What is Chapter 7 Bankruptcy?

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

Chapter 7 bankruptcy can eliminate many common unsecured debts, including credit cards, medical bills, personal loans, old utility bills, and certain collection accounts. But filing Chapter 7 is not just about whether the debt can be wiped out. You also need to know whether your property is protected, whether your income creates a means test issue, and whether any debts will survive the case. For the right candidate, Chapter 7 can be a powerful reset. But it should be reviewed carefully before filing, especially if you own valuable property, recently paid or transferred assets, or have debts that may not be dischargeable.

Chapter 7 is one of the most common bankruptcy options for people dealing with personal debt because it is usually faster and simpler than a repayment case. Instead of proposing a years-long payment plan, the filer asks the bankruptcy court for a discharge of qualifying debts. In many consumer cases, that process can be completed in a matter of months.

Chapter 7 relief sounds great, but there are also some drawbacks to filing. As it is a form of "liquidation" bankruptcy, filers need to be careful navigating their exemptions to protect needed items, like their home and vehicle. Chapter 7 can also impact your credit score, so filers need to understand the long-term repercussions and how to rebuild credit after the case is closed.

How Chapter 7 Bankruptcy Works

A Chapter 7 case starts when the bankruptcy petition is filed with the court. Once the case is filed, the automatic stay goes into effect under 11 U.S.C. § 362. The automatic stay is one of the immediate protections in bankruptcy. It can instantly stop or pause many collection efforts, including collection calls, lawsuits, wage garnishments, repossessions, and foreclosure activity.

After the case is filed, a Chapter 7 trustee is appointed. The trustee does not represent the filer or the creditors. The trustee’s job is to review the filer’s paperwork, examine assets and exemptions, conduct the 341 meeting of creditors, and determine whether there are any nonexempt assets that can be sold or settled for the benefit of creditors.

If the case is completed successfully, the court enters a discharge order. The discharge is the main reason most people file Chapter 7. It eliminates the filer’s personal legal obligation to pay many qualifying debts, which is what gives Chapter 7 its real power as a debt relief option.

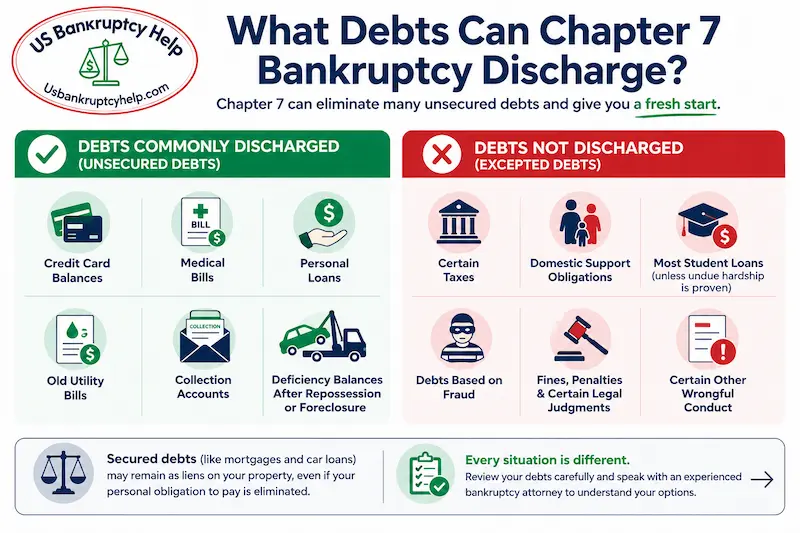

What Debts Does Chapter 7 Bankruptcy Discharge?

Chapter 7 bankruptcy can discharge many unsecured debts. Unsecured debt is debt that is not tied to a specific piece of property the creditor can take back if you do not pay. Credit cards, medical bills, personal loans, old utility bills, and many collection accounts are common examples.

Secured debts are different. A secured debt is connected to collateral, such as a mortgage tied to a house or a car loan tied to a vehicle. Chapter 7 may eliminate your personal obligation to pay a secured debt, but it usually does not remove the creditor’s lien from the property. That is why secured debts need to be reviewed carefully before filing.

Not every unsecured debt is discharged. Some debts are excepted from discharge under bankruptcy law, including certain taxes, domestic support obligations, most student loans unless the filer proves undue hardship, and debts based on fraud or certain wrongful conduct.

Examples of Debts Commonly Discharged in Chapter 7

Common examples of unsecured debts that may be discharged in Chapter 7 include:

- Credit card balances

- Medical bills

- Personal loans

- Old utility bills

- Collection accounts

- Deficiency balances after repossession or foreclosure

What Debts Does Chapter 7 Bankruptcy Not Discharge?

Chapter 7 bankruptcy can discharge many common unsecured debts, but it does not eliminate every type of debt. Some debts are protected by bankruptcy law and usually survive the case. Others may be discharged only if special requirements are met.

Examples of Debts That Are Usually Not Discharged in Chapter 7

Some examples of debts that generally survive Chapter 7 include:

- Child support and Alimony obligations

- Most student loans, unless undue hardship is proven

- Certain tax debts, including many recent income taxes and some penalties

- Debts based on fraud, false pretenses, or misconduct

- Debts for willful and malicious injury to another person or property

- Certain fines, penalties, or restitution obligations

Chapter 7 vs. Chapter 13 Bankruptcy

Chapter 7 and Chapter 13 are the two bankruptcy chapters most consumers use. The right choice usually depends on what you are trying to accomplish. Chapter 7 is often used when the main goal is to discharge qualifying debt quickly. Chapter 13 is often used when the filer needs time to catch up on a mortgage, protect property, deal with nonexempt equity, or restructure certain secured debts.

| Issue | Chapter 7 | Chapter 13 |

|---|---|---|

| Main Purpose | Discharge qualifying debts in a shorter case. | Use a court-approved repayment plan to catch up, reorganize, or protect property. |

| Who Can File | Individuals, married couples, and businesses. | Individuals and married couples. Businesses cannot file Chapter 13. |

| Main Eligibility Rule | Most consumer filers must pass the means test or qualify for an exception. | The filer must have regular income and be able to make the required plan payments. |

| Debt Limits | Chapter 7 does not have the same debt-limit structure as Chapter 13. | Chapter 13 has debt limits under 11 U.S.C. § 109. |

| Typical Case Length | Often about 4 to 6 months in a straightforward consumer case. | Usually 3 to 5 years, depending on income, plan requirements, and case facts. |

| What Happens to Property | Property protected by exemptions is kept. Nonexempt property may be sold by the trustee. | The filer usually keeps property, but nonexempt equity may increase the plan payment. |

| Mortgage or Car Loan Arrears | Chapter 7 does not create a long-term plan to catch up on missed payments. | Chapter 13 may allow missed payments to be caught up over time. |

| Biggest Advantage | Faster relief and a discharge of many qualifying debts without a multi-year repayment plan. | More time and flexibility to protect property, catch up on important payments, and deal with secured debts. |

Use the Chapter 7 vs. Chapter 13 decision tool below to walk through the practical questions that often matter in a real bankruptcy review: Are you behind on your mortgage or car loan? Do you have property that may not be fully protected? Is your income a possible Chapter 7 problem?

Chapter 7 vs Chapter 13 Decision Tool

Answer a few questions to get an educational estimate of which bankruptcy chapter may fit your situation.

Step 1 of 2

Window 1 of 2: Income Snapshot

ZIP lookup is optional and used as a quick state check.

This tool is for educational purposes only and is not legal advice.

When Is Chapter 7 Bankruptcy a Better Option Than Chapter 13?

Most of Your Debt Is Unsecured

Chapter 7 is often a good fit when the debt problem is mostly credit cards, medical bills, personal loans, old utility bills, or collection accounts. If there are no major property or income issues, Chapter 7 provides a faster path to relief.

Your Property Is Protected by Exemptions

The key question is not whether you own property. The key question is whether the property is protected by bankruptcy exemptions. Someone with ordinary household goods, a modest vehicle, and no significant nonexempt equity typically has less property risk in Chapter 7.

You Do Not Have Room for a Repayment Plan

If there is no realistic room in the budget for a monthly bankruptcy plan payment after covering rent, groceries, and basic living expenses, Chapter 7 usually makes more sense than Chapter 13.

Legal Sources: The law behind Chapter 7 and Chapter 13 is found in 11 U.S. Code Chapter 7 and 11 U.S. Code Chapter 13.

What Qualifies You to File Chapter 7 Bankruptcy?

One of the first questions people ask about Chapter 7 is simple: “Do I qualify?” The honest answer is that income matters, but it is not always as simple as being above or below one number. Household size, state median income, allowed expenses, secured debt payments, and tax deductions can all affect the result.

That is why we built the Chapter 7 means test calculator below. Instead of making you read through pages of means test rules, the calculator walks you through the major inputs commonly used to estimate Chapter 7 eligibility.

Chapter 7 Means Test Calculator

Estimate whether your household income is above or below your state’s median income for educational planning.

Educational estimate only. This Chapter 7 means test calculator is not legal advice, does not create an attorney-client relationship, and cannot account for every legal nuance. Attorney review may still be necessary.

Step 1: Initial Screening

If filing alone, household starts at 1. If filing jointly, household starts at 2. Add only additional dependents here.

Consumer debts are usually personal, family, or household debts.

Median-income dataset effective April 1, 2026. IRS/local standards preset date: Configurable - update with current IRS + USTP data. Presumption thresholds: $10,025 and $16,700 (60-month).

This calculator is for educational purposes only and is not legal advice. It provides an estimate based on the information entered and does not replace a full review by a bankruptcy attorney.

Other Chapter 7 Requirements Still Matter

Passing the means test is important, but it is not the only issue. You must also:

- Complete an approved credit counseling course within 180 days before filing.

- Ensure prior bankruptcy cases do not affect your ability to receive a discharge (e.g., usually waiting 8 years after a previous Chapter 7 discharge).

- Make sure there are no unprotected property transfers or asset risks.

Why Are Bankruptcy Exemptions Important in Chapter 7 Bankruptcy?

Bankruptcy exemptions determine what property you can protect. This is a critical part of Chapter 7 because the trustee is allowed to review your assets and, in some cases, sell property that is not protected by an exemption.

The exemptions available to you usually depend on where you live and how long you have lived there. Bankruptcy is a federal court process, but exemption rules vary by state. Attorney Insight: Exemptions should be reviewed before the case is filed. Once a Chapter 7 case is filed, it may be too late to fix an exemption problem without creating additional risk.

How to File for Chapter 7 Bankruptcy

1. Review Whether Chapter 7 Is the Right Fit

Ensure Chapter 7 aligns with your goals. It may need closer review if you are behind on a mortgage, own valuable property, or recently transferred assets.

2. Complete the Required Credit Counseling Course

This course must usually be completed within 180 days before filing. This is a strict filing requirement.

3. Prepare the Bankruptcy Petition and Schedules

These forms disclose your income, expenses, debts, property, exemptions, and recent financial history. They are signed under penalty of perjury, so accuracy is critical.

4. File the Case and Get the Automatic Stay

Once filed, the automatic stay goes into effect, halting most collection actions, lawsuits, and garnishments.

5. Attend the 341 Meeting of Creditors

The 341 meeting is usually the only required appearance. The trustee places the filer under oath and asks questions about the bankruptcy paperwork and financial history.

6. Receive the Chapter 7 Discharge

After completing a final debtor education course, the court will enter a discharge order, eliminating your legal obligation to pay many qualifying debts.

How Chapter 7 Affects Your Credit

A Chapter 7 bankruptcy can remain on your credit report for up to 10 years from the filing date. That does not mean you are locked out of credit for 10 years. It means future lenders may see the bankruptcy and consider it when deciding whether to approve credit.

The bigger question is often what your credit looks like without bankruptcy. If debts continue to go unpaid, collections, judgments, and garnishments may keep causing damage. Chapter 7 can hurt your credit, but it can also stop the cycle of unpaid debt that is already pulling your financial life down.

How Much Does It Cost to File Chapter 7 Bankruptcy?

Court Filing Fee & Courses

The court filing fee for a Chapter 7 case is currently $338. If you cannot pay the full fee at once, the court may allow installments or a fee waiver for low-income filers. You will also pay for the two required credit counseling courses (usually around $10 to $50 each).

Chapter 7 Attorney Fees

Attorney fees vary by location and case complexity. In many straightforward consumer Chapter 7 cases, attorney fees commonly fall somewhere around $1,500 to $2,500. The cheapest option is not always the safest option when dealing with your assets and future discharge rights.

Explore More National Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin