracts | Certain annuity contracts and insurance-type accounts may be treated as exempt under the same life insurance provision, under other Colorado insurance statutes, or under the separate retirement exemption in § 13-54-102(1)(s), depending on how the contract is structured and used. Courts look closely at the facts, so classification and exemption of annuities tends to be a case-by-case, fact-intensive analysis. | Colo. Rev. Stat. § 13-54-102(1)(l); Colo. Rev. Stat. § 13-54-102(1)(s) |

Important: The treatment of life insurance and annuities in bankruptcy is highly fact-specific and influenced by case law. The summary above is a general overview of how Colorado's statute is structured, not a substitute for reviewing the actual contract and current Colorado and federal case law.

Planning Around Life Insurance and Annuities

In practice, annuities are one of the most technical—and risky—areas of bankruptcy exemptions in Colorado. Annuity contracts are often drafted so that the person signing the paperwork is not clearly the “owner” in the way the exemption statute uses that term. A debtor may be listed as an annuitant or beneficiary rather than the contract owner, or ownership rights may be shared, reserved, or subject to complex restrictions.

Chapter 7 trustees know this, and annuities tend to light up their radar. If a debtor lists an annuity interest, you can expect the trustee to request the full contract and any riders, often through a detailed document request or a Rule 2004 examination. Trustees routinely dig into who technically owns the contract, who can change beneficiaries, who can demand distributions, whether there have been recent transfers, and how the payments are structured.

Because of this scrutiny, annuities are not “set it and forget it” assets in bankruptcy. Any practitioner should treat the appearance of an annuity in a case as a bright red flag and slow down to analyze ownership, control, funding history, and the interplay between Colorado's exemption statute and relevant case law. Done carefully, the life insurance and annuity exemptions can still protect important long-term planning, but they require a much deeper dive than simpler Colorado bankruptcy exemptions such as household goods or motor vehicles.

How Colorado Bankruptcy Exemptions Work in Chapters 7 and 13

Colorado bankruptcy exemptions play different roles depending on whether you file under chapter 7 or chapter 13. At a high level, exemptions help determine how much property is exposed to creditors and, in chapter 13, how much unsecured creditors must receive over the life of the plan.

This section gives a high-level overview. For a deeper, chapter-by-chapter discussion of how exemptions work in real cases, our dedicated Colorado guides are the go-to resources: see our Colorado chapter 7 bankruptcy guide and our Colorado chapter 13 bankruptcy guide.

Chapter 7 & Colorado Exemptions

In a chapter 7 case, the trustee compares your assets to the available bankruptcy exemptions in Colorado. Non-exempt equity can, in some situations, be liquidated for the benefit of creditors, while exempt property is generally protected. Many consumer cases end up as “no-asset” cases because all of the debtor's property is either exempt or has no meaningful equity after liens are accounted for.

Exemptions in chapter 7 are therefore about drawing a line between what a trustee could potentially sell and what you are allowed to keep as part of your fresh start.

Chapter 13 Colorado Exemptions

In a chapter 13 case, exemptions serve a different function. Instead of selling non-exempt property, the court looks at how much non-exempt value you would have in a hypothetical chapter 7 and uses that figure as part of the “best interests of creditors” test. In simple terms, the more non-exempt property you would have in chapter 7, the more your chapter 13 plan usually has to pay to unsecured creditors over time.

You generally keep your property in chapter 13 so long as you complete the plan, but exemptions still matter because they help set the minimum required payout to unsecured creditors.

Key Differences in How Exemptions Apply

Key differences in how exemptions apply can be summarized this way:

- Chapter 7: exemptions primarily determine what non-exempt equity a trustee could reach or sell, and whether the case is likely to be treated as an “asset” or “no-asset” case.

- Chapter 13: exemptions help set the minimum amount that unsecured creditors must receive through the plan, even though you generally keep your property so long as the plan is completed.

Both chapters rely on the same Colorado bankruptcy exemptions, but they use them in very different ways. Choosing between chapter 7 and chapter 13 is a strategy decision that should factor in not just your exemptions, but also income, secured debts, and long-term goals—which is why our chapter 7 guide and chapter 13 guide go into these issues in much more detail.

How to Claim Bankruptcy Exemptions in Colorado

Claiming bankruptcy exemptions in Colorado is not just a paperwork exercise—it is the process that decides how the exemption rules you have been reading about actually apply to your real-life property. Getting this wrong can mean losing assets you could have kept or inviting avoidable trustee challenges, which is why this step deserves careful attention.

In a Colorado bankruptcy case, you must fully disclose your assets and then claim the appropriate exemptions on your schedules, usually with supporting values and documentation. The court, the trustee, and your creditors all rely on those schedules to understand what you are asking to protect under Colorado law. Even if your case ultimately becomes a “no-asset” case, you still need to get the exemption work right.

Practical Steps for Claiming Exemptions

At a very high level, the process looks like this. In practice, each step involves more nuance than most people expect, especially when there are questions about value, co-ownership, or how a particular asset should be categorized under the Colorado exemption statutes:

Steps to claim exemptions:

- Compile a complete list of all your assets

- Match each asset to a relevant exemption

- Complete the necessary bankruptcy forms

In a real case, this usually means gathering recent statements, titles, appraisals, tax notices, and other documents to support your values; deciding whether an item belongs under the homestead, motor vehicle, tools of the trade, retirement, or other Colorado bankruptcy exemptions; and then carefully filling out the property and exemption schedules so that everything lines up and is internally consistent.

Why Working With a Colorado Bankruptcy Attorney Matters

While it is possible to file a case without a lawyer, the exemption analysis is one of the main areas where self-represented filers run into trouble. Trustees routinely review exemption claims, challenge values, and ask for more information when something does not look right. A knowledgeable Colorado bankruptcy attorney can help you:

- Apply the correct Colorado statutes to each asset and avoid overlooking important exemptions

- Choose realistic values and document them in a way that makes sense to the trustee and the court

- Spot red flags—such as recent transfers, annuities, or unusually titled property—before the case is filed

Careful planning and professional guidance can make the difference between a smooth case where your exemptions are accepted and a stressful case filled with objections and hearings. If you are serious about protecting your property using the bankruptcy exemptions in Colorado, talking with an experienced attorney before you file is almost always the safest approach.

Common Mistakes and Tips for Maximizing Exemptions

Avoiding common mistakes can have as much impact on your case as knowing the rules themselves. The exemption system in Colorado is powerful, but it is not forgiving if you guess, assume, or try to cut corners. Missteps withColorado bankruptcy exemptions can turn what should have been a straightforward fresh start into a fight with the trustee—or even the loss of property you could have kept.

Mistake #1: Trying to Navigate Exemptions Without an Attorney

The single biggest mistake for anyone who owns a home, vehicles, retirement accounts, or other significant assets is trying to handle exemptions without legal counsel. If you have property to protect, it rarely makes sense to gamble that property on a do-it-yourself filing. Trustees review exemption claims closely, and a misunderstanding ofbankruptcy exemptions in Coloradocan cost far more than a lawyer's fee.

An experienced Colorado bankruptcy attorney does more than “fill out forms.” They help you decide when to file, how to value assets, which exemptions apply, and how to structure the case so your property is protected as fully as the law allows. For a debtor with real assets, not getting legal advice is often the most expensive “savings” decision they ever make.

Mistake #2: Guessing at Values Instead of Getting Real Numbers

Another common mistake is casually estimating values instead of backing them up. Exemptions only protect you up to the statutory caps. If your house, vehicle, or other property is close to those limits, a proper valuation can be the difference between a smooth case and a dispute with the trustee.

With a home that is anywhere near the edge of the homestead limit, a professional appraisal is often worth the extra cost. A written opinion from a licensed appraiser is much harder to refute than a guess or a Zillow printout. The same logic applies to vehicles, jewelry, collectibles, and other items where value can be debated: when an asset matters to your life, it deserves a serious, documented valuation.

Mistake #3: Not Listing Everything (or “It’s Just a Small Thing” Thinking)

Some people assume they do not need to list every item or account, especially if they think something is “too small” to matter. That is a serious error. Bankruptcy schedules are signed under penalty of perjury, and trustees expect a full, honest inventory of what you own—even if most of it ends up being exempt or of little resale value.

Leaving out property, even by accident, can undermine your credibility, trigger extra scrutiny, and in extreme cases jeopardize exemptions or the discharge itself. A complete list of assets is the foundation of any exemption analysis. Only when everything is on the table can you and your attorney match each item to the correct Colorado bankruptcy exemptions.

Tips for Maximizing Colorado Bankruptcy Exemptions

Some practical ways to avoid these mistakes and get the full benefit of the exemption system include:

- Work with a knowledgeable Colorado bankruptcy attorney if you have a home, vehicles, or other meaningful assets.

- Use realistic, documented values—appraisals for homes, solid market data for vehicles, and receipts or expert opinions for high-value items.

- List every asset you own, even small or sentimental items, and then decide how to exempt them; do not self-censor your schedules.

- Review the major bankruptcy exemptions in Colorado with counsel before filing so you understand how they apply to your specific mix of property.

Proper planning, full disclosure, and professional guidance are the keys to making the most of your exemptions and protecting the property that matters most to you.

Frequently Asked Questions About Colorado Bankruptcy Exemptions

Navigating bankruptcy can be complex and daunting. These common questions and answers are meant to give a practical overview of how Colorado bankruptcy exemptionswork in real cases, and when it's time to slow down and get individualized legal advice.

What happens if I mistakenly claim an exemption in Colorado?

If you mistakenly claim an exemption, the most common outcome is that the chapter 7 trustee or a creditor objects and asks the court to disallow part or all of that exemption. In some cases, that can put the asset at risk of being sold or force you to negotiate a cash settlement with the estate. Honest mistakes can often be corrected by amendment, but inaccurate, incomplete, or misleading schedules can also damage your credibility with the court and make the entire case more difficult. This is one reason careful planning and accurate values are so important when using bankruptcy exemptions in Colorado.

Can I choose between federal and state bankruptcy exemptions in Colorado?

No. Colorado is an “opt-out” state, which means individual debtors who have been Colorado residents for the required time must generally use the Colorado bankruptcy exemptionsinstead of the federal exemption scheme. Federal law still plays a role—especially for retirement accounts and certain benefits—but you do not get to simply pick the federal exemption list instead of Colorado's state-specific system.

Do Colorado bankruptcy exemptions change over time?

Yes. The Colorado legislature has updated exemption amounts and categories multiple times in recent years, including significant changes in 2022. This means that exemption limits you find in an old article or an outdated form may no longer be correct. Before you file, it's important to confirm that you are working from the most current version of the Colorado statutes and any recent amendments affecting bankruptcy exemptions Colorado law provides.

Is legal advice really necessary to claim Colorado bankruptcy exemptions?

Technically, you are allowed to file and claim exemptions without a lawyer. Practically, if you have a home, vehicles, retirement accounts, or other meaningful assets, trying to navigate Colorado bankruptcy exemptions on your own is a major risk. Trustees routinely scrutinize exemption claims, and the cost of a mistake can easily exceed what you would have paid for competent legal counsel—especially if the issue involves a house with borderline equity, an annuity, or a contested valuation.

Can Colorado bankruptcy exemptions protect all of my property?

No exemption system protects everything. Colorado's homestead, motor vehicle, tools of the trade, and retirement exemptions are generous, but there are still limits. Some property may be only partially exempt, and some categories (such as certain recreational vehicles, large cash balances, or high-value luxury items) may not be fully protected. The goal is to use the available bankruptcy exemptions in Colorado to shield as much as the law allows, while being realistic that there are statutory caps and carve-outs.

Does Colorado have a wildcard bankruptcy exemption?

No. Unlike the federal exemption scheme and some other states, Colorado does not have a true “wildcard” exemption that you can apply to any property of your choice. Instead, Colorado uses a series of targeted exemptions—homestead, motor vehicle, tools of the trade, bank accounts, and others—that you must match to each asset. With careful planning, those category-specific protections can sometimes function like a partial wildcard, but there is no single, flexible pool of wildcard dollars under Colorado law.

Is an RV exempt under Colorado bankruptcy law?

Most recreational vehicles are not automatically covered by the standard motor vehicle exemption. Colorado's motor vehicle exemption specifically excludes motor homes, travel trailers, tent trailers, and similar recreational vehicles from that particular category. In some cases, if an RV is truly used as your principal residence and fits the statutory definition (similar to a manufactured or mobile home), you may argue homestead protection instead, but that is a fact-intensive question and often involves case law. Because RVs sit at the intersection of homestead, vehicle, and personal property rules, they tend to draw trustee scrutiny, and anyone with an RV should discuss it carefully with a Colorado bankruptcy attorney before filing.

Do Colorado bankruptcy exemptions work the same in chapter 7 and chapter 13?

The same basic Colorado bankruptcy exemptions apply in both chapter 7 and chapter 13, but they are used differently. In chapter 7, exemptions primarily determine what a trustee could sell and whether your case will be treated as an “asset” or “no-asset” case. In chapter 13, exemptions help set the minimum amount that unsecured creditors must receive through your repayment plan under the “best interests of creditors” test. Our Colorado chapter 7 guide and chapter 13 guide go into these differences in more detail.

Do I need to get appraisals or formal valuations for my assets?

You are required to list good-faith, realistic values for your property. When an asset is close to the applicable exemption limit—such as a home near the homestead cap or a vehicle with borderline equity—getting a professional appraisal or other documented valuation is often worth the cost. A licensed appraiser's written opinion is much harder for a trustee to attack than a guess or an online estimate, and it can make the difference between keeping the asset and facing a dispute over non-exempt value.

Protecting Your Property With Colorado Bankruptcy Exemptions

The core idea behind Colorado bankruptcy exemptions is simple: you are not supposed to lose everything just because you need relief from debt. Colorado law sets out a detailed framework for protecting your home, vehicles, tools, retirement accounts, benefits, and other essentials so you have a real chance at a fresh start.

At the same time, the details are anything but simple. Homestead rules, motor vehicle limits, tools of the trade, retirement protections, life insurance, annuities, and wage and benefit exemptions all have their own conditions, caps, and traps for the unwary. The difference between a smooth case and a painful one often comes down to how carefully you match your assets to the right bankruptcy exemptions in Colorado, how accurately you value those assets, and whether you spot issues early—especially with borderline equity, annuities, or unusual forms of ownership.

If you are thinking about filing, the safest path is to treat your exemptions as a planning project, not a formality. Make a complete list of what you own, get solid numbers for anything that matters to you, and then sit down with a Colorado bankruptcy attorney who works with these statutes and trustees every day. Used thoughtfully, bankruptcy exemptions Colorado law provides can protect the property that matters most while you deal with your debt and move forward with the next chapter of your financial life.

Explore Our Colorado Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin