Understanding Chapter 13 Bankruptcy in Colorado

If you're typing "chapter 13 bankruptcy colorado" into a search bar, you're probably stressed, overwhelmed, and trying to figure out how to keep your life from spinning off track. Chapter 13 bankruptcy in Colorado is designed for exactly that situation: it gives you a structured way to reorganize your debts while you keep living your life, paying your bills, and protecting the things that matter most.

Colorado Chapter 13 Bankruptcy — At a Glance

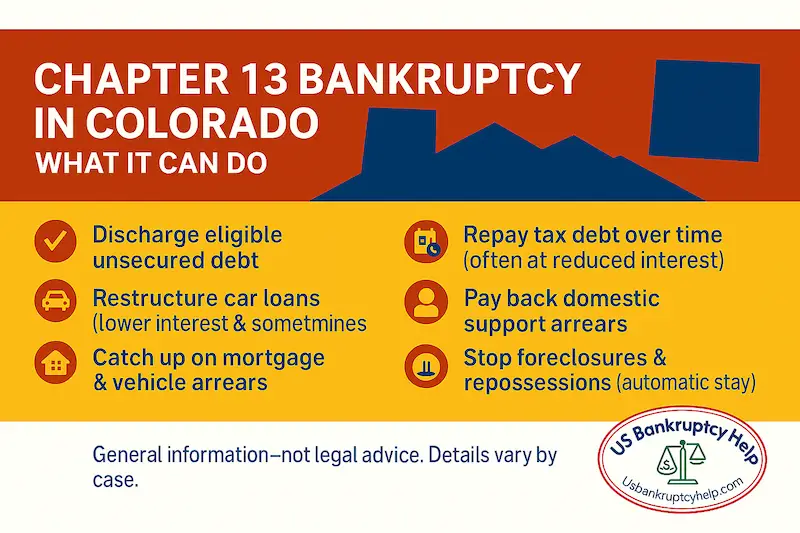

- Built On A Court-Approved Repayment Plan: In a typical chapter 13 bankruptcy in Colorado, you propose a three– to five–year repayment plan that pulls mortgage arrears, car loans, taxes, support obligations, and unsecured debts into one structured payment instead of juggling separate crises.

- Income + Debts Drive Eligibility: You need regular income and must be under the chapter 13 debt limits in 11 U.S.C. § 109(e). The court and the chapter 13 trustee look at whether your budget can realistically support the plan you propose for the full three to five years.

- Powerful Tools For Catching Up Secured Debts: A Colorado chapter 13 plan can be used to cure past–due mortgage payments over time, stop most foreclosure activity, and address vehicle arrears—sometimes adjusting interest or how the car is paid for within the plan when the law allows.

- Priority Debts Must Be Dealt With: Domestic support obligations and many tax debts are treated as priority claims and usually must be paid in full over the life of the plan. Chapter 13 gives you a structured way to do that instead of scrambling outside of court.

- Unsecured Creditors Get What The Law Requires—Not Always 100%:Credit cards, medical bills, and similar unsecured debts are often paid only a percentage of what's owed, with the remainder potentially discharged at the end of the plan. How much they receive depends on your income, your budget, and how much non-exempt asset value (under Colorado exemption law) has to be factored into the plan.

- Automatic Stay = Breathing Room: Once your case is filed, the automatic stay usually stops most collection efforts—wage garnishments, lawsuits, foreclosure sales, and repossession attempts—while you make plan payments and keep up with required ongoing obligations like current support and taxes.

- Trustee Administration And Court Confirmation: A standing chapter 13 trustee in Colorado reviews your plan, runs your 341 meeting, collects your payments, and distributes funds to creditors. The plan does not become binding until the bankruptcy judge confirms it, so feasibility and compliance with the Code are critical.

- Most Plans End In A Discharge, Some In Full Pay: Many plans finish with remaining balances on eligible unsecured debts being discharged. Others are “100% plans,” where all allowed claims are paid in full over time and the discharge mainly serves to close the case and bar future collection on those claims.

- Life In Chapter 13 Is Structured But Livable: Expect a tighter, more intentional budget and a mandatory monthly payment to the trustee, while you stay current on key ongoing expenses. Over three to five years, many filers build strong financial habits that outlast the case itself.

- Not A Self-Help Project: Chapter 13 is a sophisticated federal remedy that interacts with Colorado exemption law, federal priority rules, and local trustee practices. A Colorado bankruptcy attorney's role is to design and defend a plan that fits your goals and the law, so you're not trying to learn the system while your home, wages, or business are on the line.

If you're still comparing your options and want a broader overview of how bankruptcy works across the state, you can also visit our Colorado bankruptcy information home page, which brings together our main Colorado bankruptcy resources in one place.

Instead of wiping out eligible debts quickly like chapter 7, chapter 13 colorado focuses on a long-term repayment plan. You keep important assets such as your home and your car as long as you stay on track with the plan. For many Colorado filers with steady income, this "colorado bankruptcy chapter 13" approach offers a more realistic, less disruptive path out of debt.

In a typical bankruptcy chapter 13 colorado case, you propose a repayment plan that usually lasts three to five years. The plan lays out how much you will pay each month based on your income, reasonable living expenses, and what the law requires you to pay certain creditors. The bankruptcy court must review and approve this plan before it becomes binding on you and your creditors.

The chapter 13 trustee colorado plays a central role in whether your case succeeds. The chapter 13 bankruptcy colorado trustee reviews your paperwork and plan, asks questions at your creditor meeting, and then collects your monthly payments and distributes them to creditors. Understanding what the trustee is looking for—and how to stay in compliance—can make the entire process smoother and far less stressful.

Colorado residents also benefit from state-specific protections known as colorado chapter 13 exemptions. These exemptions help shield certain property—like a portion of your home equity, vehicle, and household goods—while you're in your repayment plan. Knowing what is and isn't protected before filing can help you structure your plan in a way that preserves as much of your property as possible.

One of the most powerful features of filing chapter 13 in colorado is its ability to stop a foreclosure or repossession. The moment your case is filed, an automatic stay usually goes into effect, which can pause collection calls, lawsuits, garnishments, and foreclosure activity. For many families, that breathing room—and the chance to catch up on missed house or car payments over time—is nothing short of a lifeline.

Because chapter 7 vs chapter 13 colorado cases involve different rules, tradeoffs, and long-term consequences, legal guidance is strongly recommended. An experienced bankruptcy attorney can help you evaluate whether chapter 13 truly fits your goals, explain how Colorado's exemptions and trustee practices apply to your situation, and guide you through each step so you're not trying to navigate this complex process alone.

What Is Chapter 13 Bankruptcy in Colorado?

How Chapter 13 Bankruptcy Works in Colorado

Chapter 13 bankruptcy comes from federal law—specifically chapter 13 of the Bankruptcy Code (11 U.S.C. §§ 1301–1330). When you file a chapter 13 bankruptcy in Colorado, you are using that federal framework to create a court-approved repayment plan that pulls all of your different debts into one organized strategy instead of juggling multiple crises at once.

Unlike chapter 7, which focuses on discharging eligible debts in a shorter time frame, chapter 13 colorado is built around a three- to five-year plan. During that time, you make one regular payment to the chapter 13 trustee, and the trustee distributes those funds according to the rules in your confirmed plan and the Bankruptcy Code.

Federal law sets the structure for chapter 13, but Colorado statutes supply important protection rules in the background. Instead of using the federal exemption list in 11 U.S.C. § 522(d), most long-term Colorado residents rely on Colorado exemptions. Those state-law protections help determine how much you must pay certain creditors in your plan and what you can realistically keep while you are in chapter 13.

Key Ways Chapter 13 Bankruptcy Helps Colorado Filers

The power of colorado bankruptcy chapter 13 is not just that you can keep property—it is that you can fix specific problems over time in a controlled way. A well-designed plan can address mortgage issues, vehicle loans, priority debts, and everyday unsecured bills inside one coordinated strategy.

| Chapter 13 Tool | How It Helps You in Colorado | Typical Debts or Situations |

|---|---|---|

| Curing Mortgage Arrears Over Time | Past-due mortgage amounts can be spread out over the three- to five-year plan instead of having to come up with a lump sum. As long as you make your plan payment and keep ongoing mortgage payments current, you can use chapter 13 bankruptcy colorado to stop a foreclosure and catch up gradually. | Delinquent home loans, foreclosure threats, and homeowners who fell behind due to job loss, illness, or other temporary setbacks. |

| Addressing Vehicle Loans and Arrears | Chapter 13 can be used to catch up on missed car payments inside the plan. In some cases, you may be able to pay off a vehicle at a reduced interest rate or, when the law allows, reduce the principal paid through the plan rather than what is owed on paper. | Behind-on-car-payments situations, upside-down auto loans, and vehicles at risk of repossession. |

| Paying Priority Debts That Do Not Go Away | Certain obligations must be paid in full, even in bankruptcy. Chapter 13 colorado lets you structure repayment of these "priority" debts over time instead of all at once, inside a single monthly plan payment. | Domestic support obligations and many types of tax debts that would survive a chapter 7 case. |

| Managing General Unsecured Debts | Credit cards, medical bills, and other unsecured claims are grouped together and paid based on what your budget and the law require. Many chapter 13 bankruptcy colorado filers do not pay these debts in full, yet still receive a discharge of the unpaid balance at the end of the plan. | Credit card accounts, personal loans, medical balances, and other unsecured obligations. |

While your plan is in place, the automatic stay usually protects you from most collection activity—as long as you stay in compliance with the plan and any required direct payments. That means lawsuits, garnishments, foreclosure efforts, and repossession attempts are put on hold while you work through your bankruptcy chapter 13 colorado plan.

Understanding these moving parts—how the plan is built, how the automatic stay works over time, and how your various debts fit into the rules—is crucial. With the right strategy, chapter 13 bankruptcy colorado can be less about “avoiding liquidation” and more about rebuilding your financial life in a structured, predictable way.

Who Qualifies for Chapter 13 Bankruptcy in Colorado?

Not everyone can file chapter 13 bankruptcy in Colorado. Eligibility starts with federal law, with an important Colorado layer on top. The main federal rule is found in 11 U.S.C. § 109(e), which limits chapter 13 to individuals (and married couples filing jointly) whose debts fall below certain caps and who have regular income.

To see whether filing chapter 13 in Colorado is even an option, the court and the chapter 13 trustee will look at your income, your total debt picture, and whether you have completed the required credit counseling before filing. Colorado-specific rules then help determine which exemptions apply and whether chapter 7 or chapter 13 is the better strategic fit.

Key Eligibility Requirements for Chapter 13 in Colorado

| Eligibility Factor | What It Means in a Colorado Chapter 13 Case | Key Authority / Notes |

|---|---|---|

| Regular, Reliable Income | You must have income that is predictable enough to support a three- to five-year repayment plan. That income can come from wages, self-employment, Social Security, pensions, or other consistent sources. The court and the chapter 13 trustee will look at whether the numbers realistically support the plan payment you propose. | Federal requirement under the Bankruptcy Code; the focus is on stability and feasibility over the full plan term. |

| Debt Limits Under 11 U.S.C. § 109(e) | Your total secured and unsecured debts must fall under the chapter 13 debt caps set by Congress and adjusted periodically for inflation. If your mortgages, car loans, credit cards, medical bills, and other obligations push you over those limits, you may need to consider a different chapter instead of chapter 13. | 11 U.S.C. § 109(e) (chapter 13 eligibility); limits change over time based on when you file your case. |

| Pre-Filing Credit Counseling | Before you can file, you must complete a credit counseling course from an approved provider and obtain a certificate. The course reviews your financial picture and confirms that a repayment plan is an appropriate option. Filing without a valid certificate can result in dismissal of your case. | 11 U.S.C. § 109(h); counseling must be completed within the required time frame before filing. |

| Ability to Propose a Feasible Plan | Even if you meet the basic income, debt limit, and counseling requirements, you still need to propose a plan the court can approve. That means showing that your budget supports the proposed payment and that the plan complies with the priority, secured, and unsecured debt rules in chapter 13. | Governed by 11 U.S.C. §§ 1322 and 1325; feasibility is based on your actual income, expenses, and debt structure. |

Separate from these eligibility factors, there are also residency and exemption rules that affect how your case is handled—but they do not usually decide whether you are allowed to file. In general, you need to have lived in Colorado long enough to file here under the federal venue rules, and the look-back rules in 11 U.S.C. § 522(b)(3) determine whether you use Colorado's exemption scheme or another state's.

Colorado has opted out of the federal exemption system in C.R.S. § 13-54-107, so long-term residents typically rely on Colorado exemptions instead of the federal list. Those exemptions don't control your basic eligibility for chapter 13, but they can strongly influence how much your unsecured creditors must receive in your plan and whether chapter 13 or chapter 7 is the better overall strategy.

Meeting the baseline requirements opens the door, but it does not answer the bigger question of whether chapter 13 is the right move for you. Because filing chapter 13 in Colorado involves both federal statutes and Colorado exemption law, talking with an experienced bankruptcy attorney can help you confirm your eligibility and choose the chapter that best fits your long-term goals.

Chapter 13 vs. Chapter 7 Bankruptcy in Colorado

When people in Colorado start looking at chapter 13, they're usually weighing some very practical questions: "Do I qualify for a repayment plan? Can I use it to catch up on my mortgage or car, and what happens to my other debts?" It naturally leads to a comparison with chapter 7 in Colorado, because the two chapters solve different kinds of problems. This page focuses on chapter 13, but seeing how it differs from the other chapter can help you decide which path fits your situation better.

At a high level, chapter 13 is about restructuring and catching up over time, while chapter 7 is about a more immediate discharge of qualifying debts if you meet that chapter’s requirements. Both are federal tools, but they solve different kinds of financial problems.

| Issue | How It Works in Chapter 13 | How It Works in Chapter 7 |

|---|---|---|

| Overall Approach | You propose a three- to five-year repayment plan. The court and the trustee review your income, expenses, and debts, and if the plan is confirmed, you make one regular payment that gets distributed to creditors according to the rules in chapter 13. | The focus is on identifying which debts can be discharged and how any non-exempt property will be handled under that chapter. The case timeline is generally shorter, and there is no long-term repayment plan supervised by the court. |

| Catching Up on Secured Debts | Chapter 13 is often the better fit when you are behind on a mortgage or vehicle loan but want to keep the property. You can catch up on arrears over the life of the plan while the automatic stay usually keeps foreclosure or repossession efforts on hold. | If you are behind on a secured debt, this chapter may not give you the same long-term tools to cure arrears inside the case. It can still be very helpful for the right person, but it does not offer the same structured catch-up mechanism. |

| Priority Debts (Taxes, Support) | Priority debts that must be paid in full under the Bankruptcy Code, such as many tax obligations and domestic support, can be built into your chapter 13 plan and repaid over several years in an orderly way. | Priority debts are still treated specially, and many are not discharged, but there is no multi-year payment plan supervised by the court. You may need a separate strategy for paying them after the case closes. |

| General Unsecured Debts | Credit cards, medical bills, and similar unsecured debts are grouped together and paid based on what your budget and the law require. Many filers do not pay these debts in full, yet can still receive a discharge of the unpaid balance at the end of a successful plan. | These debts may be discharged more quickly if they are eligible under that chapter, but the tradeoff is that you do not get the same long-term plan structure to handle arrears on secured or priority debts. |

| Time Commitment | You are committing to a three- to five-year plan, with ongoing payments and reporting obligations. This longer horizon can be a strength if you need time to fix multiple issues under court supervision. | The overall case is typically shorter, but you lose the ongoing structure that chapter 13 provides for catching up and coordinating different kinds of debt. |

| Who Typically Uses It | Often a good fit for people with steady income who are behind on a home or car, need to pay priority debts over time, or want a more holistic, long-range plan to deal with several problem areas at once. | Often used by people whose financial situation is better addressed by a shorter case focused on discharging qualifying debts, rather than a long-term repayment structure. |

Ultimately, the better option depends on your goals and your specific mix of debts, assets, and income. Chapter 13 may make more sense if you need time and structure to fix mortgage arrears, vehicle issues, or priority debts under court protection. The other chapter may be more suitable if your situation is best addressed by a shorter case and you meet that chapter’s requirements.

If you want a deeper dive into how the other chapter works in your state, you can review our detailed Colorado chapter 7 page. For a broader, nationwide comparison of the two chapters, you can also visit our chapter 7 vs. chapter 13 guide.

A conversation with an experienced bankruptcy attorney can help you apply these concepts to your own facts and decide whether a chapter 13 repayment plan is the right path for you.

The Chapter 13 Bankruptcy Process in Colorado

The process of filing chapter 13 bankruptcy in Colorado is more like running a marathon than flipping a switch. It follows a series of structured steps laid out in the Bankruptcy Code and applied through the U.S. Bankruptcy Court for the District of Colorado. Understanding what happens—and when—can make the experience far less intimidating.

Every case is a little different, but most chapter 13 cases in Colorado move through the same core milestones: credit counseling, preparing paperwork, filing the petition and plan, gaining the protection of the automatic stay, meeting with the trustee and creditors, and seeking court approval (confirmation) of your repayment plan.

Key Steps in a Colorado Chapter 13 Case

| Step | What Happens | Why It Matters |

|---|---|---|

| 1. Complete Credit Counseling | Before filing, you must take a credit counseling course from an approved provider and obtain a certificate. This is a federal requirement for all individual filers and must be completed within the required time frame before your case is opened. | Without this certificate, the court can dismiss your chapter 13 case. The course also gives a baseline review of your finances and confirms that a repayment plan is an appropriate option. |

| 2. Gather Financial Documents | You and your attorney (if you work with one) assemble pay stubs, tax returns, bank statements, a list of all creditors, household expenses, and information about your property and debts. | Complete and accurate documents are the backbone of a successful chapter 13 case. The trustee and court rely on this information to evaluate your budget and repayment plan. |

| 3. File the Petition and Proposed Plan | Your bankruptcy petition, schedules, and proposed chapter 13 plan are filed with the U.S. Bankruptcy Court for the District of Colorado. You also disclose your income, assets, debts, and expenses under penalty of perjury. | Filing officially starts your case. It sets deadlines, triggers the trustee's review, and begins the court's oversight of your proposed three- to five-year repayment plan. |

| 4. Automatic Stay Goes Into Effect | In most situations, the automatic stay under 11 U.S.C. § 362 takes effect as soon as your case is filed. This usually stops most collection actions, including lawsuits, garnishments, foreclosure sales, and repossession efforts. | The stay gives you immediate breathing room while the plan is evaluated. As long as you follow the rules and make required payments, it can protect your home, vehicle, and wages during the case. |

| 5. Begin Making Plan Payments | In chapter 13, you typically must start making payments to the trustee within 30 days after the plan is filed, even before the court officially approves it. Payments continue every month throughout the plan. | Making these early payments shows the court and trustee that your plan is feasible and that you are serious about following through on the repayment schedule. |

| 6. Attend the 341 Meeting of Creditors | About a month after filing, you attend a brief, recorded meeting run by the chapter 13 trustee (not a judge). The trustee asks questions about your paperwork, budget, and plan. Creditors can appear and ask questions too, although many do not. | This is your opportunity to clarify anything in your documents and show that you have been honest and thorough. It is a required step in every chapter 13 case. |

| 7. Plan Review and Confirmation | The trustee reviews your plan in detail and may request changes. If objections are resolved and the plan meets the legal requirements, the court enters an order confirming the plan. | Confirmation is the court's formal approval of your repayment roadmap. Once confirmed, it governs how creditors are paid and what you must do over the remaining three to five years. |

In practice, the chapter 13 bankruptcy process in Colorado is a blend of paperwork, deadlines, and communication with the trustee and the court. Staying organized, being honest in your disclosures, and following each step carefully can dramatically increase the chances that your plan will be confirmed and carried through to a successful discharge.

This overview is meant to give you a clear big-picture roadmap, not to serve as a set of instructions for handling a chapter 13 case on your own. A Colorado bankruptcy attorney can prepare the required forms, track deadlines, communicate with the trustee, respond to any objections, and guide you through each phase so you are not learning the system at the same time you are relying on it to protect your home, income, and property.

Filing Chapter 13 in Colorado: Step-by-Step

By the time you are seriously considering filing chapter 13 in Colorado, you are usually past the theoretical stage and into the practical one: "What do I need in place before we actually file, and what will my attorney help me with from that point forward?" The earlier section outlined the major milestones in a Colorado chapter 13 case. This section focuses on the big-picture preparation that makes those steps go more smoothly.

Filing a chapter 13 case is not just handing in forms to the court. It is a coordinated process that should reflect your real goals—saving a home, keeping a vehicle, dealing with tax or support obligations, and bringing credit cards and medical bills under control—using a single repayment plan.

Before You File: Colorado Chapter 13 Readiness Checklist

- Clarify Your Goals. Decide what you most need chapter 13 to accomplish: catching up on a mortgage, stabilizing a car situation, addressing tax or support debts, or creating breathing room from constant collection pressure. Clear goals help shape the repayment plan.

- Confirm Basic Eligibility. Review your income stability, overall debt levels, and recent credit counseling with a Colorado bankruptcy attorney to make sure chapter 13 is available and appropriate for your situation.

- Gather Core Financial Information. Collect pay stubs, tax returns, bank statements, and a complete list of creditors, along with a realistic picture of your monthly household budget. This is the raw material your attorney will use to build a feasible plan.

- Understand the Commitment. Filing chapter 13 in Colorado means agreeing to a three- to five-year repayment structure, regular payments to the trustee, and ongoing communication if your circumstances change.

- Work With Counsel on Timing and Strategy. A Colorado bankruptcy attorney can advise you on when to file, how to structure the plan payment, how the automatic stay is likely to protect you, and how your mortgage, car loans, taxes, and unsecured debts will be treated once the case is filed.

In other words, the "step-by-step" of filing chapter 13 is not meant to be a do-it-yourself exercise. The court provides the legal framework, but your attorney's job is to navigate that framework with you—preparing the paperwork, coordinating the filing, communicating with the chapter 13 trustee, and guiding you from the day the case is filed through confirmation and, ultimately, discharge.

The Role of the Chapter 13 Trustee in Colorado

When you file a chapter 13 case in Colorado, you are automatically assigned to a chapter 13 trustee. This person is not the judge and not your attorney. The trustee’s job is to administer your case under the Bankruptcy Code and local practice—reviewing your paperwork, evaluating your plan, collecting payments, and making sure the process is fair to everyone involved.

Under 11 U.S.C. § 1302 and related provisions, the chapter 13 trustee in Colorado has several core responsibilities. First, the trustee reviews your proposed repayment plan and financial disclosures to see whether the plan is feasible and complies with the law. The trustee can recommend confirmation, request changes, or object if something does not line up with the statutory requirements.

Once the case is underway, the trustee serves as a disbursing agent. You make a single monthly plan payment, and the trustee divides those funds among your creditors according to the confirmed plan—paying secured creditors, priority claims like certain taxes or support, and then general unsecured creditors as the law requires.

The trustee also runs the "341 meeting" (meeting of creditors), asks you questions under oath about your finances, and may communicate with your attorney about plan changes or case issues over the life of the plan. In short, the chapter 13 trustee is the day-to-day administrator of your case, while the judge resolves disputes and ultimately decides whether to confirm your plan.

How Many Chapter 13 Trustees Does Colorado Have?

In the District of Colorado, there are generally two standing chapter 13 trustees assigned to administer chapter 13 cases. Each trustee is responsible for a defined group of cases within the district, including Colorado and, for one trustee, certain Wyoming filings.

You do not choose your trustee; assignment is handled administratively based on where your case is filed and how the court and U.S. Trustee have divided the caseload. A Colorado bankruptcy attorney will know which trustee typically handles cases in your part of the state and can help you understand any local practices or expectations specific to that trustee’s office.

Finding Official Chapter 13 Trustee Contact Information

For the most up-to-date contact details for chapter 13 trustees serving Colorado, you can use the official U.S. Department of Justice resource. The U.S. Trustee Program maintains a public list of standing chapter 13 trustees nationwide, including those assigned to the District of Colorado:

Official U.S. Trustee list of Chapter 13 standing trustees

That page is updated by the U.S. Trustee Program and is the best single source for trustee names, mailing addresses, and phone numbers.

If you ever have a concern about how a case is being administered, the Office of the United States Trustee for Region 19 (which covers Colorado) also publishes its contact information:

U.S. Trustee Program – Region 19 (Colorado)

The chapter 13 trustee is central to whether your plan is confirmed and successfully completed. An experienced Colorado bankruptcy attorney will not only draft your plan but also work with the assigned trustee’s office—responding to requests, addressing objections, and helping keep your case on track from filing through discharge.

Creating a Chapter 13 Repayment Plan

A chapter 13 repayment plan is not just a spreadsheet of numbers. It is a court-approved blueprint that explainswho gets paid, in what order, and how much over the next three to five years. When you file chapter 13 in Colorado, this plan becomes the heart of your case—if the plan works, the case works.

The Bankruptcy Code divides your debts into broad groups, and the plan has to respect that structure. At a high level:

- Priority debts (like domestic support obligations and many taxes) have to be paid in full over the life of the plan unless the creditor agrees otherwise.

- Secured debts (like mortgages and vehicle loans) are treated based on the collateral, the loan terms, and what the plan is trying to accomplish—often catching up arrears or, in some cases, adjusting interest or how the debt is repaid.

- Unsecured debts (like most credit cards and medical bills) are grouped together and paid based on what your budget and the law require, not necessarily the full balance.

On top of that, your plan has to satisfy two big tests: your income must support the payment you are proposing, and your exemptions and assets must be handled in a way that gives unsecured creditors at least as much as they would receive in a hypothetical chapter 7 case. In Colorado, that “best interests of creditors” analysis is heavily influenced by the Colorado exemptions available to you.

How a Chapter 13 Plan Pays Your Debts

Think of the plan as a funnel: your monthly payment goes in at the top, and the money flows out in a legally required order. Typically, it looks something like this:

- First, administrative costs (such as trustee commissions and approved attorney’s fees) are paid.

- Next, priority claims are paid—most commonly certain tax debts and domestic support obligations.

- Then, secured creditors are paid according to how the plan treats their claims (for example, curing mortgage arrears, paying off a car loan through the plan).

- Finally, whatever is left goes to general unsecured creditors, who often receive only a percentage of what they are owed.

The total amount that reaches unsecured creditors is driven by a combination of your household income and expenses, the value of your non-exempt assets, and how much has to be devoted to priority and secured debts before anything “trickles down” to that last group.

Different Types of Chapter 13 Plans in Colorado

No two chapter 13 plans look exactly alike. Here are a few common patterns that show how flexible the structure can be:

- Mostly Secured / Priority Plan. Some people use chapter 13 primarily to fix secured and priority problems—catching up on a mortgage, saving a car, and paying tax or support arrears—while general unsecured creditors receive very little or, in some cases, almost nothing. If your income is modest and your non-exempt asset value is low, this type of plan can still be confirmed as long as it meets the legal tests.

- Balanced Plan. In other cases, the plan payment is high enough that, after paying priority and secured debts, there is a meaningful pot left for unsecured creditors. These plans might pay a significant fraction of unsecured claims—say 20%, 40%, or more—depending on income, expenses, and asset values.

- “100% Plan.” Some chapter 13 filers end up paying all allowed claims (including unsecured debts) in full over the life of the plan. This can happen when income is relatively strong, non-exempt assets are substantial, or there are strategic reasons to use chapter 13 even though a full repayment is required.

Which category you fall into depends on several moving parts: your income and household budget, the value of your assets, how much of that value is protected by exemptions, the amount of secured and priority debt that must be addressed, and which secured debts you choose to treat inside the plan (for example, whether to pay a car loan through the trustee or keep paying it directly).

A well-crafted chapter 13 plan in Colorado weaves all of this together. Rather than walking you through line-by-line paperwork, your attorney’s role is to understand your goals, apply the income and exemption rules correctly, and design a plan that pays the right creditors in the right order—so that three to five years of effort actually leads to the discharge and fresh start you are working toward.

Benefits and Drawbacks of Chapter 13 Bankruptcy in Colorado

Benefits of Chapter 13 in Colorado

Chapter 13 bankruptcy in Colorado can be a powerful tool when used for the right situation. One major benefit is the ability to pull different types of debt—mortgage arrears, vehicle loans, taxes, support obligations, and unsecured debts—into one coordinated repayment plan instead of trying to juggle them separately.

For many people, the biggest immediate relief comes from the automatic stay. Once your case is filed, most collection activity must stop: foreclosure sales are typically paused, wage garnishments are halted, and repossession efforts usually cannot go forward while you are under the protection of the court and making required payments.

Over the longer term, a chapter 13 plan can:

- Give you time to fix secured debts. You can catch up on missed mortgage payments or car payments over three to five years instead of all at once.

- Provide a structured way to pay priority debts. Domestic support obligations and many tax debts can be repaid in an orderly fashion inside the plan.

- Control how unsecured debts are handled. Credit cards, medical bills, and similar unsecured claims are grouped together and paid based on your budget and the legal requirements, not necessarily in full.

- Create a predictable framework. Instead of reacting to every new collection action, you follow one court-approved plan that, if completed, leads to a discharge of eligible remaining balances.

Drawbacks and Challenges of Chapter 13

Chapter 13 is not the right fit for everyone. The same features that make it powerful can also make it demanding. The plan typically lasts three to five years, which means you are committing to a long-term payment schedule and ongoing oversight from the trustee and the court.

Because your budget is central to the case, you have less flexibility to absorb new financial shocks. A job loss, major medical issue, or unexpected expense can put strain on the plan and may require a modification or, in some cases, lead to dismissal if payments cannot be maintained.

Other potential drawbacks include:

- Steady income is essential. Without reliable income, it is difficult to propose and sustain a feasible plan payment for three to five years.

- Credit impact and public record. A chapter 13 filing appears on your credit report and becomes a matter of public record, and it takes time and intentional effort to rebuild credit afterward.

- Ongoing obligations during the case. You must keep up with current obligations (like ongoing mortgage payments, support obligations, and taxes) at the same time you are making your plan payment.

Understanding both the strengths and the limitations of chapter 13 in Colorado is critical before you decide to move forward. A conversation with an experienced Colorado bankruptcy attorney can help you weigh these benefits and drawbacks against your own goals and decide whether committing to a chapter 13 plan makes sense for you.

Life During a Chapter 13 Bankruptcy Plan

How Daily Life Changes in a Chapter 13 Plan

Being in a chapter 13 plan in Colorado is less about one big court date and more about what happens every month afterward. For three to five years, your plan payment becomes a fixed part of your budget, and your financial life runs through that structure. When the plan is designed well, it brings order to a situation that used to be driven by panic and collection pressure.

In many cases, plan payments are made through a payroll order so that the money goes straight from your paycheck to the chapter 13 trustee. That can feel restrictive at first, but it also takes some of the stress out of remembering due dates and helps prove to the court and trustee that the plan is sustainable.

At the same time, you still have to keep up with certain "outside the plan" obligations. That often means staying current on ongoing mortgage payments, vehicle insurance, domestic support obligations, and current taxes while your past-due amounts and other debts are being addressed inside the plan.

Staying on Track During Your Colorado Chapter 13 Plan

Communication is crucial. If your income changes, you lose a job, you need to replace a car, or you face an unexpected major expense, your attorney needs to know so they can talk with the trustee about possible options—such as a plan modification, temporary relief, or other adjustments. Trying to hide a problem usually makes it worse; raising it early often keeps the case on track.

You are also expected to live within a tighter, more intentional budget. That can mean delaying certain purchases, planning ahead for irregular expenses, and being careful about taking on new debt during the case. The goal is not to punish you, but to make sure the plan is realistic and that you can actually finish it.

The Emotional Side and Long-Term Habits

Emotionally, life in chapter 13 is a mix of discipline and relief. You may feel the squeeze of a tighter budget, but you also gain structure, a clear end point, and a way to answer collection calls with, "I'm in an active chapter 13 case." For many people, that alone is a major shift in stress levels.

Over time, the habits you develop during the plan—tracking expenses, planning ahead, and making intentional financial decisions—can become the foundation for long-term stability even after discharge. Support from family, friends, and professionals can make it easier to stay focused on why you filed in the first place and what life can look like when the plan is complete.

Key aspects of life during a Colorado chapter 13 plan include:

- Living within a structured budget, with a fixed plan payment and less room for impulse spending.

- Staying current on ongoing obligations, such as mortgage or rent, insurance, support, and taxes, while the plan handles arrears and other debts.

- Regular communication with your attorney and the trustee's office if your circumstances change, rather than trying to navigate problems alone.

- Leaning on healthy support systems—family, friends, and professionals—to stay focused on the goal of finishing the plan and receiving a discharge.

Modifying or Failing a Chapter 13 Plan

When a Chapter 13 Plan Needs to Change

A chapter 13 plan in Colorado is designed to last three to five years, and very few people's lives stay exactly the same for that long. Job changes, reduced hours, medical issues, new family obligations, or unexpected expenses can all make the original payment schedule harder—or impossible—to maintain.

The key point is that the plan is not carved in stone. If something important changes, the Bankruptcy Code allows for modifications in many situations. With your attorney's help, you may be able to lower the payment, change how certain debts are treated, extend the length of the plan (within legal limits), or adjust the plan to reflect new realities.

What you should not do is quietly stop paying and hope it works itself out. As soon as you see that you are going to struggle with your plan payment or ongoing obligations, it is critical to talk with your attorney so they can raise the issue with the chapter 13 trustee and, if appropriate, ask the court to approve a modified plan.

Options If You Cannot Keep Up

When a chapter 13 plan in Colorado becomes unworkable, there are often more options than just "pay or fail." Depending on your situation, your attorney may explore:

- Plan Modification. Adjusting the monthly payment or the way certain debts are treated, based on a documented change in income or expenses, and asking the court to approve the revised plan.

- Temporary Relief. In some cases, seeking short-term relief or a brief pause in payments (if the law and local practice allow) while you address a temporary setback such as a medical issue or gap in employment.

- Conversion to a Different Chapter. If your circumstances have changed dramatically, it may make sense to discuss whether converting the case to a different chapter is appropriate and available in your situation.

- Early Exit in Limited Cases.In rare situations where you have done everything you reasonably can and circumstances beyond your control prevent completion, your attorney may evaluate whether you qualify for a limited "hardship" discharge under the Bankruptcy Code.

What Happens If a Chapter 13 Plan Fails

If payments stop and no adjustment is approved, the trustee will typically move to dismiss the case. A dismissal ends the protection of the automatic stay and generally puts creditors back in the position to pursue collection, including garnishments, lawsuits, foreclosure, or repossession, depending on the type of debt.

In some situations, it may be possible to refile, but there can be waiting periods, limits on how long the automatic stay lasts, and strategic considerations about timing and chapter choice. That is why it is so important to treat problems with your plan as early warning signs and not as something to ignore.

The bottom line: chapter 13 in Colorado is meant to be a flexible, long-term tool, but it works best when you stay in close contact with your attorney. If your income changes, your expenses jump, or your life takes an unexpected turn, raising the issue promptly gives you the best chance to modify the plan, preserve court protection, and still reach the discharge you were working toward.

Completing Chapter 13: Discharge and Aftermath

What Happens at the End of a Chapter 13 Plan

In most Colorado chapter 13 cases, the goal is straightforward: make all required plan payments, meet the other statutory requirements, and receive a discharge order from the court. A chapter 13 discharge wipes out remaining balances on eligible debts that were included in the plan, giving you the fresh start you have been working toward for three to five years.

To reach that point, you generally must:

- Complete all required payments under your confirmed plan.

- Stay current on domestic support obligations that came due after you filed.

- Complete a post-filing financial management (debtor education) course and file the certificate.

If those conditions are met and there are no disqualifying events, the court typically enters a chapter 13 discharge under 11 U.S.C. § 1328. That order permanently eliminates personal liability on dischargeable debts that still have a balance at the end of the plan.

What About 100% Plans?

Not every chapter 13 plan ends with unpaid balances to discharge. In some cases—often called "100% plans"—all allowed claims are paid in full over the life of the plan. In that scenario, the discharge does not provide the same economic benefit because there is little or nothing left to wipe out, but the court will usually still enter a discharge order once the plan is successfully completed and the other requirements are met.

In practical terms, the key distinction is this:

- Most plans use the discharge to eliminate remaining balances on eligible unsecured debts after priority and secured debts have been addressed.

- 100% plans mainly use chapter 13 for structure and timing—coordinating payments, catching up arrears, and managing different kinds of debt—because the creditors end up being paid in full by the end of the case.

Life After a Chapter 13 Discharge

Whether your case was a lower-percentage plan or a 100% plan, the end of chapter 13 is a transition point. You no longer make payments to the trustee, and the automatic stay is no longer needed because the case has run its course. From that point forward, your focus shifts to rebuilding and protecting the progress you have made.

Smart next steps after a chapter 13 discharge include:

- Reviewing your credit reports to confirm that discharged debts are reported accurately and that the bankruptcy is reflected correctly.

- Continuing the budgeting habits you developed during the plan so you do not slide back into the same patterns that led to filing.

- Using credit thoughtfully, if at all, starting small and paying balances in full to rebuild your credit profile over time.

A completed chapter 13 case is the culmination of years of disciplined effort. Understanding how the discharge works, and what it means in your specific situation—whether you had remaining balances or paid everyone in full—can help you make the most of the fresh start you earned.

Rebuilding Credit After Chapter 13 Bankruptcy

Why Life After Chapter 13 Starts Further Ahead

Coming out of a chapter 13 case in Colorado is very different from emerging from a shorter case that simply wipes out eligible debts. By the time your plan ends, you have usually:

- Made three to five years of on-time payments to the chapter 13 trustee.

- Caught up on a mortgage or vehicle, or paid one off entirely through the plan.

- Paid priority debts like taxes or domestic support obligations in an organized way.

- Reduced or eliminated a large portion of your unsecured balances.

That means your credit story is not just "there was a bankruptcy." It is also, "for several years afterward, this person made consistent payments under court supervision and dealt with difficult debts instead of ignoring them." Many people coming out of chapter 13 find that lenders pay attention to that pattern over time.

Turning Plan History Into Positive Credit History

After your plan is complete and the case is closed, the focus shifts from trustee payments to how you handle the accounts that remain and any new credit you choose to use. The habits you built during your plan—budgeting, planning ahead, and making payments on time—are exactly what credit scoring models tend to reward.

Smart moves in the first year or two after chapter 13 include:

- Check your credit reports for accuracy. Make sure accounts treated in your chapter 13 are reported correctly and that any remaining balances match what should be left after the plan and discharge. Dispute clear errors in writing with the credit bureaus.

- Protect existing positive trade lines. If you kept a mortgage, vehicle loan, or other ongoing account during the case, on-time payments going forward can be a powerful driver of score improvement.

- Add new credit slowly and intentionally. Some people use a small secured card or a low-limit card from a mainstream lender, charging modest, predictable amounts and paying in full each month. The goal is to show responsible use, not to carry large balances.

Building Long-Term Stability, Not Just a Higher Score

Rebuilding after chapter 13 is less about digging out of a fresh crater and more about continuing the progress you started in the plan. You have already proven you can live within a budget and make payments consistently over years. The next phase is about keeping that structure without court supervision.

That usually means:

- Maintaining a written or digital budgetso the room created by paying off old debts doesn't quietly get filled with new ones.

- Using credit as a tool, not a lifeline, borrowing only for purposes that fit your long-term goals and that you can realistically repay.

- Monitoring your credit reports periodically to track progress and catch issues early, rather than waiting until you need a loan or a major purchase.

A chapter 13 case is a long, demanding process, but the discipline it requires often leaves you in a stronger position than you might expect. By treating the years after your plan as an extension of that work—not a return to old habits—you can turn the structure of chapter 13 into a lasting foundation for your financial life.

Colorado Chapter 13 Bankruptcy FAQs

Can You Pay Off A Chapter 13 Plan Early In Colorado?

Sometimes. In a Colorado chapter 13 case, you generally commit your projected disposable income for a three- to five-year “applicable commitment period.” In many plans, you cannot simply send in a lump sum, stop paying, and expect the case to close early unless you have paid everything the law requires, including what unsecured creditors are entitled to receive. In a true 100% plan—where all allowed claims will be paid in full—an early payoff is more realistic. In other cases, trying to finish early can trigger objections from the trustee or creditors and may require a plan modification or, effectively, a 100% payout. The safest approach is to treat early payoff as a strategy question for you and your Colorado bankruptcy attorney, not something to attempt on your own.

What Can I Keep In A Chapter 13 Case In Colorado?

Most people who file chapter 13 in Colorado keep all of their property, as long as the plan is structured correctly and they can afford the required payment. The Bankruptcy Code looks at the value of what you own and compares it to what creditors would receive in a hypothetical chapter 7 case. Colorado’s exemption laws—often called Colorado exemptions—help protect equity in things like your home, vehicle, household goods, and certain other assets. If you have more non-exempt value than the exemptions cover, the plan typically has to pay at least that much to unsecured creditors over time. In practice, chapter 13 is usually about keeping property and paying what the law requires, not about giving assets up.

How Long Does A Chapter 13 Case Take In Colorado?

For most Colorado filers, a chapter 13 case lasts between three and five years. The length of your plan depends on your income level, how the “applicable commitment period” rules apply to you, and what it takes to pay required amounts on priority and secured debts. Some people qualify for a shorter plan, and a small number of cases finish sooner when all allowed claims are paid in full more quickly, but you should think of chapter 13 as a multi-year commitment from the start.

What Does The Chapter 13 Trustee Do In My Colorado Case?

The chapter 13 trustee is the court-appointed administrator of your case. In Colorado, the trustee reviews your repayment plan, runs your meeting of creditors, and makes sure your plan follows the rules. You make one regular payment to the trustee, and that office distributes the funds to creditors according to your confirmed plan. The trustee is not your lawyer and does not represent you or your creditors; their job is to apply the Bankruptcy Code and local practice fairly to every case in their docket.

Can I Change My Chapter 13 Plan If My Situation Changes?

Often, yes. If your income goes down, your expenses increase, or something significant changes during your Colorado chapter 13 case, it may be possible to modify the plan. A modification can sometimes reduce the payment, change how certain debts are treated, or adjust the remaining term within legal limits. Any change has to be proposed through the court and approved by a judge, so it is not as simple as just paying a different amount. The key is to talk to your attorney early, before missed payments turn into a motion to dismiss.

What Happens If I Miss A Chapter 13 Plan Payment?

Missing a payment is a warning sign, not an automatic disaster—but it cannot be ignored. If payments fall behind, the chapter 13 trustee will usually file a motion asking the court to dismiss your case. Dismissal ends the protection of the automatic stay and puts creditors back in position to pursue garnishments, lawsuits, foreclosure, or repossession. If you see trouble coming, contact your attorney immediately. It may be possible to catch up, ask for a modification, or explore other options before the case is lost.

Does Filing Chapter 13 In Colorado Destroy My Credit Forever?

A chapter 13 case will appear on your credit report for years, and you should expect a noticeable impact at first. But people who complete Colorado chapter 13 plans are often in better shape than they were before filing: past-due balances are resolved, priority debts are under control, and there is a track record of years of structured payments. Many filers are able to qualify for vehicle loans, mortgages, or other credit again sooner than they expect—often at improving terms over time—as long as they protect existing positive accounts, avoid new problem debt, and keep using the budgeting skills they developed during the plan.

Is Chapter 13 Bankruptcy in Colorado Right for You?

Seeing Chapter 13 As A Tool, Not A Failure

Deciding whether to file chapter 13 bankruptcy in Colorado is not about giving up—it is about deciding whether this particular tool fits the problems you are trying to solve. For many people, chapter 13 is the first time their mortgage arrears, car issues, tax debt, support obligations, and credit cards are all addressed inside one structured, court-supervised plan instead of in a constant emergency.

At its best, a chapter 13 plan gives you three to five years of structure, protection, and progress: time to catch up on what matters most, pay what the law requires, and work toward a discharge or full payoff that closes the book on a difficult chapter of your financial life.

When Chapter 13 May Make Sense In Colorado

Chapter 13 is not right for everyone, but it is worth serious consideration if you:

- Have steady income but cannot catch up on past-due debts—especially a mortgage or vehicle—without a structured plan.

- Need to deal with priority debts like certain taxes or domestic support obligations that will not simply disappear in another chapter.

- Want to protect important property while still complying with the rules on how much your creditors must receive over time.

- Are willing to commit to a three- to five-year framework in exchange for a realistic path out of constant collection pressure.

Next Steps: Get Advice That Fits Your Situation

Reading about chapter 13 can give you a strong foundation, but it cannot replace a review of your actual numbers—your income, expenses, assets, and debts—under Colorado law. The same chapter 13 rules can play out very differently for a homeowner behind on a mortgage, a family dealing with tax or support arrears, or someone whose main issue is high-interest unsecured debt.

A Colorado bankruptcy attorney can walk through your full picture, compare chapter 13 with other options, and show you what a plan might look like in real dollars and months. From there, you can decide whether filing chapter 13 in Colorado is simply one idea among many—or the structured, realistic path forward you have been looking for.

Explore Our Colorado Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin