Understanding Bankruptcy Laws in Ohio

Bankruptcy in Ohio is not just a financial decision; it's a legal process with long-term implications for you and your family. There is so much of your financial health on the line, therefore it's essential to approach it with a clear understanding of what it entails. While the process may seem difficult, knowing the steps and requirements can help ease the burden. This article will guide you through the types of bankruptcy available in Ohio, the filing process, and the unique state laws that may affect your case.

What Is Bankruptcy in Ohio?

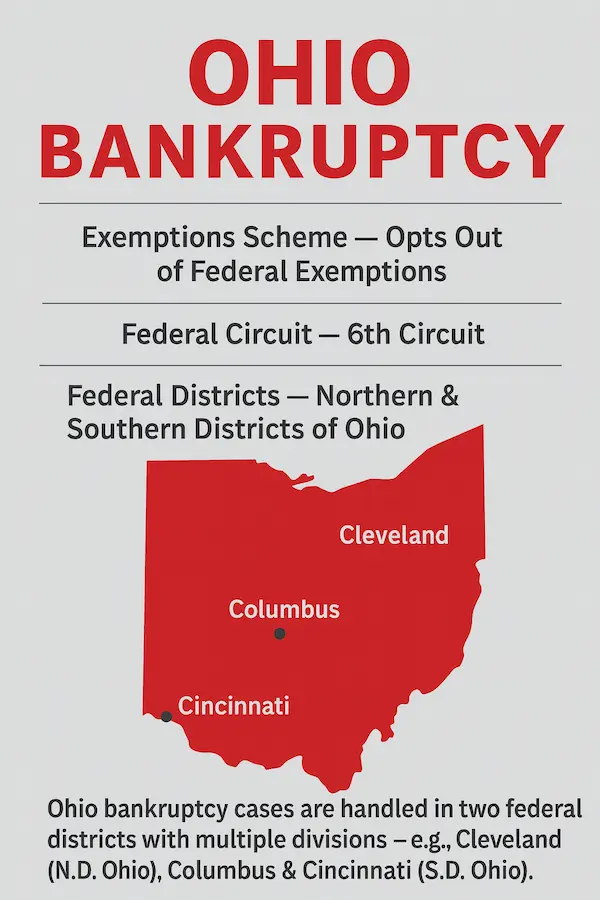

Anchored by manufacturing, healthcare, logistics, education, and agriculture, Ohio’s economy offers plenty of opportunity—but financial setbacks still happen. If high-interest credit cards, unexpected medical bills, or other debts have you feeling stuck, bankruptcy may provide a lawful path to relief. The process is governed federally under Title 11 of the U.S. Code and Ohio cases are filed in the Northern or Southern District of Ohio. Ohio is an “opt-out” state for exemptions, so residents generally use Ohio’s own exemption laws rather than the federal scheme, with amounts updated periodically under Ohio Rev. Code § 2329.66.

Bankruptcy is a legal process designed to help individuals or businesses eliminate or repay their debts under the protection of the federal bankruptcy court. In Ohio, as in other states, the bankruptcy process is governed by federal law, but there are specific state provisions you need to be aware of. Bankruptcy is intended to give debtors a fresh start while ensuring that creditors are treated fairly.

The concept of bankruptcy is often misunderstood. Many people see it as a last resort, but it can be a strategic step toward rebuilding financial health. Bankruptcy can provide relief from harassing creditors and offer a structured way to address debts. In Ohio, understanding both the federal framework and state-specific nuances is vital for anyone considering this option, as the laws can significantly affect the outcome of your case.

What Happens When You File for Bankruptcy in Ohio?

One of the major benefits of filing for bankruptcy is the protection you receive when you file. When you file a bankruptcy petition, an automatic stay immediately stops most creditor actions. For example, if you had a foreclosure pending in Cleveland and filed before the foreclosure sale, the sale would not be able to move forward.

Residency Requirements

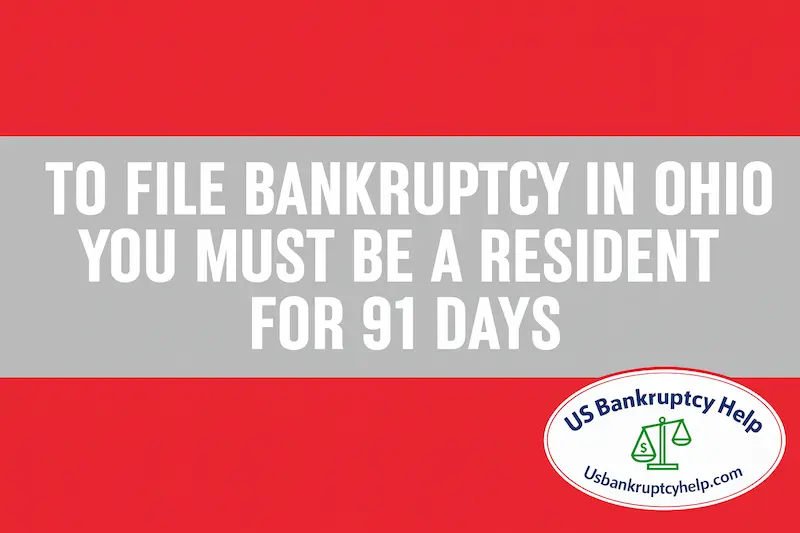

To file for bankruptcy in Ohio, you must have lived in the state for at least 91 days. This residency requirements ensure that you're subject to the appropriate state's laws and exemptions, which can vary significantly. If you have recently moved to Ohio, understanding these rules will help you plan your filing strategy accordingly.

Types of Bankruptcy

In Ohio, most individuals file for either Chapter 7 or Chapter 13 bankruptcy. Ohio businesses typically file under Chapter 7 or Chapter 11. Individuals can also file under chapter 11, but is is rare. Each type has its own eligibility requirements, processes, and outcomes. Understanding the differences between these types is very important so that you can make an informed decision about which path to take.

Chapter 7 Bankruptcy

Chapter 7 is a way to discharge unsecured debt (like credit cards and medical bills) quickly. It is the most common type of bankruptcy filed in Ohio. Sometimes chapter 7 is called a "liquidation" form of bankruptcy. However losing assets is rare because of Ohio's generous bankruptcy exemptions scheme.

Eligibility for Chapter 7

To qualify for chapter 7, most Ohio filers must be under the median income level or complete the means test. This compares your “current monthly income” (the average of the last 6 full months, annualized) to the Ohio median for your household size.

Chapter 13 Bankruptcy

Chapter 13 bankruptcy involves a 3 to 5 year payment plan with many great options that also offers a discharge of unsecured debt at the end of the 3 to 5 year plan. It is often used by Ohio residents to save a home from foreclosure, catch up on overdue mortgage payments, or manage tax debts. Chapter 13 is also a good option for those who have too much income to qualify for Chapter 7 but still need debt relief.

Chapter 7 vs Chapter 13 Bankruptcy in Ohio

Choosing between Chapter 7 and Chapter 13 depends on various factors, including your income, assets, and financial goals. Consulting with a bankruptcy attorney can help you decide which option is best for your situation. Understanding the differences between these types can significantly impact how you manage your debts and assets moving forward.

Chapter 11 Bankruptcy

Chapter 11 isn't a chapter of bankruptcy that is commonly filed by individuals in Ohio, but it is available to those who do not qualify for chapter 13. However, chapter 11 bankruptcy is a great way for struggling Ohio businesses to reorganize and continue operating.

Ohio Bankruptcy Laws Overview

Ohio follows federal laws, but Ohio also has specific state laws that affect the bankruptcy process. Being familiar with these will help you understand and navigate a bankruptcy case more effectively.

Federal vs State Ohio Bankruptcy Laws

Think of it like this: federal laws are the main rules of the game, while state laws are like the house rules that can change how you play. In Ohio, federal bankruptcy laws set the overall framework, but state-specific provisions can influence exemptions, residency requirements, and other aspects of the process.

Ohio Bankruptcy Exemptions

Ohio has its own set of bankruptcy exemptions that differ from federal exemptions. You have to be an Ohio resident for at least 730 days to be able to use these exemptions. These exemptions allow you to protect certain assets from being sold to pay off creditors. As a matter of fact, Ohio "opts out" of the federal exemption scheme, so most Ohio residents must use Ohio's own exemptions. We highly encourage you to check out our page on Ohio's bankruptcy exemptions for more information on the specific exemptions (like the homestead and vehicle exemptions) available and how they can protect your property during bankruptcy.

Ohio-Specific Bankruptcy Procedures

Ohio has state-specific bankruptcy procedures that apply in addition to federal requirements. Cases are filed in either the Northern or Southern District of Ohio, and each district maintains Local Bankruptcy Rules, standing orders, and required local forms (with some division-specific practices). Using the correct Ohio forms, following local filing and noticing guidelines (including creditor-matrix and fee rules), and observing page and signature requirements helps avoid delays. Filers should also complete the required pre-filing credit counseling and post-filing financial-management course and review the court’s instructions before submitting documents.

The Importance of Legal Guidance

After practicing bankruptcy law for 18 years I have seen many people get hurt by filing bankruptcy without an attorney. I have talked to chapter 7 trustees who prefer debtors who are not represented, because they usually make mistakes and are more likely to turn over property. It is highly recommended that you consult with a qualified Ohio bankruptcy attorney before filing. It is easy to get in trouble in bankruptcy if you don't know what you're doing, and I don't know why people put so much on the line by trying to do it themselves. Do yourself and your family a favor and get an Ohio bankruptcy attorney

The Ohio Bankruptcy Filing Process

The Ohio bankruptcy process starts with filing a petition in the correct bankruptcy court in your area. Filing for bankruptcy in Ohio involves several steps. Here's a simplified guide to help you understand the process.

Essential Ohio Bankruptcy Information & Resources

Discover how bankruptcy in Ohio can help you eliminate debt, protect your property, and move toward financial stability under Ohio and federal law.

Credit Counseling

Before you file, you must complete a credit counseling course from an approved agency. This course will help you evaluate your financial situation and explore alternatives to bankruptcy. The goal is to ensure that filing for bankruptcy is your best option. Credit counseling provides valuable insights into managing finances and can sometimes offer solutions that make filing unnecessary. It's important to select an agency approved by the Department of Justice to ensure that the course meets all legal requirements. Completing this step is mandatory and must be done within 180 days before filing your bankruptcy petition. This requirement underscores the importance of being well-informed and considering all possible options before proceeding with such a significant legal action.

File a Petition

To start the bankruptcy process, you must file a petition with the Ohio bankruptcy court. This document includes details about your assets, debts, income, and expenses. Filing the petition requires careful preparation and attention to detail.

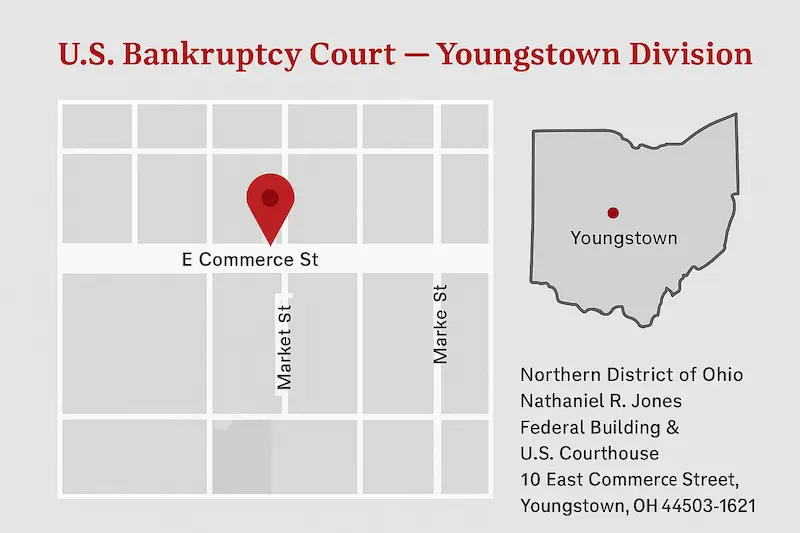

Which Bankruptcy Court Handles Your Case?

In Ohio, your case is assigned by the county where you live. Residents of northern counties—such as those around Cleveland (Cuyahoga), Akron (Summit), Toledo (Lucas), Youngstown (Mahoning), and nearby areas—file in the U.S. Bankruptcy Court for the Northern District of Ohio and are placed on the calendar for the correct division (e.g., Cleveland, Akron, Toledo, or Youngstown). Court hearings for these cases are scheduled on that division’s docket and may be held in person or by video/phone, as specified in your hearing notice.

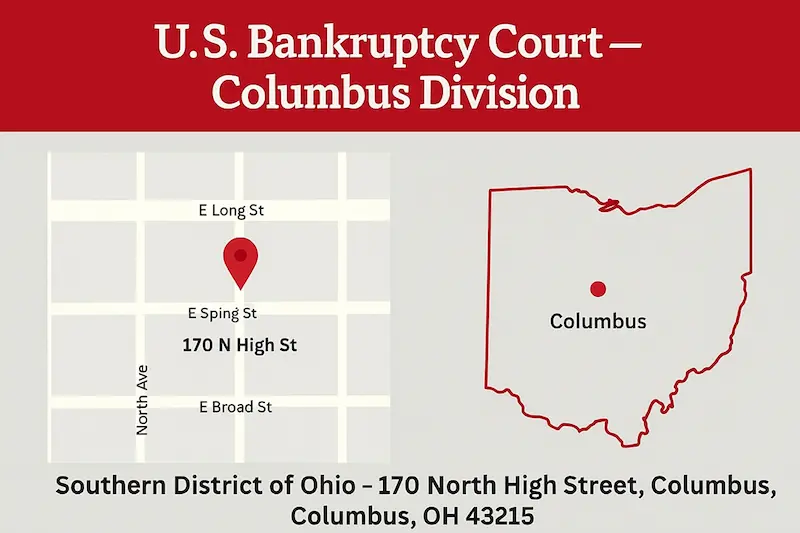

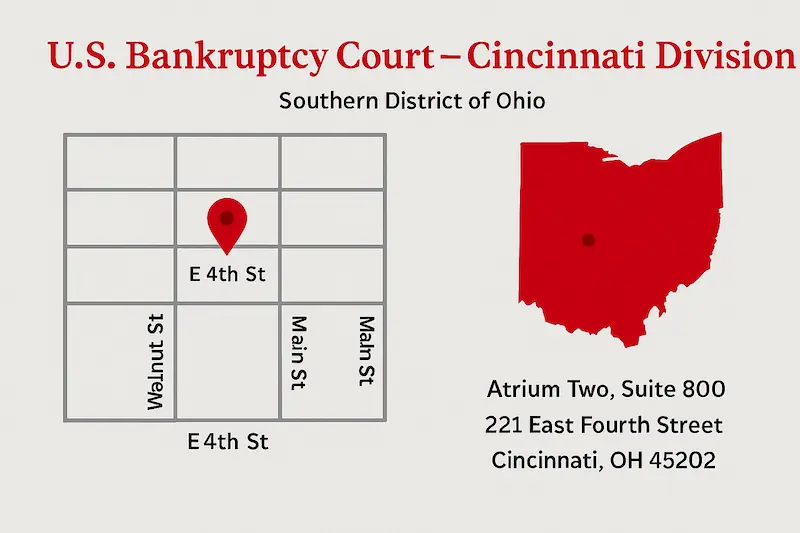

Those living in central and southern counties—such as Columbus (Franklin), Cincinnati (Hamilton), Dayton (Montgomery), and surrounding areas—file in the U.S. Bankruptcy Court for the Southern District of Ohio and are assigned to the Columbus, Cincinnati, or Dayton division. Hearings appear on that division’s calendar, with your notice indicating whether you must appear in person or by video/telephone.

Automatic Stay

Once your petition is filed, an automatic stay goes into effect. This stops creditors from collecting debts, garnishing wages, or foreclosing on your home. The automatic stay is one of the most powerful protections offered by bankruptcy, providing immediate relief from financial pressures.

During this time, creditors are prohibited from contacting you, which can provide a much-needed respite and allow you to focus on the bankruptcy process.

Ohio 341 Meeting of Creditors

There is a "meeting of creditors" required for every bankruptcy case that is filed. Most often, creditors do not attend this meeting, despite it's name. Section 341 meetings of creditors in Ohio are generally conducted remotely (telephonic or video) under current U.S. Trustee Program procedures, unless your trustee or the court directs otherwise.

Your official notice will provide the date, time, and connection details, and any updates will appear on your docket and the court’s calendars.

Preparing for the 341 Meeting

Before your 341 meeting your bankruptcy trustee should have made a document request to you and your attorney. You will have provided the requested documents to your attorney before the meeting. These generally include pay check stubs, tax returns, and bank statements. You will also have to verify your ID and Social security number with the trustee's office, so don't be alarmed if your trustee requests a copy of your social security card and driver's license or other government ID.

Role of the Trustee

The bankruptcy trustee is an impartial party appointed to oversee your case. Their role includes verifying the information in your petition, asking questions about your financial situation, and ensuring that creditors' interests are considered. If you are in chapter 7, the trustee may also review your assets to determine if any non-exempt property can be sold to pay creditors. If you are in chapter 13, the trustee will collect your monthly plan payments and distribute them to creditors.

Debtor Education Course

Before your debts can be discharged, you must complete a debtor education course. This course focuses on financial management and preventing future financial issues. The course covers topics such as budgeting, saving, and using credit wisely, equipping you with the tools to avoid future financial pitfalls.

Like the credit counseling course, completion of this course is mandatory and can be done on the phone or online. This must be done after filing the petition but before the discharge is granted. Successfully completing the debtor education requirement demonstrates your commitment to financial responsibility and is a crucial step toward achieving a fresh financial start.

Debt Discharge

Discharge is an order from the bankruptcy court to your general unsecured creditors. This order mandates that creditors may no longer take any action whatsoever against you to collect on your debt with them.

Chapter 7 Discharge

In chapter 7, discharge typically occurs about 60 days after the 341 meeting, provided there are no objections, and you complete your financial management course.

Chapter 13 Discharge

Chapter 13 discharge generally occurs after you complete your payment plan, which lasts 3 to 5 years.

Understand Ohio's Bankruptcy Laws

Understanding bankruptcy laws in Ohio is crucial for anyone considering filing. By knowing the types of bankruptcy, the filing process, available exemptions, and state-specific regulations, you can make informed decisions about your financial future. Bankruptcy is a significant legal step, and consulting with a experienced Ohio bankruptcy attorney can help you navigate the process and protect your interests.

Whether you're struggling with overwhelming debt or seeking a fresh financial start, understanding your options is the first step toward financial recovery. Making informed choices and seeking professional guidance can empower you to regain control of your financial life and work toward a more stable and secure future.

Frequently Asked Questions

Do I have to complete credit counseling before filing bankruptcy in Ohio?

Yes. Federal law requires every debtor to finish a credit-counseling course from a DOJ-approved agency within 180 days before filing. The session reviews your finances and confirms that bankruptcy is the right step.

What is the “automatic stay,” and how does it protect me?

The instant your Ohio bankruptcy petition is filed, an automatic stay freezes most collection actions—calls, wage garnishments, lawsuits, even foreclosure—giving you immediate breathing room while the case proceeds.

How does the Ohio means test decide if I qualify for chapter 7?

The means test compares your last six months of household income to Ohio’s median. Below-median income usually passes automatically; above-median filers may still qualify after deducting allowable expenses.

What happens at the § 341 “meeting of creditors” in Ohio?

About 30–40 days after filing, you attend a short 341 meeting (often at your local U.S. Courthouse). Under oath, you answer a trustee’s questions about your petition; creditors may attend but rarely do.

How long does a chapter 7 case usually take in Ohio?

Most Ohio chapter 7 cases conclude in roughly four to six months from filing to discharge, provided there are no objections or complex asset issues.

What is a reaffirmation agreement, and should I sign one?

A reaffirmation agreement lets you keep secured property—like a car—by recommitting to the loan after filing. You remain liable for that debt, so discuss risks and benefits with your attorney before signing.

How do Ohio’s residency rules affect my bankruptcy filing?

You must live in Ohio at least 91 days to file here andtwo years to use Ohio exemptions. Recent movers may need to apply a prior state’s exemption scheme.

What’s the difference between the credit-counseling and debtor-education courses?

Credit counseling happens before filing and explores alternatives; the debtor-education course occursafter filing and teaches budgeting, saving, and responsible credit use—both are mandatory for discharge.

Are student loans or recent tax debts wiped out in Ohio bankruptcy?

Generally, student loans and most recent tax debts are not dischargeableabsent special hardship findings. Chapter 13 can still structure payments to manage these obligations more affordably.

Explore Our Ohio Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown