Understanding Bankruptcy Laws in Michigan

At a Glance: Bankruptcy in Michigan

- Automatic stay can stop garnishments, shutoffs, and repossessions.

- Choose one: Michigan or federal exemptions (no mixing).

- Eastern vs. Western District affects procedure and trustee.

- Chapter 7 = faster relief; Chapter 13 = catch-up & asset protection.

- Filing fees fixed; attorney fees vary by complexity/chapter.

- 341 meeting usually remote in MI; creditors rarely appear.

- On-time payments + low utilization can improve scores within months.

- Consult an experienced Michigan bankruptcy lawyer.

Immediate Protection: Why Timing Matters

Filing bankruptcy in Michigan can stop collections immediately through the automatic stay—crucial if you’re facing a Detroit-area wage garnishment, a shutoff notice from DTE or Consumers Energy, or a looming auto repossession. Acting quickly matters: every paycheck, utility bill, and day without protection can change your options.

Michigan vs. Federal Exemptions: Your First Big Choice

Michigan residents face a mix of federal rules and Michigan-specific choices that meaningfully affect outcomes. Unlike some states, Michiganders may choose either the federal exemptions or Michigan's own exemptions set—an early strategic decision that can determine how much home equity, vehicle value, or personal property you keep.

Which District Handles Your Case?

Where you file also matters. Michigan is split into two federal bankruptcy districts with distinct courthouses and trustee panels: the Eastern District (serving communities such as Detroit, Flint, Ann Arbor, and Bay City) and the Western District (serving Grand Rapids, Kalamazoo, Lansing, and the Upper Peninsula). Your residence controls the venue, meeting location, and local procedures you’ll follow.

Chapter 7 vs. Chapter 13: Picking the Right Path

Most individuals file under one of two chapters. Chapter 7 targets fast relief from unsecured debt when income and assets are limited. Chapter 13 builds a structured repayment plan—often used to catch up on mortgages or car loans while keeping property. The right fit depends on your income, assets, and goals.

Expect costs as you plan—but also prioritize qualified counsel. Bankruptcy is a niche area, and working with an experienced Michigan bankruptcy lawyer can be the difference between protecting assets and losing them. A local attorney will navigate means-test calculations, select between Michigan and federal exemptions, apply district-specific procedures in the Eastern or Western District, and avoid pitfalls that can delay discharge or jeopardize your home, vehicle, or wages.

This guide walks you step-by-step through how Michigan cases actually unfold—from filing and the 341 meeting to local court practices—so you can move decisively and protect what matters most.

What Is Bankruptcy? An Overview for Michigan Residents

Bankruptcy in Michigan is a legal tool designed to stop the bleeding fast—halting wage garnishments (often up to 25% of take-home pay), pausing lawsuits from Detroit to Grand Rapids, and even preventing utility shutoffs from providers like DTE or Consumers Energy. It offers immediate relief and a path to reset finances for both individuals and Michigan businesses.

For Michigan residents, the basics matter because local details shape outcomes. Once you file, the automatic stay forces most creditors to pause collections, giving you breathing room. Your case will run through either the Eastern District (serving communities such as Detroit, Flint, Ann Arbor, and Bay City) or the Western District (serving Grand Rapids, Kalamazoo, Lansing, and the Upper Peninsula), each with its own trustees and procedures.

When considering bankruptcy, it’s important to know your options. Most individuals choose between chapter 7 (quick relief from unsecured debt when income and assets are limited) and chapter 13 (a structured repayment plan to catch up on mortgages or car loans while keeping property). Michigan filers also make an early strategic choice between Michigan’s exemption set and the federal exemptions—an election that can affect how much home equity, vehicle value, and personal property you keep.

Key aspects of bankruptcy include:

- Halting creditor harassment.

- Providing a structured debt solution.

- Offering a financial fresh start.

Despite the benefits, bankruptcy has long-term effects on your credit and future borrowing. Weigh the relief against the consequences and timing—especially if you’re facing garnishment, foreclosure timelines, or a pending repossession.

In Michigan, professional guidance is critical. An experienced Michigan bankruptcy lawyer will help you choose the right chapter, select between Michigan and federal exemptions, and navigate district-specific procedures so you protect your home, vehicle, and wages.

Overview: Chapter 7 and Chapter 13 Bankruptcy in Michigan

This section is only a high-level overview of how chapter 7 and chapter 13 work in Michigan. For in-depth, always up-to-date guides, please see our dedicated pages: Chapter 7 Bankruptcy in Michigan and Chapter 13 Bankruptcy in Michigan. Those pages are your primary resources for chapter-specific details, trustee practices, and examples.

When filing for bankruptcy in Michigan, understanding the types available is essential. Most consumer cases in the Eastern District (Detroit, Flint, Ann Arbor, Bay City) and Western District (Grand Rapids, Kalamazoo, Lansing, Marquette/UP) proceed under chapter 7 or chapter 13, and the right choice can determine whether you keep your car, protect home equity, and how fast you get relief.

Chapter 7 provides quick relief from qualifying unsecured debts, with a trustee reviewing assets and any non-exempt equity. It involves selling non-exempt assets for the benefit of creditors under a court-appointed trustee, with “property of the estate” defined by federal law and narrowed by exemptions you claim (11 U.S.C. §§ 541, 704, 726). Once complete, remaining qualifying unsecured debts are discharged (11 U.S.C. § 727). It’s a relatively swift process in Michigan—often a few months from filing to discharge— assuming there are no asset sales or objections. For a deeper dive into Michigan-specific chapter 7 strategy, visit our Chapter 7 Bankruptcy in Michigan guide.

A means test decides eligibility for chapter 7 by comparing your household income to Michigan’s median and then applying allowed deductions (11 U.S.C. § 707(b)(2)). If your income is below the state median (per the U.S. Trustee’s Michigan figures) or your deductions show little to no disposable income, you may qualify. Michigan filers also face an early strategic choice: elect Michigan’s exemption scheme (MCL 600.5451, plus other state provisions) or the federal exemptions (11 U.S.C. § 522(d))—a decision that can impact home equity, vehicle value, tools of the trade, and personal property you keep.

Chapter 13, in contrast, focuses on repayment. You keep assets and make plan payments over three to five years to catch up on mortgage arrears, cure car loan defaults, or manage tax debts while protected by the automatic stay (11 U.S.C. §§ 362, 1322(b), 1325). Plan length and confirmation standards are set by federal law (e.g., 11 U.S.C. § 1322(d) for 3–5 year terms), and eligibility is governed by 11 U.S.C. § 109(e). Many Michigan homeowners use chapter 13 to stop a sheriff’s sale and spread arrears over time, subject to the local practices of their district and assigned trustee. For more detail on how this works in practice, see our Chapter 13 Bankruptcy in Michigan page.

Key differences between chapter 7 and chapter 13 include:

- Chapter 7: Quick discharge, potential liquidation of non-exempt assets, income-based eligibility via the means test (11 U.S.C. § 707(b)).

- Chapter 13: Longer repayment, asset retention, court-approved plan with confirmation requirements (11 U.S.C. § 1325) and typical 3–5 year term (11 U.S.C. § 1322(d)).

Choosing between these chapters depends on personal circumstances—income stability, arrears on a home or car, recent garnishments in places like Detroit or Grand Rapids, and which exemption set (Michigan or federal) preserves more value. Consulting with an experienced Michigan bankruptcy lawyer ensures your chapter selection, exemption election, and district-specific procedures align with your goals and the law cited above. You can learn more about the differences between chapter 7 and chapter 13 here, and then drill down into our dedicated Chapter 7 Bankruptcy in Michigan and Chapter 13 Bankruptcy in Michigan guides for Michigan-specific details.

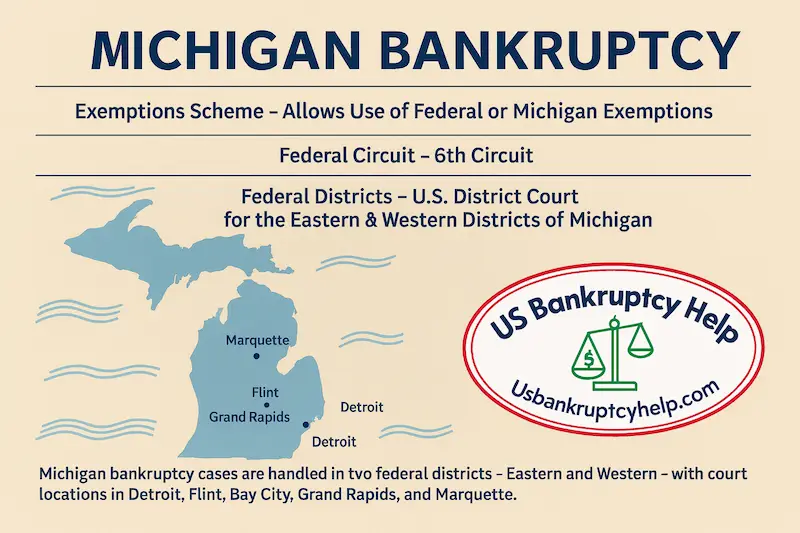

Michigan Bankruptcy Courts: Eastern and Western Districts

Michigan’s bankruptcy cases are heard in two federal districts created by Congress—the Eastern District and the Western District (28 U.S.C. § 102; 28 U.S.C. § 151). Your residence determines where you file, which trustee panel you’ll see, and the local procedures that apply, so getting the district right is critical for timing, venue, and the logistics of your 341 meeting (28 U.S.C. § 1408).

Eastern District of Michigan

This district handles a large share of the state’s consumer filings and covers populous communities such as Detroit, Flint, Ann Arbor, and Bay City. Cases are administered by Eastern District bankruptcy judges and trustees familiar with high-volume wage-garnishment and auto-loan matters common in Southeast Michigan.

Western District of Michigan

This district serves Grand Rapids, Kalamazoo, Lansing, and the Upper Peninsula (including Marquette). Local practice reflects a distinct geography—with cases frequently involving small-business debt, seasonal employment, and rural homestead considerations—administered by Western District bankruptcy judges and trustees.

Key differences between the districts include:

- Eastern District: Serves Detroit, Flint, Ann Arbor, Bay City; historically higher filing volume and busier dockets.

- Western District: Covers Grand Rapids, Kalamazoo, Lansing, Marquette/UP; distinct local procedures and trustee practices.

Michigan Bankruptcy Court Locations & Contacts

| District | Courthouse / City | Street Address | Clerk’s Phone | Website |

|---|---|---|---|---|

| Eastern | Detroit | U.S. Bankruptcy Court, 211 West Fort Street, Detroit, MI 48226 | (313) 234-0065 | mieb.uscourts.gov |

| Eastern | Flint | U.S. Bankruptcy Court, 226 West Second Street, Flint, MI 48502 | (810) 235-4126 | mieb.uscourts.gov |

| Eastern | Bay City | U.S. Bankruptcy Court, 111 First Street, Bay City, MI 48708 | (989) 894-8840 | mieb.uscourts.gov |

| Western | Grand Rapids (Clerk’s Office) | US Bankruptcy Court, 1 Division Ave N, Room 200, Grand Rapids, MI 49503 | (616) 456-2693 | miwb.uscourts.gov |

| Western | Marquette | US Bankruptcy Court, 202 West Washington Street, 3rd Floor, Marquette, MI 49855 | (616) 456-2693 | miwb.uscourts.gov — Marquette |

| Western | Kalamazoo (Not Staffed) | US Courthouse & Federal Building, 410 West Michigan, Room 114, Kalamazoo, MI 49007 | (616) 456-2693 | miwb.uscourts.gov — Kalamazoo |

| Western | Lansing (Not Staffed) | US Post Office & Federal Courthouse, 315 West Allegan Street, Room 101, Lansing, MI 48933 | (616) 456-2693 | miwb.uscourts.gov — Lansing |

| Western | Traverse City (Not Staffed) | Logan Place West, 3249 Racquet Club Drive, Traverse City, MI 49684 | (616) 456-2693 | miwb.uscourts.gov — Traverse City |

Filing in the correct district ensures proper venue and smoother administration (28 U.S.C. § 1408). Verify your district by home address before filing—this controls your courthouse, trustee assignment, and where your 341 meeting will be held. An experienced Michigan bankruptcy lawyer can confirm venue and prepare you for any district-specific requirements that affect exemptions, plan confirmation, or case timing.

The Bankruptcy Filing Process in Michigan

General overview (not legal advice): The steps below outline how bankruptcy in Michigan typically unfolds, but the process differs in important ways between chapter 7 and chapter 13. Because timing, exemptions, and local procedures in the Eastern vs. Western District can materially change your outcome, work with an experienced Michigan bankruptcy attorney to tailor each step to your situation.

1) Pre-filing counseling. Before you file, you must complete credit counseling with a U.S. Trustee–approved provider (11 U.S.C. § 109(h)). An attorney will help you choose the right timing, gather documents, and decide whether Michigan or federal exemptions better protect your assets.

2) File the petition and schedules. Your case begins when you submit the bankruptcy petition, schedules, and statements detailing income, expenses, assets, and debts. Accuracy is critical—errors can delay your case or draw objections. In chapter 7, eligibility hinges on the means test calculus (11 U.S.C. § 707(b)); in chapter 13, you’ll also propose a plan and confirm eligibility under 11 U.S.C. § 109(e).

3) Automatic stay takes effect. Filing triggers the automatic stay, which generally stops garnishments, foreclosures, repossessions, and lawsuits (11 U.S.C. § 362). In chapter 13, the stay also protects you while you catch up on mortgage or auto arrears through plan payments; in chapter 7, the stay remains while the trustee reviews your estate and exemptions.

4) 341 meeting of creditors. You’ll attend a brief, recorded meeting run by the trustee (11 U.S.C. § 341). You answer questions under oath about your petition and documents. Local trustee practices vary by district; counsel will prepare you for what to expect in Detroit/Flint/Bay City (Eastern) versus Grand Rapids/Kalamazoo/Lansing/UP (Western).

5) Education requirement. After filing, complete a debtor-education/financial-management course to be eligible for discharge (e.g., 11 U.S.C. § 727(a)(11) for chapter 7; § 1328(g) for chapter 13).

Here’s a brief checklist for the process:

- Complete credit counseling with an approved provider (pre-filing).

- File the petition and required schedules in the correct Michigan district.

- Automatic stay begins; comply with trustee document requests.

- Attend the 341 meeting of creditors and verify all information.

- Finish the post-filing debtor-education course and obtain discharge (if eligible).

Documentation & timelines differ by chapter. Chapter 7 cases in Michigan commonly finish in a few months if no objections arise; the trustee administers any non-exempt property and the court enters discharge (11 U.S.C. § 727). Chapter 13 adds plan confirmation and monthly payments over three to five years (11 U.S.C. § 1322(d), § 1325), often used to cure mortgage arrears or protect vehicles while staying current. An attorney will calibrate chapter selection, exemption elections, and local rules to protect your home, wages, and car.

Bottom line: Treat this as a roadmap, not a DIY guide. Michigan bankruptcy is nuanced, and early choices—chapter, timing, exemptions, and venue—have lasting consequences. A seasoned Michigan bankruptcy lawyer will help you move decisively and avoid costly mistakes.

Costs and Fees: How Much Does It Cost to File Bankruptcy in Michigan?

Michigan Bankruptcy Costs Overview

Understanding the costs associated with bankruptcy in Michigan is crucial—both the court costs and the attorney fees that drive most budgets. Court filing fees are fixed, but attorney fees vary with chapter, complexity, and the district (Eastern vs. Western) where your case is filed.

Court Filing Fees and Required Courses

Court costs (typical): filing fees of about $338 for chapter 7 and $313 for chapter 13, plus required courses (credit counseling and debtor education) that often total around $50–$100 combined.

Michigan Chapter 7 Attorney Fees

Attorney fees for chapter 7: many Michigan cases fall in the $1,500–$3,500+ range, depending on the facts. Some matters—especially business cases—can run much higher (tens of thousands of dollars) due to investigations, asset sales, or litigation. Factors that push fees to the higher end include:

- “Asset” cases (non-exempt equity in a home, vehicle, tools, or other property).

- Close calls on the means test or anticipated scrutiny from the U.S. Trustee.

- Potential creditor objections to discharge or dischargeability (adversary proceedings).

- Business ownership, recent transfers, insider payments, or complex tax issues.

- Extensive document workup (multiple bank accounts, side income, or inadequate records).

Michigan Chapter 13 Attorney Fees

Attorney fees for chapter 13: most Michigan cases fall roughly in the $3,500–$5,500 range, with complex plans reaching $10,000–$20,000 over the life of the case. Importantly, these fees are usually paid through your regular plan payments after a modest amount up front. Complexity (and cost) can increase when the case involves:

- Significant mortgage arrears, condo/HOA issues, or multiple properties.

- Car loan disputes (valuation, interest, or cramdown eligibility) or multiple vehicles.

- Priority and secured tax debts, domestic support obligations, or prior bankruptcies.

- Creditor plan objections seeking higher principal/interest or different treatment.

- Motions for relief from the automatic stay (e.g., mortgage or auto lenders) that must be defended.

- Business income, fluctuating earnings, or trustee-required budget adjustments.

Why Hire a Michigan Bankruptcy Attorney

Why hire a Michigan bankruptcy attorney: Michigan lawyers price cases to the work required in your district, and many follow court-approved fee guidelines in chapter 13. A seasoned Michigan bankruptcy lawyer will quote a fee structure up front, explain what’s covered, and help you avoid costly mistakes—choosing the right chapter, timing, and exemptions; preparing complete schedules; addressing trustee requests; and responding to creditor or U.S. Trustee objections.

Bottom Line on Bankruptcy Fees in Michigan

Bottom line: plan for the filing fee and courses, but focus on securing qualified counsel. The right attorney can often save you money—and protect assets—by preventing missteps that lead to objections, delays, or loss of property.

Michigan Exemptions

This section is a high-level overview of how exemptions work in Michigan. For a detailed, always up-to-date breakdown of exemption categories, dollar limits, statute citations, and examples, please see our dedicated guide that lists and explains Michigan bankruptcy exemptions in detail. That page is your primary resource for Michigan exemption charts and strategy.

Michigan vs. Federal Exemptions

In a Michigan bankruptcy, you’ll choose one exemption system—either Michigan’s state exemptions (for example, MCL 600.5451 and related provisions) or the federal exemptions (11 U.S.C. § 522(d)). You can’t mix and match. That election, usually made with the help of counsel, determines how much equity you can protect in a home, vehicle, tools of the trade, household goods, and other essentials. The Michigan Bankruptcy Exemptions page walks through these categories side by side so you can see how the systems compare.

Why This Choice Matters

Michigan filers may elect the federal exemption set instead of the state set. The decision can swing outcomes by thousands of dollars and interacts with rules like the 730-day domicile requirement (11 U.S.C. § 522(b)(3)(A)) and the homestead timing cap (11 U.S.C. § 522(p)). Because practice varies between the Eastern and Western Districts, it is important to review your facts with an experienced Michigan bankruptcy lawyer and to consult the detailed charts on our Michigan Bankruptcy Exemptions guide before you file.

Strategy, Not Just Numbers

The best exemption strategy looks at your whole balance sheet. Work with your attorney to compare category by category—homestead, vehicle, personal property, wildcard, tools of the trade, retirement—and pick the set that shields the most value for your situation. Chapter choice also matters: exemptions protect assets from liquidation in chapter 7 and affect plan feasibility and best-interests tests in chapter 13. For a more granular, line-by-line discussion of these categories, head to the Michigan Bankruptcy Exemptions page.

- Citations (overview): 11 U.S.C. § 522(b), (d); § 522(b)(3)(A); § 522(p); § 522(b)(3)(B); MCL 600.5451.

The Role of the Bankruptcy Trustee and the 341 Meeting

Chapter 7 vs. Chapter 13 Trustee Roles in Michigan

The bankruptcy trustee is a pivotal figure in every Michigan case, but their role differs by chapter. In chapter 7, a panel trustee reviews your paperwork, verifies exemptions, and determines whether there are non-exempt assets to liquidate for creditors. In chapter 13, the standing trustee reviews your proposed repayment plan, recommends confirmation (or changes), collects monthly plan payments, and monitors compliance throughout the case.

Trustee Appointment and Case Oversight

Once you file, a trustee is appointed in your district (Eastern or Western) to examine your schedules, request documents, and ensure you comply with the Bankruptcy Code and local procedures. A core checkpoint is the “meeting of creditors,” commonly called the 341 meeting, where you answer questions under oath about your petition and financial history.

What To Expect at the 341 Meeting in Michigan

What to expect at the 341 meeting: Although it’s called a meeting of creditors, creditors rarely appear in routine consumer cases. In Michigan, attendance is usually conducted remotely (telephone or video) unless the court or trustee instructs otherwise. Your attorney will prepare you on the format used in your division and what documents to have handy.

Your Responsibilities at the 341 Meeting

During the 341 meeting, you must:

- Attend (typically by phone or video unless otherwise directed) and testify under oath

- Provide accurate information about your financial affairs and recent transactions

- Respond to questions about your bankruptcy petition, schedules, and supporting documents

Why Counsel Matters

Bottom line: Trustee objectives are chapter-specific—asset review and potential liquidation in chapter 7; plan feasibility, payments, and ongoing oversight in chapter 13. Proper preparation with an experienced Michigan bankruptcy lawyer helps you avoid surprises, satisfy trustee requests, and keep your case on track.

Credit Counseling and Debtor Education Requirements

Michigan Credit Counseling (Before You File)

Required by law (11 U.S.C. § 109(h)). Every Michigan filer must complete a brief credit-counseling “briefing” with a U.S. Trustee–approved agency within the 180 days before filing. It’s usually online or by phone and results in a certificate you’ll file with your petition. The session reviews your budget and any non-bankruptcy options (11 U.S.C. § 111), but it’s not legal advice—timing this step with your attorney can affect venue, exemptions, and the automatic stay.

- Must be from an approved provider for the Eastern or Western District of Michigan.

- Joint filers may attend together; reduced-fee or fee-waiver policies are available for low-income filers.

- Rare exceptions (exigent circumstances/incapacity) exist, but are strictly limited.

Debtor Education / Financial Management (After You File)

After your case is filed—and before discharge—you must complete a separate financial-management course covering budgeting, credit use, and long-term planning (11 U.S.C. § 727(a)(11) for chapter 7; § 1328(g) for chapter 13). You’ll file your completion certificate (e.g., Official Form 423 in chapter 7) by the court’s deadline; missing it can delay or deny discharge.

- Typically completed online/phone after the 341 meeting; some trustees encourage earlier completion in chapter 13.

- Covers practical tools: budgeting, rebuilding credit, and preventing future delinquencies.

- Use a U.S. Trustee–approved provider for Michigan; keep your receipt and certificate.

Chapter 7 vs. Chapter 13: Practical Differences

In chapter 7, you’ll usually take the post-filing course soon after the 341 meeting and file the certificate promptly to avoid discharge delays. In chapter 13, many filers complete the course earlier but discharge won’t enter until plan completion; keep documentation current throughout your 3–5 year plan.

Why Counsel Still Matters

These courses are mandatory, but they’re not a roadmap to strategy. An experienced Michigan bankruptcy lawyer will advise on the best timing (within the 180-day window), help you choose an approved provider, and ensure certificates and forms are filed correctly in your district to prevent avoidable hiccups.

Quick Checklist

- Complete pre-filing credit counseling within 180 days (11 U.S.C. § 109(h)); file the certificate.

- File your case; attend the 341 meeting (typically remote in Michigan unless instructed otherwise).

- Complete the post-filing debtor-education course; file the completion certificate by the deadline (11 U.S.C. § 727(a)(11) / § 1328(g)).

- Coordinate all timing and filings with your attorney to avoid discharge delays.

The Impact of Bankruptcy on Your Credit and Future Finances

How Bankruptcy Shows Up on Credit Reports

Bankruptcy in Michigan is a reset—not a lifetime sentence. A chapter 7 can appear on your credit report for up to 10 years and a chapter 13 for up to 7 years, but lenders weigh recent behavior heavily. Many Michiganders see scores start to recover within months when they build new positive history and avoid new delinquencies.

What Lenders Look For After Filing

Lenders care less about the word “bankruptcy” and more about what you’ve done since. They look for on-time payments, low credit utilization, stable income, and no new collections. A short, clean track record post-filing often matters more than the raw score alone.

A Practical 90-Day / 6-Month / 12-Month Playbook

- First 90 Days: Pull all three credit reports, dispute inaccuracies, and set up autopay for utilities, phone, and any reaffirmed or new accounts. Consider a secured card with a modest limit—make small charges and pay in full.

- Next 6 Months: Keep utilization under ~10–20% of available credit, never miss a due date, and add only one additional starter tradeline if needed (e.g., a credit-builder loan through a Michigan credit union).

- By 12 Months: Ask for a secured-to-unsecured graduation or a small limit increase based on spotless history. Maintain emergency savings so you don’t rely on credit for surprises.

Michigan-Specific Ways To Rebuild

Leverage local institutions that understand community banking. Many Michigan credit unions offer credit-builder loans and starter cards with fair terms, and on-time auto/insurance payments can help stabilize your profile in a state where transportation is essential. If you commute in the Detroit metro or West Michigan, a reliable, affordable vehicle with on-time payments can add positive data quickly.

Mortgages, Auto Loans, and Renting After Bankruptcy

Access to credit returns in stages. Some auto lenders will work with recent filers who demonstrate steady income and a sensible down payment. Landlords commonly verify income and recent payment history more than they fixate on an old filing. Mortgage programs have “seasoning” periods that vary by product and chapter—your attorney or loan officer can map the options once you’ve built 12+ months of clean history.

Habits That Move Your Score Up

- Pay every bill on time—set autopay and calendar reminders.

- Keep credit utilization low (aim for ~10–20% of limits).

- Avoid applying for multiple new accounts at once.

- Monitor reports quarterly and dispute any errors promptly.

- Build cash reserves to prevent new late payments or high-interest borrowing.

Alternatives to Bankruptcy in Michigan

A Brief, Attorney-Led Overview

Bankruptcy isn’t the only path, but it’s often the most reliable legal remedy when you’re facing Michigan realities like 25% wage garnishment, repo threats, or a pending sheriff’s sale. If you’re exploring options, do it with an experienced Michigan bankruptcy lawyer so you don’t trade short-term relief for long-term risk.

When Non-Bankruptcy Options May Help

- Nonprofit Credit Counseling / DMP: A structured plan to lower rates and consolidate unsecured cards into one payment. Good payment history helps credit recovery; doesn’t stop lawsuits or garnishments already in motion.

- Direct Negotiation / Settlements: Case-by-case lump-sum or installment settlements with individual creditors. Useful when debts are limited and you can fund offers; taxable “forgiven” amounts and lawsuit risk remain during negotiations.

- Refi / Consolidation Loans: May reduce interest if you qualify, but adds secured risk if you roll debt into a home or vehicle—and won’t fix unaffordable balances.

- Short-Term Hardship Arrangements: Temporary forbearance or reduced payments after a job loss or medical event; best for brief income dips.

Red Flags With For-Profit “Debt Relief”

- High upfront fees or advice to stop paying all creditors (lawsuits/garnishments often follow).

- Promises of guaranteed results or “one-size-fits-all” plans.

- No written disclosures about taxes, litigation risk, or creditor opt-outs.

Why Many Michiganders Still Choose Bankruptcy

- Immediate protection: The automatic stay can stop garnishments, repossessions, and lawsuits.

- Predictable endpoint: Chapter 7 discharges eligible debts in months; chapter 13 provides a court-enforced plan.

- Asset strategy: Michigan vs. federal exemptions (chosen with counsel) to protect home/vehicle equity.

Best Practice: Compare Paths With Counsel

Have a Michigan bankruptcy attorney evaluate your debts, income, assets, and timelines. If a nonprofit debt-management plan or targeted settlement truly beats a chapter 7 or chapter 13 outcome, your lawyer will tell you—and help you avoid companies that put fees ahead of your interests.

Frequently Asked Questions About Bankruptcy in Michigan

Bankruptcy can feel overwhelming. These Michigan-focused FAQs give you practical answers and next steps—without replacing advice from an experienced Michigan bankruptcy lawyer.

How long will bankruptcy stay on my credit report?

A chapter 7 can appear for up to 10 years; a chapter 13 for up to 7. Many Michiganders see meaningful improvement sooner by paying on time, keeping utilization low, and adding positive tradelines (e.g., a secured card or credit-builder loan through a Michigan credit union).

Will I lose my house or car in Michigan?

Most filers keep essential property. You’ll elect one exemption system—Michigan’s state exemptions or the federal set—and apply them strategically to home and vehicle equity. In chapter 13, you can also use a repayment plan to cure mortgage or auto arrears while protected by the automatic stay. The best approach depends on equity, loan status, and which exemption set protects more value in your district.

What’s the real difference between chapter 7 and chapter 13?

- Chapter 7: Faster discharge of eligible unsecured debts; trustee reviews assets and non-exempt equity.

- Chapter 13: Court-approved repayment plan (usually 3–5 years) to catch up on secured debts and manage taxes while keeping assets.

Do creditors actually show up at the 341 meeting?

Rarely in routine consumer cases. Your “meeting of creditors” is typically brief and, in Michigan, usually held by phone or video unless otherwise instructed. You’ll verify ID, swear an oath, and answer the trustee’s questions about your petition and documents.

Can student loans be discharged?

It’s possible but not automatic. You must file a separate lawsuit in your case (an adversary proceeding) and prove “undue hardship” under controlling law in the Sixth Circuit. Outcomes are highly fact-specific—discuss this with your attorney before filing.

Do both spouses have to file together?

No. Many Michigan couples file jointly for efficiency, but you can file individually. Consider whose debts are involved, how title is held (including potential tenancy-by-the-entirety issues for a home), and how exemptions will apply before deciding.

Will bankruptcy stop a wage garnishment or a pending repo/foreclosure?

Yes—filing triggers the automatic stay, which generally stops most collections immediately, including a 25% wage garnishment, repossessions, and mortgage actions. Timing matters: file early enough to protect paychecks and property.

What happens to my tax refunds?

Refunds are assets. In chapter 7, part or all of a refund may need to be exempted; in chapter 13, refunds can affect plan funding depending on your trustee’s policies. Bring prior returns and current withholdings to your consult so your attorney can plan around them.

How soon can I rebuild credit or get a car/mortgage?

Credit rebuilding starts immediately after filing: on-time payments and low utilization drive results. Some auto lenders work with recent filers who show steady income. Mortgage seasoning periods vary by program and chapter—your attorney or loan officer can map a timeline once you’ve built 12+ months of clean history.

What documents should I gather before filing in Michigan?

- Photo ID and Social Security evidence

- Last 6+ months of pay stubs or income proof (longer for self-employed)

- Recent tax returns (usually last two years)

- Bank statements, titles, deeds, retirement and insurance account statements

- Mortgage, car loan, collection, judgment, and garnishment paperwork

How do I start the bankruptcy process in Michigan?

Begin with a consult. Your attorney will confirm venue (Eastern or Western District), analyze chapter options, and time your filing. You’ll complete pre-filing credit counseling with a U.S. Trustee–approved provider, then your lawyer files the petition and schedules and prepares you for the 341 meeting.

Key Takeaways

- Most Michiganders keep a home and vehicle with the right chapter and exemption strategy.

- The automatic stay can immediately halt garnishments, repossessions, and lawsuits.

- Credit can rebound with on-time payments, low utilization, and a sensible credit mix.

- An experienced Michigan bankruptcy lawyer is essential for chapter selection, exemption elections, timing, and district-specific procedure.

Michigan Bankruptcy Success Stories

Real client scenarios are anonymized and for illustration only. Results vary. Speak with an experienced Michigan bankruptcy lawyer about your specific facts.

Chapter 7 in Detroit: Stopping a 25% Wage Garnishment

“Marcus,” a Detroit manufacturing tech, was losing 25% of each paycheck to a judgment garnishment while juggling high-interest credit cards and a repossession threat on a second vehicle he no longer owned. After reviewing means-test numbers and choosing the federal exemption set, he filed chapter 7. The automatic stay stopped the garnishment immediately, unsecured debts were discharged in a few months, and he rebuilt with a secured card through a Michigan credit union—on-time payments and low utilization helped his score rebound within the first year.

Chapter 13 in Grand Rapids: Saving a Home From a Sheriff’s Sale

“Sara and Luis,” homeowners in Kent County, fell behind on the mortgage after a medical leave. With a sheriff’s sale scheduled, they used chapter 13 to halt the sale, spread arrears over 60 months, and keep their car by addressing past-due payments inside the plan. Their attorney structured a realistic budget, responded to a creditor’s plan objection, and secured confirmation. They finished credit counseling and financial-management courses, stayed current on plan payments, and kept the home.

Small Business Wind-Down in Ann Arbor: Clean Exit and Restart

“Nadia,” a café owner near campus, decided to close after a certain rivalry Saturday when scarlet-and-gray visitors turned The Big House into a tough house—plus rising supply costs and lease pressure. With personal guarantees, recent equipment sales, and mixed tax debts in the picture, a chapter choice analysis pointed to chapter 7. With careful exemption planning and full disclosure, the trustee administered a small non-exempt asset and unsecured debts were discharged. Nadia rebuilt with a credit-builder loan and a modest secured card while transitioning to a salaried hospitality role.

Why These Stories Matter for Michigan Filers

Across Eastern and Western Districts, chapter 7 can deliver fast relief from unsecured debt and garnishments, while chapter 13 can protect homes and vehicles by curing arrears over time. The right outcome turns on timing, exemption elections (Michigan vs. federal), and local trustee practices—areas where an experienced Michigan bankruptcy lawyer makes the difference.

Is Bankruptcy the Right Choice for You?

Bankruptcy in Michigan is a strategic legal reset—not a last resort. The question isn’t simply “should I file,” but when, under which chapter, and with which exemption set to protect the most value. The right timing and strategy can stop garnishments, pause foreclosures and repossessions, and position you to rebuild quickly.

When Bankruptcy Makes Sense in Michigan

- Wage garnishment (often up to 25%) or active lawsuits are draining cash flow.

- Mortgage arrears or a scheduled sheriff’s sale require a court-enforced plan.

- High-interest unsecured debt is growing faster than you can repay.

- Your asset mix favors a smart exemption election (Michigan vs. federal) to keep home/vehicle equity.

Choosing the Right Path: Chapter 7 vs. Chapter 13

Chapter 7 seeks fast discharge when income and assets are limited; a trustee reviews non-exempt property and exemptions. Chapter 13 builds a 3–5 year plan to cure arrears and protect assets while you make affordable payments. Your residence determines venue—Eastern or Western District—and local trustee practices and timelines vary. An experienced Michigan bankruptcy lawyer will map your options to district procedure.

Your Next Step

Talk to a Michigan bankruptcy attorney before you decide. In one consult, you can verify venue, run the means test, compare exemption sets, and choose the chapter that best protects your home, wages, and vehicle—so you file once, correctly, and start rebuilding with confidence.

Explore Our Michigan Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin