Chapter 13 Bankruptcy: What It Is, How It Works, and When It May Help

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

Legal Disclaimer

This article is for educational purposes only and does not constitute legal, tax, or financial advice. Reading this content does not create an attorney-client relationship. Bankruptcy laws and local court procedures vary significantly by jurisdiction. Always consult with a licensed bankruptcy attorney to evaluate your specific situation before filing.

Chapter 13 bankruptcy is a court-approved repayment plan for people who have a steady income. Instead of wiping out qualifying debts quickly like chapter 7 bankruptcy, Chapter 13 usually lets you pay back some or all of what you owe over three to five years. It’s especially helpful if you need to stop a foreclosure, catch up on a car loan, protect your property, deal with tax debt, or move forward with bankruptcy when Chapter 7 just doesn’t quite fit your situation.

Chapter 13 bankruptcy is a court-approved repayment plan for people who have a steady income. Instead of wiping out qualifying debts quickly like in Chapter 7, Chapter 13 usually lets you pay back some or all of what you owe over three to five years. It’s especially helpful if you need to stop a foreclosure, catch up on a car loan, protect your property, deal with tax debt, or move forward with bankruptcy when Chapter 7 just doesn’t quite fit your situation.

When Chapter 13 Bankruptcy May Make Sense

Chapter 13 is usually worth looking at when you need more than a quick discharge of unsecured debt. It may make sense when you need time to catch up, protect property, or use bankruptcy tools that chapter 7 does not provide.

Common situations where chapter 13 may be worth considering include:

- You are behind on your mortgage and want to stop foreclosure.

- You are behind on your car loan and want to avoid repossession.

- You have regular income but need a structured repayment plan.

- You have too much home, vehicle, or other property equity for chapter 7.

- You do not qualify for chapter 7 because of your income.

- You owe tax debt, domestic support arrears, or other debts that need special treatment.

- You filed bankruptcy before and chapter 7 may not be available right now.

These situations do not automatically mean chapter 13 is the right choice, but they are signs that a chapter 13 analysis may be worth doing before deciding what to file.

Chapter 13 Bankruptcy at a Glance

Chapter 13 bankruptcy is usually about time, structure, and protection. It helps people with regular income catch up on important debts, protect property, and deal with creditors through a court‑approved repayment plan.

- What it is: Chapter 13 is a federal bankruptcy process that allows individuals with regular income to propose a repayment plan under chapter 13 of the U.S. Bankruptcy Code.

- How long it usually lasts: Most chapter 13 repayment plans last three to five years, depending on income, plan requirements, and the debts that must be handled through the plan.

- How payments work: You typically make one monthly payment to a chapter 13 trustee, who distributes money to creditors under the court-approved plan.

- Why people use it: Chapter 13 may help stop foreclosure, stop repossession, catch up on missed mortgage or car payments, manage certain tax debts, or protect property that could be at risk in chapter 7.

- What filing can stop: Filing bankruptcy usually creates an automatic stay that pauses many collection actions under 11 U.S.C. § 362, although exceptions and limits may apply.

- What happens at the end: If you complete the repayment plan and meet all required obligations, certain remaining eligible debts may be discharged under 11 U.S.C. § 1328.

- The key question: Chapter 13 is not just about whether you can file. The real question is whether it solves the debt problem you actually have and whether the plan payment is realistic.

Should You File Chapter 7 or Chapter 13 Bankruptcy?

Many people who look into chapter 13 are also wondering whether chapter 7 might be a better fit. Chapter 7 is usually faster and does not involve a repayment plan. Chapter 13, on the other hand, may offer more protection if you are behind on a house, car, taxes, or other debts that need time and structure.

The table below gives a quick side-by-side comparison. It is not meant to decide the issue by itself, but it can help you see which chapter may better match the problem you are trying to solve.

| Category | Chapter 7 | Chapter 13 |

|---|---|---|

| Length of Case | Usually lasts a few months. | Usually lasts three to five years. |

| Repayment Plan | No repayment plan. | Requires a court-approved repayment plan. |

| Income Requirements | Income must fall below certain levels or pass means test. | Must have sufficient income to make plan payments. |

| Treatment of Property | Non-exempt property may be sold or settled by a trustee to pay creditors. | You may be able to keep nonexempt property, but the plan may need to pay creditors at least the amount required by bankruptcy law. |

| Catching Up on Missed Payments | No ability to cure mortgage or car arrears over time. | Allows the repayment of arrears over the life of the plan. |

| Best Suited For | People who need a faster discharge and do not need a long-term plan to catch up on secured debts. | Individuals with steady income who need time to reorganize debt. |

The right chapter depends on the problem you are trying to solve. Chapter 7 may be a better fit if your main goal is a faster discharge of qualifying unsecured debt and your property is protected. Chapter 13 may be a better fit if you need to stop foreclosure, catch up on a car loan, protect nonexempt property, or repay certain debts over time.

For a deeper comparison, see our guide on chapter 7 vs chapter 13 bankruptcy.

If you are not sure which chapter may fit your situation better, use the tool below to compare common decision points, including income, assets, secured debts, payment problems, and your main reason for considering bankruptcy. The tool is free to use, and you do not need to provide your name, email address, or phone number to see a result. You can also visit our chapter 7 vs chapter 13 decision tool page.

Chapter 7 vs Chapter 13 Decision Tool

Answer a few questions to get an educational estimate of which bankruptcy chapter may fit your situation.

Step 1 of 2

Window 1 of 2: Income Snapshot

ZIP lookup is optional and used as a quick state check.

What Is a Chapter 13 Bankruptcy Plan?

A chapter 13 plan is the court-approved plan for how your debts will be handled during the case. It explains how much you will pay each month, how long the plan will last, which debts must be paid in full, how secured debts such as a mortgage or car loan will be treated, and what may happen to qualifying unsecured debts at the end of the case.

The plan is important because chapter 13 does not work unless the payment is realistic and the plan satisfies bankruptcy rules. The court, trustee, and creditors can review the plan, and the court will confirm it only if it meets the legal requirements for approval.

In practical terms, the plan is where chapter 13 becomes personal. A person trying to stop foreclosure may need a plan that catches up missed mortgage payments. A person trying to keep a car may need a plan that properly handles the vehicle loan. A person with tax debt, support arrears, or nonexempt property may need a plan that accounts for those issues.

For example, a chapter 13 plan might:

- Let you catch up on missed mortgage payments over three to five years, while you keep making your regular monthly payment.

- Put your missed car payments into the plan so the lender doesn’t demand all of the past-due amount at once.

- Take care of certain tax debts or overdue support that bankruptcy law requires to be handled in a specific way.

- Allow you to keep property that would otherwise be nonexempt, as long as your plan pays creditors what the bankruptcy rules require.

- Pay only a portion of qualifying unsecured debts—like credit cards, medical bills, or personal loans—if your plan meets the legal requirements.

These are just examples, not guarantees. How a Chapter 13 plan will treat each of your debts depends on your income, expenses, property, exemptions, the types of debts you have, local practice, and whether the court ultimately approves (confirms) your plan.

If you want to see what a chapter 13 plan can look like, the U.S. Courts provides an official Chapter 13 Plan form. The form can help you understand the types of issues a plan may cover, but local bankruptcy courts may require different forms, local provisions, or district-specific procedures.

How Much Will Your Chapter 13 Plan Payment Be?

A chapter 13 plan payment is not based on a single formula. It usually depends on your income, reasonable living expenses, the kinds of debts you have, your property values, any missed mortgage or car payments, priority debts, attorney fees, trustee fees, and how long the plan will last.

In real world terms, your payment usually has to answer two questions: what can you realistically afford to pay each month, and what does bankruptcy law require your plan to pay? The answers can look different depending on your situation. For example, whether you are trying to catch up on a house, keep a car, pay tax debt, protect nonexempt property, or mainly deal with unsecured debts like credit cards and medical bills.

You can use our free chapter 13 plan payment calculator below to get an estimate of what a plan payment might look like. The tool is free to use, and you do not need to provide your name, email address, or phone number to see an estimate.

Chapter 13 Plan Payment Calculator

Chapter 13 plan payments depend on many factors, including local court and trustee practices. This tool gives an educational estimate only, not legal advice.

Median-income reference date: April 1, 2026.

Practitioner's Note: The Feasibility Test

After nearly two decades of reviewing Chapter 13 plans in practice, we consistently see that the most common reason a case fails isn't basic eligibility, it's feasibility. Bankruptcy trustees will aggressively scrutinize your proposed budget. If you submit a plan that leaves you with zero margin for error for unexpected expenses (like a car repair or medical bill), the court is likely to reject it. A successful plan requires a brutally honest assessment of your actual living expenses, not just a mathematical formula that looks good on paper.

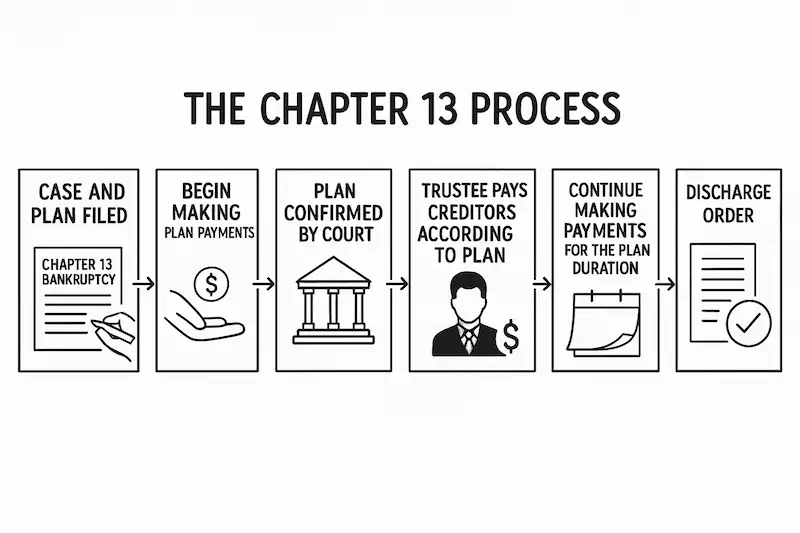

How Chapter 13 Bankruptcy Works

Chapter 13 moves through a court‑supervised process. Every case is a little different, and local court practices can vary, but most chapter 13 cases follow the same basic path: you file the case, get automatic stay protection, propose a repayment plan, go to a trustee meeting, seek plan confirmation, make payments, and then work toward completing the case and receiving a discharge.

1. Filing the Bankruptcy Case

A chapter 13 case begins when the bankruptcy petition is filed with the court. The filing usually includes schedules listing your income, expenses, assets, debts, recent financial activity, and other required information. A chapter 13 trustee is then assigned to administer the case.

The information filed with the court matters because it affects plan payments, property protection, creditor treatment, and whether the proposed plan can be approved.

2. The Automatic Stay Begins

When you file for bankruptcy, an automatic stay usually goes into effect. This legal protection can pause many collection efforts, such as lawsuits, wage garnishments, foreclosure steps, repossession efforts, collection calls, and most creditor lawsuits.

The automatic stay is one reason chapter 13 can be especially helpful in urgent situations. But it is not unlimited. Creditors can ask the court for permission to move forward in certain circumstances, and repeat filings, support obligations, criminal matters, and some other issues may be treated differently under the law.

3. You Propose a Chapter 13 Plan

The chapter 13 plan explains how your debts will be handled during the case. In many cases, the plan is filed with the petition or shortly after the case is filed. The plan may address mortgage arrears, car loans, tax debts, domestic support obligations, attorney fees, trustee fees, and unsecured debts such as credit cards, medical bills, and personal loans.

This is where chapter 13 becomes practical. The plan must be realistic enough for you to make the payments and legally sufficient for the court to approve.

4. You Start Making Plan Payments

Chapter 13 payments usually begin early in the case, often before the 341 meeting of creditors. Missing early payments can put the case at risk for dismissal.

Depending on your case and local practice, you may also need to stay current on ongoing mortgage payments, vehicle payments, insurance, tax filings, or domestic support obligations while the case is pending.

5. You Attend the Meeting of Creditors

You must attend a meeting conducted by the chapter 13 trustee, often called a 341 meeting or meeting of creditors. The trustee asks questions about your petition, income, expenses, assets, debts, and proposed plan. Creditors may attend and ask questions, although many do not.

The meeting is not usually held in a courtroom, but the questions are answered under oath. Accurate and complete information is important.

6. The Court Reviews the Plan for Confirmation

The court must decide whether the proposed plan meets the legal requirements for confirmation. The trustee or creditors may object if they believe the plan is not feasible, does not pay required debts correctly, does not account for nonexempt property, or otherwise fails to satisfy bankruptcy law.

If problems come up you may need to negotiate with creditors or amend the plan before it can be confirmed. Once the plan is confirmed, it becomes the controlling roadmap for how debts are handled during the case.

7. You Complete the Plan and Seek a Discharge

After the plan is confirmed, you continue making required payments for the length of the plan. Most plans last three to five years. If your income, expenses, or circumstances change during the case, you may need to seek a plan modification or other court-approved relief.

If you complete all required payments and satisfy the remaining bankruptcy requirements, the court may enter a discharge of eligible debts. If the plan is not completed, the case may be dismissed or, in some situations, converted to another bankruptcy chapter.

How Do You Know if Your Chapter 13 Plan Will Be Three or Five Years?

Most Chapter 13 plans last either three years or five years. A key factor is how your income compares to the median income in your state for a household your size.

You can use our median income calculator to get a quick sense of whether your income is above or below that median for your state and household size.

- If your income is below the median: your Chapter 13 plan may be allowed to last three years, unless you choose or need a longer plan.

- If your income is above the median: your Chapter 13 plan usually has to last five years, unless your unsecured creditors are paid in full sooner.

Plan length matters because it affects your monthly payment, how long you’re under the court’s supervision, and how much time you have to catch up on debts like mortgage arrears, vehicle arrears, taxes, and other required payments.

Eligibility Requirements for Chapter 13 Bankruptcy

Chapter 13 isn’t the right fit for everyone. To use Chapter 13, you generally need steady income, debts under the legal limits, required pre-filing credit counseling, and enough financial documentation to back up the plan you propose. Even then, meeting the basic rules is only step one. The court still has to decide whether your plan follows bankruptcy law and whether it realistically fits your income and expenses.

You Must Have Regular Income

Chapter 13 is meant for people who have regular income. That income can come from wages, self-employment, a small business, Social Security, a pension, rental income, or another consistent source.

In practical terms, the question is: after your normal living expenses, is there enough left over each month to make a Chapter 13 payment? If your income is irregular, seasonal, or uncertain, Chapter 13 may still work, but the court will look more closely at whether your plan is truly doable.

Your Debts Must Be Within the Chapter 13 Debt Limits

Chapter 13 also has debt limits. As of the current adjustment period beginning April 1, 2025, chapter 13 is generally available only if your debts are below these limits:

- Unsecured debts: less than $526,700

- Secured debts: less than $1,580,125

Unsecured debts usually include things like credit cards, medical bills, and personal loans — debts that aren’t tied to any specific property. Secured debts usually include mortgages, car loans, and other debts that are backed by property. These limits change from time to time, so they should be confirmed before you file.

Source: 11 U.S.C. § 109(e)

You Must Complete Credit Counseling Before Filing

Most people must complete an approved credit counseling course within 180 days before filing for bankruptcy. The course has to be taken from a provider approved for the district where your case will be filed.

You Need Complete and Accurate Financial Information

A Chapter 13 case requires full and accurate financial information. That usually includes your income, expenses, assets, debts, recent financial activity, tax returns, and any other documents the court, trustee, or local rules require.

Missing or incorrect information can slow down approval of your plan, trigger objections from the trustee, or even lead to dismissal of your case. This is especially important if you own a home or business, have tax debt, recently transferred property, or recently paid back family members.

Eligibility Does Not Guarantee Plan Approval

Even if you meet the basic eligibility requirements, the court may still reject your plan. The plan must follow bankruptcy rules, properly handle required debts, deal with any property issues, and be realistic based on what you actually earn and spend.

That’s why Chapter 13 is often less about whether you are allowed to file and more about whether the plan will actually work in real life. A plan that is too expensive, incomplete, or legally flawed can be denied, sent back for changes, dismissed, or converted to a different type of bankruptcy.

Types of Bankruptcy

Learn how chapter 7 and chapter 13 work and how each may address different types of debt.

What Chapter 13 Bankruptcy Can Help You Do

Chapter 13 gives you tools you usually don’t have outside of bankruptcy. It can help you pause certain collection actions, catch up on important debts, protect key property, and follow a court-supervised plan for dealing with creditors. How much it helps depends on your income, debts, assets, timing, and whether your plan meets the requirements of bankruptcy law.

Stop Foreclosure and Catch Up on Missed Mortgage Payments

If you’re behind on your mortgage, Chapter 13 may let you stop a foreclosure and pay back the missed payments over time through your plan. For many people, this is one of the biggest reasons to choose Chapter 13 instead of Chapter 7.

Timing and affordability are critical. Chapter 13 usually works best when you file before the foreclosure process goes too far and when you can afford both the plan payment and the ongoing mortgage payment that has to continue during the case.

Stop Repossession and Address Car Loan Arrears

Chapter 13 may help stop a vehicle repossession and move missed car payments into your plan. In some situations, Chapter 13 can also change certain loan terms, depending on how old the loan is, what the vehicle is worth, and other bankruptcy rules.

Not every car loan can be modified, and filing after repossession can make things more complicated. If keeping the vehicle is your goal, timing, insurance, the loan balance, the car’s value, and whether you can afford the plan all matter.

Protect Property That Could Be at Risk in Chapter 7

Chapter 13 can help if you have property that might be hard to protect in Chapter 7. In Chapter 7, nonexempt property can be sold or otherwise handled by the trustee. In Chapter 13, you may be able to keep that property, but your plan may have to pay creditors at least what bankruptcy law requires.

This comes up a lot with home equity, vehicle equity, valuable personal items, expected tax refunds, legal claims, or other assets that are not fully covered by exemptions.

Create One Court-Supervised Payment Structure

Instead of juggling lawsuits, collection accounts, payment demands, and constant calls, Chapter 13 gives you one structured, court-supervised repayment setup. You usually make one regular payment to the Chapter 13 trustee, and the trustee distributes the money to creditors under the terms of your confirmed plan.

That doesn’t mean every debt is treated the same way. Secured debts, priority debts, attorney fees, trustee fees, and unsecured debts can all be handled differently under the plan.

Pause Many Collection Actions

Filing Chapter 13 usually triggers an “automatic stay.” The automatic stay can pause many collection actions, including lawsuits, wage garnishments, collection calls, foreclosure steps, and repossession efforts.

The automatic stay is powerful, but it is not unlimited. Creditors can ask the court for permission to move forward in some situations, and certain kinds of actions are not completely stopped by bankruptcy. If you have filed multiple cases, that can also affect how much protection the stay provides.

Handle Certain Tax Debts and Priority Debts Over Time

Chapter 13 can help you manage some tax debts, domestic support arrears, and other priority debts through a structured repayment plan. Some of these debts must be paid in full through the plan. Others can be treated differently, depending on the type of debt and the details of your case.

This is one reason Chapter 13 can be useful even if your main concern is not wiping out credit cards or medical bills. The plan can create time and structure to deal with debts that need special treatment.

Protect Certain Co-Debtors in Consumer Cases

In some consumer debt cases, Chapter 13 may offer limited protection for co-signers or co-debtors through what is called the co-debtor stay. This can matter if someone else signed on a debt with you and you are trying to prevent that person from being immediately targeted by a creditor.

This protection has limits and the court can lift it in some situations. Still, it is an important difference between Chapter 13 and Chapter 7 in the right case.

Discharge Some Remaining Eligible Debts After Plan Completion

If you complete your Chapter 13 plan and meet the remaining requirements, certain eligible debts may be discharged at the end of the case. This can include remaining balances on some unsecured debts such as credit cards, medical bills, personal loans, and collection accounts.

Not every debt goes away. Certain taxes, domestic support obligations, most student loans (unless additional standards are met), and some other debts may survive the case. The final outcome depends on the type of debt and how it is treated under bankruptcy law.

What Chapter 13 Bankruptcy Cannot Do

Chapter 13 can be very helpful, but it doesn’t fix every debt problem. Before you file, it’s important to be clear about what Chapter 13 can’t do.

- It does not automatically make ongoing mortgage payments disappear. If you want to keep your home, you typically still need to stay current on your regular mortgage payments, unless your plan or a court order clearly says otherwise.

- It does not guarantee you’ll keep your house or car. Chapter 13 can help you catch up or change how some debts are paid, but your plan still must be affordable and must follow bankruptcy rules. If the numbers don’t work, you may not be able to keep certain property.

- It does not wipe out every tax debt. Some tax debts must be paid through the plan, and some may still be owed after bankruptcy. The result depends on the type of tax, when it became due, and other specific facts.

- It does not get rid of child support or alimony. Domestic support obligations almost always have to be paid. Chapter 13 may help you deal with past-due amounts, but it does not erase the obligation itself.

- It usually does not discharge student loans by itself. Most student loans require a separate hardship process before they can be discharged, and many are not discharged at all.

- It does not work if you cannot make the plan payments. If your plan is not realistic, the court may dismiss the case or require changes. Chapter 13 depends on you being able to make the required payments.

Can Chapter 13 Bankruptcy Help You Keep Your House?

Chapter 13 bankruptcy may help you keep your home if you’re behind on your mortgage, facing foreclosure, or need time to catch up on missed payments. In many cases, filing Chapter 13 can stop a foreclosure and give you a chance to repay the past-due amount through a court-approved repayment plan.

Chapter 13 usually does not erase the mortgage if you want to keep the house. Instead, it creates a structure for catching up on missed payments while you continue making your regular mortgage payment. This is one of the biggest differences between Chapter 13 and Chapter 7.

How Chapter 13 Can Help With Mortgage Arrears

If you’re behind on your mortgage, the past-due amount is often called “mortgage arrears.” Chapter 13 may let you spread those arrears over the length of your repayment plan, which is usually three to five years. That can make catching up more realistic than trying to pay the full past-due balance all at once.

For example, if you are $12,000 behind, a Chapter 13 plan may allow that amount to be paid over time through the trustee payment, while you keep making your normal mortgage payment going forward. The exact payment will depend on your income, expenses, mortgage status, other debts, and local bankruptcy practice.

The video below walks you through how Chapter 13 bankruptcy can help you pause a foreclosure and pay back missed mortgage payments (mortgage arrearage) through the Chapter 13 plan.

You Usually Need to Keep Paying the Current Mortgage

Chapter 13 can help with missed payments, but it usually does not remove the need to make your future mortgage payments if you want to keep the house. In many cases, you must stay current on the regular mortgage payment after filing, on top of the Chapter 13 plan payment.

If you fall behind again during the case, the lender may ask the bankruptcy court for permission to restart the foreclosure process. That’s why Chapter 13 tends to work best when the total payment is realistic from the start.

Home Equity Still Matters

Chapter 13 can sometimes protect a home that might be at risk in Chapter 7, but your home equity still matters. If your equity is not fully covered by your state’s homestead exemption, your Chapter 13 plan may need to pay unsecured creditors at least what they would have received in a Chapter 7 case.

In practical terms, Chapter 13 can sometimes help you keep a home with nonexempt equity, but that equity may increase how much you have to pay through the plan.

Timing Can Be Critical if Foreclosure Is Pending

If a foreclosure sale is already scheduled, timing is critical. Chapter 13 may stop the sale if the case is filed before the sale is completed, but waiting too long can limit your options. Foreclosure rules and sale procedures vary by state, so it’s important to get advice quickly if a sale date is coming up.

Chapter 13 can be a powerful tool for homeowners, but it is not automatic. Your plan must properly address mortgage arrears, ongoing payments, home equity, and any other required debts. If the plan is not affordable or does not meet legal requirements, the case may not succeed.

For a deeper look at this topic, see our guide on filing bankruptcy and keeping your house.

Can Chapter 13 Bankruptcy Help You Keep Your Car?

Chapter 13 bankruptcy may help you keep your car if you’re behind on payments, facing repossession, or need a structured way to deal with your vehicle loan. In many cases, filing Chapter 13 can stop a pending repossession and give you time to catch up on what you owe.

Chapter 13 can be especially helpful when you rely on your car for work, school, family responsibilities, medical appointments, or everyday transportation. But keeping the vehicle usually depends on timing, the loan balance, the car’s value, insurance, ongoing payments, and whether the plan you propose is affordable.

How Chapter 13 Can Help With Missed Car Payments

If you’re behind on a car loan, Chapter 13 may let you handle the missed payments through your repayment plan instead of requiring you to bring the loan fully current right away. This can give you breathing room if the lender is threatening repossession.

For example, if you’re several months behind, a Chapter 13 plan may allow those arrears to be paid over time while you keep making the payments required under the plan. The exact treatment depends on the loan terms, the vehicle, the car’s value, when you bought it, and local bankruptcy practices.

Chapter 13 May Stop Repossession if Filed in Time

Filing Chapter 13 usually creates an automatic stay that can pause repossession efforts. If the lender has not yet taken the vehicle, the automatic stay may prevent them from repossessing the car without first getting permission from the bankruptcy court.

Timing matters, though. If the car has already been repossessed, getting it back is often more complicated. It may depend on state law, how far along the lender is in the repossession or sale process, and how quickly the Chapter 13 case is filed.

Some Vehicle Loans May Be Restructured in Chapter 13

In some Chapter 13 cases, a vehicle loan can be restructured through the plan. Depending on your situation, this might include changing how the loan is paid, paying it through the trustee, adjusting the interest rate, or, in limited situations, reducing the secured portion of the debt to the car’s value.

This is sometimes called a "vehicle cramdown", but not every loan qualifies. The timing of the purchase, the type of vehicle, the loan documents, the value of the car, and how the car is used can all matter. If this could be important in your case, it should be reviewed carefully before you file.

You Usually Need to Maintain Insurance and Required Payments

Chapter 13 does not mean you can ignore the car loan or stop protecting the vehicle. If you want to keep the car, you usually need to keep required insurance in place and make whichever payments your plan or court order requires.

If payments are missed or insurance lapses, the lender may ask the court for permission to repossess the vehicle. Chapter 13 tends to work best when the way your car is handled in the plan is realistic and the total monthly payment fits your budget.

Vehicle Equity Still Matters

Vehicle equity can also affect a Chapter 13 case. If your car is worth more than what you owe and that equity is not fully covered by your state’s vehicle exemption or other available exemptions, your plan may need to pay unsecured creditors at least what they would have received in a Chapter 7 case.

This doesn’t always mean you’ll lose the car. In Chapter 13, you may still be able to keep it, but nonexempt equity can increase the amount that must be paid through the plan.

For a deeper look at this issue, see our guide on filing bankruptcy and keeping your car. You can also review our chapter 13 vehicle cramdown guide if you want to learn more about when a car loan may be modified in chapter 13.

Chapter 13 vs. Chapter 7: Key Differences

Chapter 7 and Chapter 13 both give you bankruptcy protection, but they are usually used for different kinds of problems. Chapter 7 is generally faster and is often used when your main goal is to wipe out qualifying unsecured debts like credit cards and medical bills. Chapter 13 usually takes longer, but it may be the better fit if you need time to catch up on a mortgage, protect a car, deal with tax debt, or keep property that might be at risk in Chapter 7.

- Chapter 7 is usually faster. Many Chapter 7 cases last only a few months. A Chapter 13 case usually runs three to five years.

- Chapter 13 includes a repayment plan. In Chapter 13, you follow a court-supervised repayment plan. Chapter 7 usually does not involve a long-term plan.

- Chapter 13 may help with arrears. It can sometimes help you catch up on missed mortgage or car payments over time instead of all at once.

- Chapter 13 may help protect nonexempt property. If you have property that might be at risk in Chapter 7, Chapter 13 may let you keep it by paying the required value to creditors through the plan.

- Chapter 7 may be better for a faster discharge. If your main issue is qualifying unsecured debt and your property is already protected by exemptions, Chapter 7 may be simpler and quicker.

For a deeper comparison, see our guide on chapter 7 vs chapter 13 bankruptcy. You can also use our chapter 7 vs chapter 13 decision tool if you want help comparing common decision points.

Common Chapter 13 Bankruptcy Mistakes

Chapter 13 can be a powerful tool, but it is also more complicated than many people expect. A mistake before or during the case can make the plan harder to confirm, increase the payment, put property at risk, or even lead to dismissal.

Waiting Too Long Before Foreclosure or Repossession

Chapter 13 may help stop a foreclosure or repossession, but timing is critical. If a foreclosure sale or vehicle sale has already taken place, your options may be much more limited. Waiting until the last minute can also make it harder to prepare accurate paperwork, put together a realistic plan, and respond to creditor objections.

Underestimating the Chapter 13 Payment

Many people focus on whether Chapter 13 can stop a particular creditor. The more important question is whether the monthly plan payment is actually realistic.

Your payment may need to cover things like:

- Mortgage arrears

- Car debt

- Tax debt

- Trustee fees and attorney fees

- Priority debts

- The amount needed to protect nonexempt property

Forgetting About Ongoing Mortgage or Car Payments

A Chapter 13 plan may help you catch up on missed payments, but it does not always replace the need to make your regular mortgage or car payments going forward. If you fall behind again after filing, your lender may ask the court for permission to move ahead with foreclosure or repossession. That’s why it’s important to look at both the plan payment and any ongoing payments together.

Assuming Chapter 13 Wipes Out Every Debt

Chapter 13 can discharge some debts after you successfully complete the plan, but not every debt goes away. Examples of debts that may survive or need special treatment include:

- Domestic support obligations, such as child support and alimony

- Certain taxes

- Many student loans

- Restitution and other court-ordered obligations

Leaving Out Assets, Debts, Income, or Recent Transfers

Bankruptcy requires full and accurate disclosure. Leaving out a creditor, asset, source of income, lawsuit, claim, bank account, transfer, or payment to a family member can create serious problems. Even honest mistakes can slow down the case, trigger questions from the trustee, or require corrections.

Paying Back Family Before Filing

Paying back a family member before filing may feel like the right thing to do, but it can create issues in bankruptcy. Payments to “insiders,” including relatives, may be reviewed by the trustee and may affect how your case is handled. This is something to talk about before you file, not after.

Taking on New Debt Without Understanding the Rules

During a Chapter 13 case, you may need permission from the trustee or the court before taking on new debt. Buying a car, refinancing a loan, using credit cards, or borrowing money without that approval can cause problems in your case.

Filing Chapter 13 When Chapter 7 Would Be Simpler

Chapter 13 is not always the better choice. If your property is protected, your income qualifies, and your main goal is to discharge qualifying unsecured debt, Chapter 7 may be faster and simpler. Chapter 13 usually makes the most sense when you need tools that Chapter 7 doesn’t offer, such as time to catch up on secured debts.

Filing Chapter 7 When Chapter 13 Would Be Safer

The opposite mistake happens too. If you have nonexempt property, mortgage arrears, car arrears, tax debt, or other issues that Chapter 7 may not fix, Chapter 13 may provide a safer path. Choosing the wrong chapter can put your property or the overall outcome of your bankruptcy at risk.

The safest way to look at Chapter 13 is as a plan that has to work in real life, not just on paper. Before filing, it’s important to understand the expected payment, which debts must be handled, the property issues involved, and the risks that could cause the case to fail.

Life During and After Chapter 13 Bankruptcy

Chapter 13 is not just a court filing. Because the repayment plan usually lasts three to five years, it can affect your monthly budget, borrowing options, and financial decisions while the case is open.

During the Chapter 13 Plan

While your case is open, you’re expected to follow the confirmed repayment plan and stay current on key obligations. In practical terms, that usually means:

- Making your chapter 13 plan payments on time

- Staying current on your mortgage if you’re keeping a home

- Staying current on required vehicle payments or plan treatment if you’re keeping a car

- Keeping required insurance on secured property, such as a house or car

- Keeping your tax returns and filings up to date

- Avoiding new debt unless you get court or trustee approval when it’s required

The biggest practical issue is consistency. A chapter 13 case can fail if plan payments are missed, mortgage or car payments fall behind again, required documents aren’t provided, or new debt is taken on without proper approval.

If Your Income or Expenses Change

A lot can happen during a three-to-five-year repayment plan. Job loss, reduced hours, medical expenses, divorce, family changes, or unexpected repairs can make a confirmed plan harder to afford.

If your financial situation changes, you may need to seek a plan modification, payment suspension, dismissal, conversion, or other court-approved relief. These options depend on the facts of the case and local practice, so it is important to address problems early instead of waiting until payments are seriously behind.

Financial Flexibility During the Case

Chapter 13 can give you structure, but it also limits flexibility. Because the plan is based on your income, expenses, and required debt treatment, you may not be able to:

- Take on new loans freely

- Buy a vehicle without approval

- Refinance major debts

- Make big financial changes without checking requirements or getting permission first

Some people find this structure helpful because it sets a clear payment path and stops constant creditor pressure. Others find the multi-year commitment challenging, especially if income is unpredictable or the budget is already tight.

After the Chapter 13 Case Is Completed

If you make all required payments and meet the remaining bankruptcy requirements, the court may grant a discharge of eligible debts. After that, collection on those discharged debts must stop.

Life after chapter 13 usually means rebuilding financial stability over time. That might include:

- Staying current on any mortgage, car loan, student loan, or other debts that continue after the case

- Using credit carefully and only when needed

- Rebuilding savings for emergencies

- Creating a budget that doesn’t depend on new debt to get through the month

Chapter 13 can give you a structured path out of a difficult financial situation, but it doesn’t automatically fix every financial habit or protect you from future setbacks. Long-term recovery usually depends on steady income, realistic budgeting, and careful financial decisions once the case is over.

Impact of Chapter 13 on Credit and Finances

Filing Chapter 13 can affect your credit, ability to borrow, and day-to-day financial flexibility. How big the impact is depends a lot on where your credit stands before you file. Many people who are looking at Chapter 13 are already dealing with missed payments, collections, lawsuits, foreclosure, repossession risk, or wage garnishment. In those situations, your credit is often already under significant stress.

Bankruptcy is serious, but it’s usually not the only thing hurting someone’s credit. A more helpful question is often whether Chapter 13 gives you a realistic way to stop the damage, protect important property, and start rebuilding over time.

How Chapter 13 Appears on Credit Reports

A chapter 13 bankruptcy can show up on your credit report as a public record. Under consumer credit reporting guidance, a chapter 13 bankruptcy may stay on your credit report for up to seven years from the date you file.

That entry can affect:

- Access to credit and loan approvals

- Interest rates you’re offered

- Rental applications and housing options

- Other lending terms

However, most lenders look at your full credit history, not just the fact that a bankruptcy appears. They may also consider your income, current debt level, payment history since the filing, and how you’ve handled credit after bankruptcy.

Credit and Borrowing During the Plan

While a chapter 13 case is active, taking on new debt may require approval from the trustee or the court. That can affect your ability to:

- Buy a vehicle

- Refinance an existing loan

- Use credit cards

- Take on other major financial commitments

At the same time, chapter 13 can stop ongoing collection pressure and set up a clear payment path. For many people, that structure makes it easier to stabilize their finances, even though access to new credit is limited during the case.

Rebuilding Credit After Chapter 13

Once your chapter 13 case is completed and eligible debts are discharged, rebuilding credit usually happens gradually.

Many people start by:

- Staying current on any mortgage, car loan, student loan, or other debts that continue after bankruptcy

- Paying all bills on time

- Avoiding new late payments or collections

Careful, limited use of new credit can help over time, but the focus should be on stability, not rushing back into debt. Lenders often care most about:

- On-time payment history

- Steady income

- A reasonable debt load

- Some savings for emergencies

These factors can matter more in the long run than how quickly you add new accounts.

The Financial Tradeoff

Chapter 13 can make your short-term finances feel tight, because the plan payment usually lasts several years and limits how much extra money is available each month. It can also reduce your flexibility to borrow while the case is open.

The tradeoff is that chapter 13 may:

- Give you a protected structure for dealing with your debts

- Stop certain creditor actions

- Help you catch up on important payments like a mortgage or car loan

- Move you toward a discharge of eligible debts at the end of the plan

Whether that tradeoff makes sense depends on your income, property, debt situation, and the specific problem you need bankruptcy to solve.

When to Talk to a Bankruptcy Attorney About Chapter 13

Chapter 13 can be a powerful tool, but it’s more complex than most people expect. Your plan has to follow bankruptcy law, fit your budget, treat creditors correctly, and address any issues with your home, car, taxes, or support obligations.

It’s especially important to talk with a bankruptcy attorney if:

- You are facing foreclosure or have a sale date scheduled

- Your car is at risk of repossession or has already been repossessed

- You’re behind on your mortgage, car loan, taxes, or support payments

- You have significant equity in your home, vehicles, or other valuable property

- You own a business or earn self-employment income

- Your income is irregular, seasonal, or has recently changed

- You owe tax debt, child support, alimony, or other priority debts

- You recently transferred property or paid back family members

- You’ve been sued, your wages are being garnished, or a judgment has been entered against you

- You’ve filed bankruptcy before and aren’t sure which chapter you can use now

- You’re unsure whether Chapter 7 or Chapter 13 is the better option

- You want to know whether a Chapter 13 payment plan is truly realistic for you

An attorney can look closely at your income, expenses, assets, debts, recent financial activity, and goals to see whether Chapter 13 is available, whether your plan is likely to work, and whether another option may be safer.

The key question isn’t just whether you can file Chapter 13. The more important question is whether Chapter 13 actually solves the problems you’re facing without leaving you with a plan payment you can’t realistically keep up with.

What This Means for You

Chapter 13 bankruptcy is more than just a repayment plan. It’s a tool for people who need time, structure, or protection that Chapter 7 may not offer. It can help if you’re behind on your house or car, have property at risk, make too much to qualify for Chapter 7, or need a more organized way to deal with debt over time.

The real question isn’t just whether Chapter 13 is an option. The better question is whether Chapter 13 solves your specific debt problem and whether the monthly payment is one you can realistically afford.

Before you decide, it helps to look closely at the facts that drive the outcome: your income and expenses, the amount and type of your debts, how much equity you have in your property, any missed payments, tax issues, and support obligations. It’s also important to consider whether Chapter 7 would be simpler or safer in your situation. Chapter 13 can be a powerful tool, but it works best when the plan payment is affordable and clearly matched to the problem you’re trying to fix.

If you’re not sure where to start, you can:

- Compare chapter 7 and chapter 13 side by side

- Estimate a possible chapter 13 payment

- Talk with a bankruptcy attorney if you’re trying to protect a home, keep a car, stop foreclosure or repossession, or handle debts that need special treatment

That way, you can choose the approach that fits your goals and gives you the best chance of a fresh start.

Frequently Asked Questions About Chapter 13 Bankruptcy

If you’re thinking about Chapter 13, you probably have a lot of questions about how it works in real life, especially what it costs and what you can keep.

How much does it cost to file chapter 13?

There’s a court filing fee for Chapter 13, and attorney fees can vary based on how complicated your case is and local practice. The good news is that you often don’t have to pay everything upfront. In many cases, part of your attorney fees can be built into your Chapter 13 repayment plan and paid over time. The exact cost depends on your district and your specific situation.

Can I keep my house if I file chapter 13?

Many individuals use chapter 13 to catch up on missed mortgage payments over time. However, keeping a home requires maintaining ongoing mortgage payments and complying with the confirmed plan. If payments are not maintained, a lender may request court permission to proceed with foreclosure.

Can I keep my car if I file Chapter 13?

Chapter 13 may allow you to catch up on missed vehicle payments through your plan. In some situations, certain vehicle loan terms may be modified depending on how long the loan has been in place and other legal factors. Not all loans qualify for modification.

What debts are not discharged in chapter 13?

Some debts are generally not dischargeable, including certain tax obligations, domestic support obligations such as child support or alimony, and most student loans unless specific legal standards are met. The treatment of debts depends on their classification under bankruptcy law.

What happens if I miss a plan payment?

Missing payments can put your case at risk of dismissal. In some situations, it may be possible to request a plan modification if financial circumstances change. Court approval is required for most adjustments.

Can I pay off my chapter 13 plan early?

Early payoff may be possible in certain cases, but it can involve additional legal considerations, including how unsecured creditors must be treated under bankruptcy law. Early completion is not automatic and may require court approval.

Will my employer or neighbors know that I filed?

Bankruptcy filings are public records. However, they are not typically published broadly. Employers may become aware of a filing in limited circumstances, such as if a wage garnishment was in place prior to filing or if income documentation is required.

Can I file chapter 13 more than once?

In some situations, you can file Chapter 13 again after a prior bankruptcy. However, there are rules about how soon you can file and when you can receive another discharge. These waiting periods depend on the type of earlier case you filed (for example, Chapter 7 vs. Chapter 13) and how much time has passed since that case.

Filing again can be helpful in the right situation, but it’s important to talk with a bankruptcy attorney first so you understand your options, any waiting periods that apply, and what a second case would realistically do for you.

Explore More of Our Bankruptcy Guides Related to Chapter 13

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin