Arizona Bankruptcy Laws: What to Know Before You File

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

If you’re searching Arizona bankruptcy laws, you may be dealing with collection calls, past-due payments, a lawsuit threat, or concern about wage garnishment, foreclosure, or vehicle repossession. This page explains what bankruptcy in Arizona typically looks like, where federal rules apply, and where Arizona-specific rules matter most, especially Arizona exemptions (the laws that may protect certain property).

Who Can File Bankruptcy in Arizona in 2026?

Financial difficulty can happen at any time and for many reasons, including job loss, illness, rising living costs, or a sudden family emergency. In Arizona, whether or not you can file for bankruptcy will depend on factors such as the type of debt you have, your income, your prior filing history, and the chapter you want to use. On this page we have many tools and resources to help you understand your options and what may be best for your unique situation.

2026 Updates for Bankruptcy in Arizona

The Arizona personal property exemption amounts currently in effect continue to apply unless Arizona law changes or an applicable adjustment takes effect. Arizona’s homestead exemption is subject to periodic adjustment, so anyone considering bankruptcy in Arizona should confirm the current amount before filing. In some situations, the timing of a bankruptcy filing may affect how much property can be protected.

When Arizona Exemption Amounts May Change

Arizona's homestead exemption is adjusted each year on January 1 based on cost-of-living changes, so anyone considering bankruptcy in Arizona should confirm the current amount before filing. Because the homestead exemption can affect how much home equity is protected, filing dates can matter for some Arizona homeowners.

When Other Arizona Property Protections Change

Some other Arizona exemption amounts may also be updated on that annual schedule, while others change only if state law is revised. For that reason, anyone considering bankruptcy in Arizona should verify the current exemption amounts before filing rather than relying on older figures.

Timing Concerns Before Filing

Exemption updates are not the only reason timing matters when filing bankruptcy in Arizona. A tax refund can matter too. If you expect to receive a refund, the timing of your case may affect whether that money is protected or exposed. Before filing, it is wise to look at your expected refund, your available exemptions, and any other assets that could be affected by the filing date.

Chapter 7 Bankruptcy in Arizona

For Arizona filers who want faster relief from dischargeable debt, chapter 7 may be the better option. It can eliminate many unsecured debts, such as credit card balances, medical bills, and personal loans, often within a few months. Debts tied to collateral, such as a home or vehicle, may call for different considerations. Learn more in our detailed guide to chapter 7 bankruptcy.

Property in Chapter 7

One of the most important questions in an Arizona chapter 7 case is whether your property is fully protected by Arizona's exemption laws. If the equity in an asset is greater than the exemption that applies, a chapter 7 trustee may have the right to sell the property and use the nonexempt portion to pay creditors.

Many people considering chapter 7 want to know whether their property is protected. The general rule is that you must have enough available exemption coverage to protect the equity in your assets. If an asset has equity above the exemption limit, it may be at risk in chapter 7.

Who Qualifies for Chapter 7 Bankruptcy in Arizona?

In most cases whether or not you qualify for relief under chapter 7 depends on your average monthly income and whether or not you can pass the chapter 7 means test.

Below the Median. If your monthly income falls below Arizona's median income, you generally qualify. Therefore, a common first checkpoint in the Chapter 7 means test is whether your household income falls below Arizona’s median income for your family size.

| Household Size | Annual Median Income (USD) |

|---|---|

| 1 | $73,935 |

| 2 | $89,027 |

| 3 | $104,965 |

| 4 | $121,174 |

| Add $11,100 for each person over 4. | |

These figures reflect cases filed on or after April 1, 2026, and they are updated periodically. Always verify against the latest U.S. Trustee Program table: UST Median Family Income by Family Size.

Above the Median. If your income is above the median income, you can still qualify, you will just have to complete the means test (form 22) in the chapter 7 petition to show that there is not a presumption of abuse.

Want to get an idea of whether or not you qualify for chapter 7 in Arizona? Check out our free chapter 7 means test calculator directly below. Select Arizona from the "state" drop down field so that the tool uses built-in Arizona specific income information, follow the steps and input your information to get an educational estimate. We've made it possible for you to save or print your results. There is no contact information required to use this free tool.

Chapter 7 Means Test Calculator

Estimate whether your household income is above or below your state’s median income for educational planning.

Educational estimate only. This Chapter 7 means test calculator is not legal advice, does not create an attorney-client relationship, and cannot account for every legal nuance. Attorney review may still be necessary.

Step 1: Initial Screening

If filing alone, household starts at 1. If filing jointly, household starts at 2. Add only additional dependents here.

Consumer debts are usually personal, family, or household debts.

Median-income dataset effective April 1, 2026. IRS/local standards preset date: Configurable - update with current IRS + USTP data. Presumption thresholds: $10,025 and $16,700 (60-month).

Chapter 13 Bankruptcy in Arizona: Repayment Plans and Property Protection

Chapter 13 bankruptcy uses a court-approved repayment plan that typically lasts three to five years. It can help if you need time to catch up on debts tied to property, or just need to discharge debt.

Income and Eligibility Requirements for Chapter 13 in Arizona

To succeed in chapter 13, you generally need regular income to support the required monthly plan payments. Chapter 13 may also be a good option if you want to protect property that could be at risk in a chapter 7 case. In some situations, it is the better fit when chapter 7 is limited by the means test or when Arizona exemption law does not fully protect your equity.

Use our chapter 13 payment plan estimator here to get Arizona specific details on what your monthly payment could look like if you were to file bankruptcy in Arizona. Make sure you select Arizona so that the tool uses Arizona specific income and expense information. This tool is free to use and does not require any contact information to get an educational estimate of what your monthly payment could be in a chapter 13 case.

Chapter 13 Plan Payment Calculator

Chapter 13 plan payments depend on many factors, including local court and trustee practices. This tool gives an educational estimate only, not legal advice.

Median-income reference date: April 1, 2026.

Comparing Chapter 13 and Chapter 7 Bankruptcy in Arizona

Chapter 13 can help Arizona filers keep important property by allowing missed mortgage or car payments to be caught up over time through a repayment plan. Chapter 7 does not offer that catch-up option, so it may be riskier for people who are behind on secured debts. For a closer look at the differences, see our chapter 7 vs. chapter 13 guide.

| Topic | Chapter 7 | Chapter 13 | Authority |

|---|---|---|---|

| Often a better fit for | People with lower income, fewer assets at risk, and a need for faster debt relief | People with regular income who need time to catch up on secured debts or protect property | 11 U.S.C. § 101(30); 11 U.S.C. § 109(e) |

| How long the case usually lasts | Usually about three to six months | Usually three to five years | 11 U.S.C. § 727(a); 11 U.S.C. § 1322(d) |

| What happens to property | Property that is not fully protected by exemptions may be sold to pay creditors | Filers usually keep their property, but may need to pay for nonexempt value through the repayment plan | 11 U.S.C. § 541; 11 U.S.C. § 726; 11 U.S.C. § 1325(a)(4) |

| Can it help you catch up on a house or car? | Not usually. chapter 7 does not provide a repayment plan to catch up on missed secured payments | Yes. chapter 13 can allow missed mortgage or car payments to be cured over time through the plan | 11 U.S.C. § 1322(b)(5) |

| Who can qualify | Income and allowed expenses are reviewed under the means test to see whether chapter 7 is available | You must have enough regular income to support a feasible repayment plan | 11 U.S.C. § 707(b); 11 U.S.C. § 1325(b) |

| Main advantages | Can erase many unsecured debts relatively quickly without requiring a repayment plan | Can help stop foreclosure or repossession, allow catch-up payments, and protect assets that might be at risk in chapter 7 | 11 U.S.C. § 362; 11 U.S.C. § 1322(b)(5) |

| Main drawbacks | Property that is not protected by exemptions may be lost | Requires years of monthly payments, budget discipline, and court oversight | 11 U.S.C. § 727(a); 11 U.S.C. § 1307 |

| How nondischargeable debts are treated | Debts such as child support, many taxes, and most student loans usually remain after the case | These debts usually are not erased, but some can be paid over time through the plan | 11 U.S.C. § 523(a) |

| Debt limits | No debt limits | Unsecured debts less than $526,700; secured debts less than $1,580,125 | 11 U.S.C. § 109(e); adjusted effective April 1, 2025 |

| Court filing fee | $338 | $313 | 28 U.S.C. § 1930; U.S. Courts fee schedule |

| When a prior bankruptcy can affect eligibility | Usually eight years after a prior chapter 7 discharge; six years after a prior chapter 13 discharge | Usually four years after a prior chapter 7 discharge; two years after a prior chapter 13 discharge | 11 U.S.C. § 727(a)(8); 11 U.S.C. § 727(a)(9); 11 U.S.C. § 1328(f) |

Not sure whether chapter 7 or chapter 13 is right for you? Check out our chapter 7 vs chapter 13 Decision Tool directly below. This tool will ask you questions about your specific situation and what is important to you to help you get an educated idea of what chapter may be best for you. Make sure to select "Arizona" so that the tool uses Arizona specific information to give you the best result for your unique financial situation.

Chapter 7 vs Chapter 13 Decision Tool

Answer a few questions to get an educational estimate of which bankruptcy chapter may fit your situation.

Step 1 of 2

Window 1 of 2: Income Snapshot

ZIP lookup is optional and used as a quick state check.

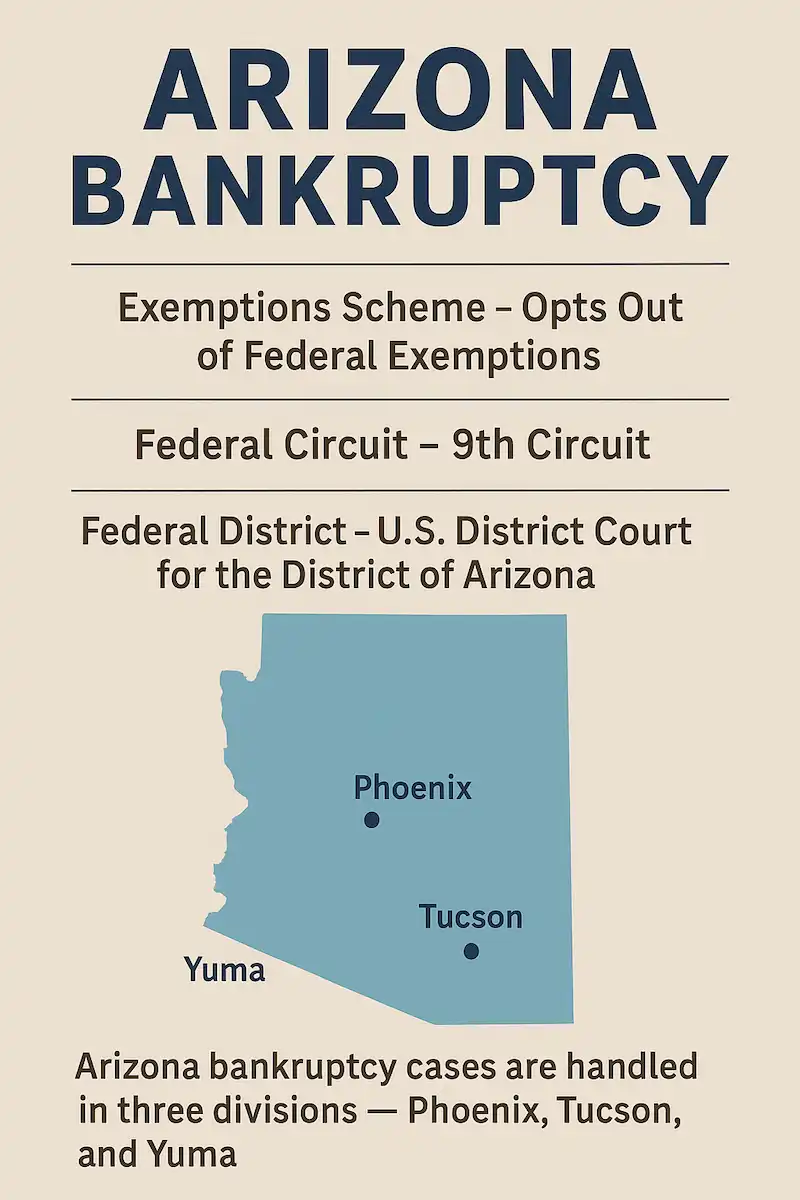

Arizona Exemptions

Arizona exemptions are the laws that help protect certain property when someone files bankruptcy in Arizona. These exemptions may apply to assets such as home equity, motor vehicles, household goods, tools used for work, and many retirement accounts, although limits and conditions apply.

In most cases, Arizona filers must use Arizona’s exemptions rather than the federal bankruptcy exemptions because Arizona is an opt-out state. It is also important to understand that recent moves can affect which exemption system applies. While many people describe this as a 730-day residency rule, the real rule looks at your residency history over a longer period and can be more complicated than it sounds.

Arizona Exemption Tools and Resources

Arizona exemptions are important to understand, and we want to do everything we can to help you become educated about how they are used. We highly recommend checking out our Arizona bankruptcy exemptions guide. There you will find our bankruptcy exemption risk estimator, our homestead exemption estimator, and our vehicle exemption estimator. These are excellent tools that use Arizona specific information so that you can see how Arizona exemptions affect the property that is most important to you.

Can You Discharge Student Loans in Arizona?

You may have heard that it is impossible to discharge, or get rid of student loans in bankruptcy. This isn't true. It is possible to discharge student loans in bankruptcy, but it is a very fact-specific process that depends on your loans and your circumstances.

Try our Student Loan Discharge Checker. No one ever seems to know where to start when trying to determine if they can discharge their student loans in bankruptcy (lawyers included). That is why we've created the cleverly named Student Loan Discharge Checker. Simply enter your unique information in the checker below, and you will get an educational estimate about whether or not you may be able to discharge your student loans in bankruptcy. This is tool uses Arizona-specific income information and covers the necessary criteria to determine student loan discharge eligibility.

This tool is free to use and does not require any contact information from you. Like all of our other forms we have enabled you to be able to save or print your results.

Arizona-Specific Procedures

Bankruptcy forms are federal, but the District of Arizona has local rules, local forms, and local practices that can affect filing requirements, hearing procedures, and trustee document requests. Your case notices (and your docket) are the official source for the deadlines and instructions that apply to your specific case.

If you want a neutral reference point, the court’s website posts current local rules and basic filing information. U.S. Bankruptcy Court for the District of Arizona (official site).

How Do I File for Bankruptcy in Arizona?

Most Arizona filings follow the steps below. The exact documents and deadlines can vary by chapter, your circumstances, and local requirements.

Credit Counseling

Within 180 days of filing, you must complete a credit counseling course from an approved provider. The course is a legal prerequisite in most cases and must be completed within the required time window.

Prepare and File the Petition

You file a petition and a set of schedules and statements that list your assets, debts, income, expenses, recent transfers, and other information. Accuracy matters. Even honest mistakes can trigger trustee follow-up requests, amendments, delays, or—in some situations—bigger problems if information is omitted. It is important to gather the financial records you will need to prepare your bankruptcy forms accurately. These documents often include pay stubs, recent tax returns, bank statements, billing statements, and a complete list of your debts, assets, income, and monthly expenses.

Practical Document Checklist (Common Starting Point)

Exact requests vary by trustee and by case. These are common items many people gather to reduce last-minute stress:

- Recent pay stubs or income proof (including benefits)

- Recent bank statements

- Most recent tax returns

- Vehicle and mortgage statements (if applicable)

- Debt list (credit cards, medical bills, loans, collections, lawsuits)

- Information on recent transfers, large payments, or sales

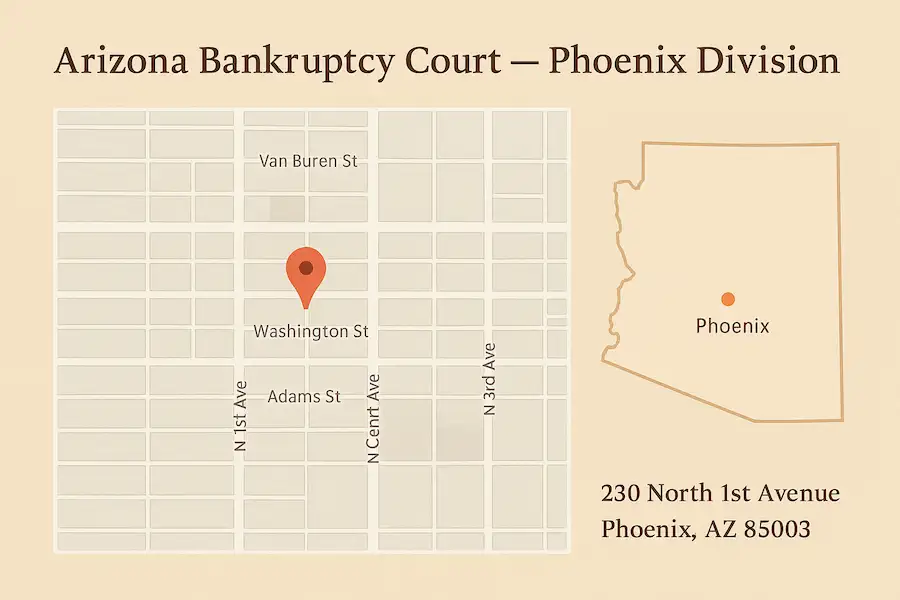

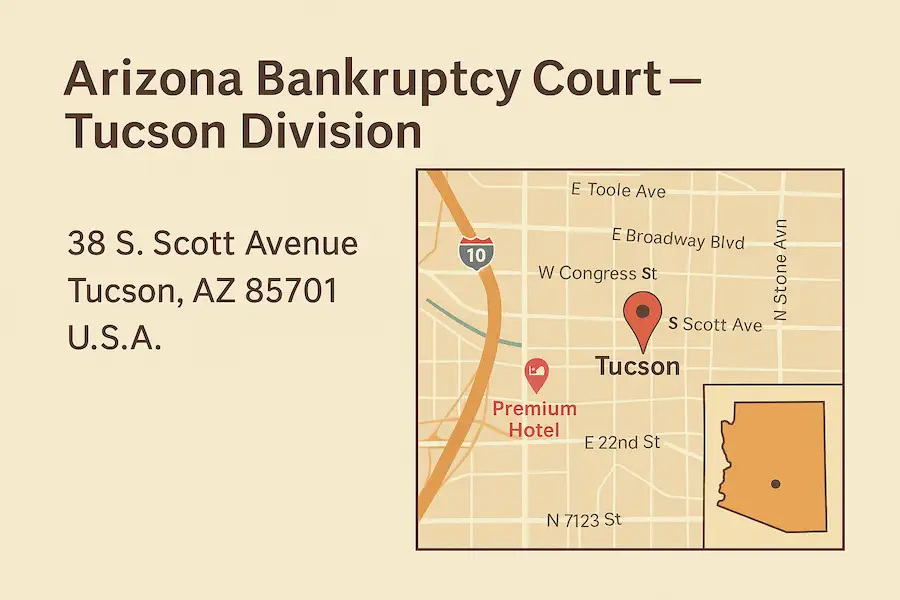

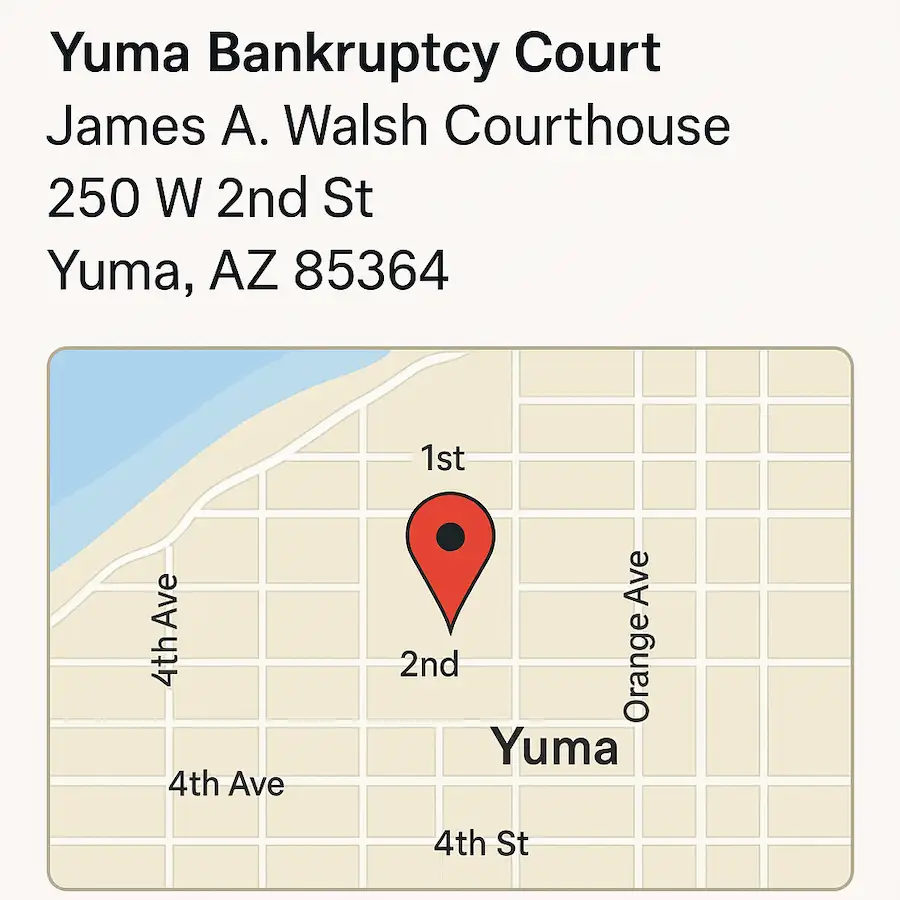

Which is the Correct Arizona Bankruptcy Court for My Case?

The U.S. Bankruptcy Court for the District of Arizona administers cases statewide. Where you live can affect division assignments and how certain matters are calendared. Because procedures can change, always follow your official notice for the 341 meeting of creditors and any hearings. Many 341 meetings of creditors in Arizona are conducted remotely, and your notice provides the official instructions.

The court maintains offices in Phoenix and Tucson, and some matters may involve other locations depending on the case and calendar. If you see an address on an infographic or older resource, treat it as a helpful starting point—not a substitute for your current notice and the court’s website.

Go to the 341 Meeting of Creditors

The 341 meeting of creditors is where the trustee asks questions under oath about your finances and paperwork. Creditors can appear, but many do not in routine consumer cases. Being organized and responsive to trustee document requests is one of the best ways to keep a case moving smoothly.

Get Your Discharge

In chapter 7, discharge is often entered a few months after filing if the case is straightforward, required courses are completed, and there are no objections. In chapter 13, discharge comes after you complete your plan and meet all plan and course requirements. Some cases take longer than the “typical” timeline due to trustee requests, asset issues, amendments, or litigation.

Why Accuracy Matters

Bankruptcy paperwork is detailed. Missing documents or inconsistent information can lead to delays, dismissal, or disputes that cost time and money. Another common pitfall is accidentally exposing an asset that could have been protected with the correct exemption approach. A qualified Arizona bankruptcy attorney can help you choose the right chapter and apply Arizona bankruptcy exemptions correctly.

Frequently Asked Questions About Bankruptcy in Arizona

How Much Does It Cost to File Bankruptcy in Arizona?

Costs commonly include the court filing fee, required courses (credit counseling and debtor education), and attorney fees (if you hire a lawyer). The most reliable numbers are the current court fee schedule and course provider pricing at the time you file. Some filers can request installments, and some chapter 7 filers may request a fee waiver if they meet strict requirements.

How Do You File for Bankruptcy in Arizona?

Filing bankruptcy in Arizona generally means: gathering financial documents (income, expenses, debts, assets), completing an approved credit counseling course, preparing the petition and schedules, filing in the U.S. Bankruptcy Court for the District of Arizona, and then attending the 341 meeting of creditors. After that, the case proceeds toward discharge in chapter 7 or plan confirmation and completion in chapter 13.

Can Inherited Property Be Included in a Bankruptcy in Arizona?

Yes. Inheritance can become part of the bankruptcy estate depending on timing and the chapter. If you become entitled to an inheritance before filing, it is typically part of the case. If you become entitled to an inheritance within 180 days after filing, it may also be included under bankruptcy law. Whether it is protected depends on the facts and whether an exemption applies. This is very fact-specific, so it’s wise to get legal advice before you accept, spend, transfer, or disclaim an inheritance if bankruptcy is on the table.

Can I File Bankruptcy Without My Spouse in Arizona?

Yes. You can file an individual bankruptcy in Arizona even if you are married. Because Arizona is a community-property state, the filing can still involve community income, community debts, and community assets, and a spouse’s income is often relevant to the means test and household budget calculations. Whether one spouse should file or both spouses should file depends on the debts, assets, income, and goals.

For a deeper dive, see Can Just One Spouse File Bankruptcy?.

How Long Does Bankruptcy Take in Arizona?

A typical consumer chapter 7 case often runs about 3–4 months from filing to discharge when paperwork is complete and there are no disputes. A chapter 13 case lasts longer because it is built around a 3–5 year repayment plan.

How Much Does a Bankruptcy Lawyer Cost in Arizona?

Attorney fees vary by chapter, complexity, and local practice. Many attorneys charge a flat fee for a routine chapter 7 case, while chapter 13 often involves different fee structures and may be paid in part through the plan (subject to court rules and disclosure). The most accurate quote usually comes after a lawyer reviews your income, assets, debts, and goals.

How Often Can You File Bankruptcy in Arizona?

You can file bankruptcy more than once, but there are waiting-period rules that control when you can receive a discharge again. For example, after a prior chapter 7 discharge, there is generally an eight-year waiting period (measured from filing date to filing date) before you can receive another chapter 7 discharge. Other chapter combinations have different waiting periods and exceptions.

For more detail, see How Often Can You File Bankruptcy?.

Final Thoughts: Making a Clear Plan Under Arizona Bankruptcy Laws

Not every person's financial situation is the same, and what you may need to do do get your financial situation in order could be much different from what someone else needs to do. Understanding Arizona bankruptcy laws can help you make calmer, more informed choices, especially when you’re deciding between chapter 7 and chapter 13, and when you’re trying to protect property using Arizona exemptions. If you’re under pressure from deadlines or active collection activity, individualized guidance can be especially important.

Explore Our Arizona Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin