Bankruptcy Laws in Tennessee: Chapter 7, Chapter 13, Exemptions, and Where to File

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

Filing for bankruptcy in Tennessee means dealing mostly with federal law, but the Tennessee-specific rules still matter. State exemptions help determine what property you can keep. Tennessee’s median income numbers are used in the Chapter 7 means test and you also have to file your case in the correct Tennessee bankruptcy district.

Most people here end up looking at either Chapter 7 or Chapter 13. Chapter 7 is usually best if your main goal is to wipe out qualifying unsecured debts— things like credit cards, medical bills, personal loans, and collection accounts—as quickly as possible. Chapter 13 is more common when you need time to catch up on a mortgage, car loan, taxes, child support or alimony arrears, or other debts through a structured repayment plan.

The better option depends on your specific situation: what problem you’re trying to solve, what property you need to protect, how urgent things are, and whether Chapter 7 or Chapter 13 offers a realistic way forward. This guide walks through the key Tennessee bankruptcy rules so you know what to look at before you decide on your next step.

Bankruptcy in Tennessee: Start With the Problem You Need to Solve

The best bankruptcy path in Tennessee usually starts with one simple question: what problem are you trying to solve? Someone buried in credit card or medical debt needs a different approach than someone trying to stop a wage garnishment, save a house from foreclosure, keep a car, or protect other property.

Before you focus on Chapter 7 or Chapter 13 , take a moment to figure out what is putting the most pressure on you right now.

- Are credit cards, medical bills, or personal loans your biggest worry?

- Has a creditor or debt buyer filed a lawsuit against you?

- Are your wages already being garnished or about to be?

- Are you behind on your mortgage payments?

- Has your lender started or threatened foreclosure?

- Are you behind on your car loan?

- Is your vehicle at real risk of repossession?

- Do you own a home, vehicle, or other property you want to be sure you can keep?

- Are you unsure whether Tennessee exemptions are enough to protect that property?

- Have you recently given away property or repaid loans to friends or family?

- Are you unsure whether Chapter 7 or Chapter 13 is the better fit?

Your answers help point you toward the next step. If unsecured debt is the main issue and it looks like Tennessee bankruptcy exemptions cover what you own, Chapter 7 may be worth a hard look. If you are trying to save a house or car, facing foreclosure or repossession, dealing with tax or support arrears, or worried that not all of your property is protected, Chapter 13 may deserve more attention.

Deadlines matter too. If a foreclosure sale, repossession, lawsuit, or wage garnishment is already on the calendar, waiting can close off options. Bankruptcy can offer strong protection, but it works best when you act before things go too far.

Bankruptcy in Tennessee at a Glance

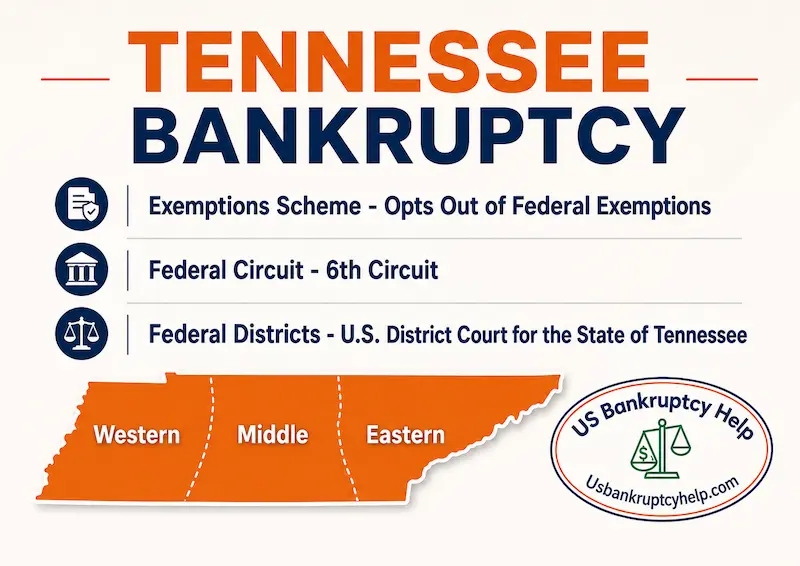

Bankruptcy in Tennessee is mostly governed by federal law, but Tennessee rules still affect the outcome. Tennessee exemptions, Tennessee median income figures, local court procedures, and the district where your case is filed can all matter.

- Most common consumer options: Individuals in Tennessee usually consider chapter 7 or chapter 13 bankruptcy.

- Chapter 7: May provide a faster discharge of qualifying unsecured debts, such as credit cards, medical bills, personal loans, and many collection accounts.

- Chapter 13: May help if you need time to catch up on a mortgage, car loan, taxes, support arrears, or other debts through a repayment plan.

- Tennessee exemptions: Tennessee generally requires filers to use Tennessee exemptions instead of the federal bankruptcy exemption list.

- Means test: Tennessee median income figures are used in the chapter 7 means test, which can affect whether chapter 7 is available or whether chapter 13 should be reviewed.

- Automatic stay: Filing bankruptcy usually creates an automatic stay that can pause many collection actions, including lawsuits, garnishments, foreclosure activity, repossession efforts, and collection calls.

- Where cases are filed: Tennessee bankruptcy cases are filed in one of three federal bankruptcy districts: Eastern, Middle, or Western Tennessee.

- Required courses: Most consumer filers must complete credit counseling before filing and debtor education after filing to receive a discharge.

- The key question: The right path depends on what problem you need bankruptcy to solve, what property you need to protect, and whether chapter 7 or chapter 13 gives you a realistic way forward.

Chapter 7 vs. Chapter 13 Bankruptcy in Tennessee

Most people in Tennessee who file for bankruptcy end up in either Chapter 7 or Chapter 13. The right fit depends on your income, what you own, the kinds of debts you have, where you’re falling behind, and what you need bankruptcy to actually do for you.

Chapter 7 is usually the go‑to option when your main goal is to wipe out qualifying unsecured debts—things like credit cards, medical bills, personal loans, and collection accounts. Chapter 13 is more common when you need time and structure to catch up on a mortgage or car loan, stop foreclosure, prevent repossession, protect property, or deal with debts that need more careful treatment.

| Issue | Chapter 7 in Tennessee | Chapter 13 in Tennessee |

|---|---|---|

| Main purpose | Focuses on getting rid of qualifying unsecured debts as quickly as the law allows. | Uses a court‑approved repayment plan to help you catch up, protect property, and deal with debts over time. |

| Typical timeline | In a straightforward case, many Chapter 7s finish in several months. | Usually lasts three to five years because you make monthly plan payments. |

| Income issue | The Chapter 7 means test looks at Tennessee median income and other income and expense rules to see if you qualify. | You need steady income that’s high enough to support a realistic plan payment each month. |

| Property issue | Tennessee exemptions help determine what property appears protected. Anything that is not exempt can create risk in Chapter 7. | You can often keep property, but any nonexempt value may increase how much you have to pay through the plan. |

| Mortgage arrears | Chapter 7 may pause a foreclosure temporarily, but it usually doesn’t give you a long‑term way to catch up on missed mortgage payments. | Chapter 13 may let you spread missed mortgage payments over the life of the plan while you keep making your regular monthly payments. |

| Car loan arrears | Chapter 7 may temporarily stop repossession, but it generally does not provide a built‑in structure to catch up on the loan. | Chapter 13 may let you deal with missed car payments in the plan and can stop repossession if you file in time. |

| Best fit | Often worth considering if unsecured debt is your main problem and your property seems safely covered by Tennessee exemptions. | Often worth considering if you need more time, structure, or protection than Chapter 7 can offer. |

The real question isn’t which chapter is “better” overall; it’s which chapter actually solves the problem you have. If you mostly need relief from unsecured debt and your property appears protected, Chapter 7 may be a good place to start. If you are behind on a house or car, facing foreclosure or repossession, dealing with priority debts, or trying to protect property that may not be fully exempt, Chapter 13 may deserve more attention.

Not sure whether Chapter 7 or Chapter 13 fits your Tennessee situation?

You can use the decision tool below to walk through common bankruptcy decision points, including income, household size, secured debt issues, property risk, foreclosure risk, repossession risk, and your main reason for considering bankruptcy.

- Compares Chapter 7 and Chapter 13 based on your answers

- Uses your state and household information as part of the analysis

- Flags common reasons Chapter 13 might need a closer look

- Helps you organize the issues before you meet with a bankruptcy attorney

- Does not ask for your name, email address, or phone number to show results

This tool is not legal advice, but it can help you think through the right questions before you decide what to do next.

Chapter 7 vs Chapter 13 Decision Tool

Answer a few questions to get an educational estimate of which bankruptcy chapter may fit your situation.

Step 1 of 2

Window 1 of 2: Income Snapshot

ZIP lookup is optional and used as a quick state check.

Chapter 7 Bankruptcy in Tennessee

In Tennessee, Chapter 7 bankruptcy is often used by people whose biggest problem is unsecured debt like credit cards, medical bills, personal loans, collection accounts, old utility bills, or deficiency balances after a repossession. In a successful Chapter 7 case, qualifying debts are wiped out without a three‑to‑five‑year repayment plan.

Chapter 7 can be a powerful way to get debt relief, but it is more than just listing what you owe and filing forms. A Tennessee filer still needs to look at income, eligibility, property, exemptions, bank balances, tax refunds, lawsuits, recent transfers, and whether Chapter 7 actually fixes the problem they are trying to solve.

When Chapter 7 May Make Sense in Tennessee

Chapter 7 may be worth reviewing if your main goal is to discharge qualifying unsecured debt and your property appears protected by Tennessee exemptions.

- Credit cards, medical bills, or personal loans are your main problem.

- Collectors are calling, sending letters, or have filed a lawsuit against you.

- Your wages are being garnished, or may be, for debts that can be discharged.

- You do not need a long‑term plan to catch up on a mortgage or car loan.

- Your income appears to fit within the Chapter 7 means test rules.

- Your home, vehicle, bank accounts, and other property seem protected by Tennessee exemptions.

- You have not recently transferred valuable property or repaid family members in a way that could create problems.

When Chapter 7 May Not Be Enough

Chapter 7 is not the right answer for every Tennessee filer. It can wipe out many unsecured debts, but it usually does not give you a long‑term structure to catch up on missed mortgage payments, missed car payments, priority taxes, or domestic support arrears.

- If you are behind on your mortgage and want to keep the home, Chapter 13 may need to be considered.

- If your vehicle is at risk of repossession and you need time to catch up, Chapter 13 may offer more structure.

- If you own property that is not fully protected by Tennessee exemptions, Chapter 7 may create property risk.

- If your income is too high for Chapter 7, Chapter 13 may be the more realistic option.

- If you owe recent taxes, domestic support obligations, or other debts that are not easily discharged, Chapter 7 may not solve the whole problem.

The Tennessee Chapter 7 Means Test

The Chapter 7 means test is a federal eligibility formula that uses Tennessee‑specific median income numbers. It generally looks at your household income during the six months before you file, annualizes that amount, and compares it to the Tennessee median income for a household of your size.

If your income is below the applicable Tennessee median income, you usually pass the first part of the means test. If your income is above median, the analysis continues by subtracting allowed expenses to see whether there is enough disposable income to repay creditors in a Chapter 13 case instead.

The Chapter 7 means test can be affected by:

- Your household size

- Your gross income during the six‑month lookback period

- Changes in income, overtime, bonuses, commissions, or job loss

- Business income or self‑employment income

- Social Security income and other benefit income

- Mortgage, car, tax, support, insurance, and other allowed expenses

- Whether your debts are mainly consumer debts or business debts

The means test matters, but it is not the only Chapter 7 question. A Tennessee filer can pass the means test and still have a property issue, recent transfer issue, lawsuit, tax refund, or specific debt that needs a closer look before filing.

Tennessee Median Income for the Chapter 7 Means Test

The first step of the Chapter 7 means test compares your household income to the Tennessee median income for your household size. These figures are published by the U.S. Trustee Program and are used when completing bankruptcy means test forms.

For bankruptcy cases filed between April 1, 2026 and July 14, 2026, the Tennessee median income figures are:

| Household Size | Tennessee Median Income |

|---|---|

| 1 person | $63,979 |

| 2 people | $82,846 |

| 3 people | $97,511 |

| 4 people | $109,585 |

| Each additional person over 4 | Add $11,100 |

Source:U.S. Trustee Program median income table for cases filed between April 1, 2026 and July 14, 2026.

Median income figures change from time to time. If you are filing after July 14, 2026, make sure you are using the current Tennessee median income numbers before relying on this table.

Use the Tennessee Chapter 7 Means Test Calculator

Use the calculator below to choose Tennessee, enter your household size, income, and basic expense information, and estimate whether you may be below or above the Tennessee median income line. If you are below the applicable Tennessee median income, Chapter 7 may be easier to evaluate. If you are above median, the calculator can help show why a more detailed means test review may be needed.

The Tennessee means test calculator can help you estimate:

- Whether your household income is above or below the Tennessee median income for your household size

- Whether Chapter 7 appears worth reviewing based on the first step of the means test

- Whether a more detailed means test analysis may be needed if your income is above the Tennessee median

- Whether Chapter 13 may deserve a closer look if the means test creates a problem

The Chapter 7 means test calculator is not legal advice, but it gives Tennessee filers a state‑specific starting point instead of a generic national estimate.

Chapter 7 Means Test Calculator

Estimate whether your household income is above or below your state’s median income for educational planning.

Educational estimate only. This Chapter 7 means test calculator is not legal advice, does not create an attorney-client relationship, and cannot account for every legal nuance. Attorney review may still be necessary.

Step 1: Initial Screening

If filing alone, household starts at 1. If filing jointly, household starts at 2. Add only additional dependents here.

Consumer debts are usually personal, family, or household debts.

Median-income dataset effective April 1, 2026. IRS/local standards preset date: Configurable - update with current IRS + USTP data. Presumption thresholds: $10,025 and $16,700 (60-month).

Tennessee Exemptions and Chapter 7 Property Risk

In Chapter 7, Tennessee exemptions help determine whether your property appears protected. Exemptions can affect home equity, vehicle equity, bank balances, tax refunds, household goods, tools, benefits, retirement accounts, lawsuits, and other assets.

If everything is fully protected by Tennessee exemptions, Chapter 7 may be less risky from a property standpoint. If something is not fully protected, the Chapter 7 trustee may look at whether nonexempt value can be used to pay creditors.

Before filing Chapter 7 in Tennessee, check:

- What your home is worth and how much you still owe on it

- What your vehicle is worth and the current loan payoff

- How much money is in your bank accounts

- Whether you are expecting a tax refund

- Whether you own valuable personal property, tools, or business assets

- Whether you have a lawsuit, injury claim, inheritance, or settlement

- Whether you recently transferred property or repaid family members

- Whether Tennessee exemptions protect the property that matters most to you

Passing the means test does not automatically mean Chapter 7 is the right choice. You still need to look at Tennessee exemptions, property values, recent transfers, tax refunds, lawsuits, secured debts, and whether Chapter 7 actually solves the problem you are trying to fix.

Chapter 13 Bankruptcy in Tennessee

Chapter 13 bankruptcy in Tennessee is the repayment plan chapter. Instead of getting a faster discharge like in Chapter 7, you propose a court-approved plan that usually lasts three to five years. During that time, you make monthly payments through the Chapter 13 trustee.

Chapter 13 may be worth reviewing when you need time, structure, or protection that Chapter 7 does not provide. It is often used by Tennessee filers who are behind on a mortgage, behind on a car loan, facing foreclosure, trying to stop repossession, dealing with tax debt, or trying to keep property that might not be fully protected in Chapter 7.

When Chapter 13 May Make Sense in Tennessee

Chapter 13 may be a better fit when discharging unsecured debt alone would not solve your financial problem. It can give you a structured way to catch up on certain debts while you keep important property.

- You are behind on your mortgage and want to keep your home.

- Foreclosure has been threatened or a sale has been scheduled.

- You are behind on a car loan and want to stop repossession.

- You need time to catch up on missed payments on secured debts.

- You owe recent taxes that may not be discharged in Chapter 7.

- You owe domestic support arrears that need to be paid through a plan.

- Your income is too high or too complex for a straightforward Chapter 7.

- You own property that may not be fully protected by Tennessee exemptions.

- You need a repayment structure that fits your budget better than lawsuits or wage garnishments.

How a Tennessee Chapter 13 Plan Works

In Chapter 13, you file a proposed repayment plan with the bankruptcy court. The plan explains how much you will pay each month, how long the plan will last, and how different types of creditors will be treated.

Your plan payment depends on your income, expenses, debts, arrears, property, exemptions, trustee fees, attorney fees, and the rules that apply to your case. Two Tennessee filers with the same amount of credit card debt may have very different Chapter 13 payments if one is behind on a mortgage, has tax debt, or owns property that is not fully protected by exemptions.

A Tennessee Chapter 13 plan may need to account for:

- Regular monthly income and necessary living expenses

- Missed mortgage payments if you are trying to keep a home

- Missed car payments if you are trying to keep a vehicle

- Vehicle loan treatment, including any possible cramdown issues where allowed

- Recent income taxes or other priority tax debts

- Domestic support arrears

- Attorney fees and trustee fees

- Nonexempt property value that unsecured creditors may need to receive

- Plan length, usually three to five years

Chapter 13 and Tennessee Mortgage Arrears

Chapter 13 can be especially important for Tennessee homeowners who are behind on mortgage payments. Chapter 7 may temporarily pause foreclosure through the automatic stay, but it usually does not give you a long-term way to catch up on missed payments.

Chapter 13 may allow you to spread mortgage arrears over the plan while you resume your regular monthly mortgage payment. This can make Chapter 13 a better fit if your main goal is to stop foreclosure and keep your home.

- The bankruptcy filing may stop a pending foreclosure if you file in time.

- Missed mortgage payments may be paid through the Chapter 13 plan.

- You usually must keep making regular mortgage payments after filing.

- The plan must be realistic based on your income and budget.

- Waiting too long can limit your options if a foreclosure sale is close.

Chapter 13 and Tennessee Car Loans

Chapter 13 may also help Tennessee filers who are behind on a vehicle loan or facing repossession. If you file in time, the automatic stay may stop repossession, and the plan may give you a way to handle missed payments inside the case.

In some situations, Chapter 13 can also change how certain vehicle loans are treated in the plan. The exact result depends on the vehicle value, loan balance, purchase date, interest rate, and whether the plan satisfies bankruptcy rules.

- Chapter 13 may stop repossession if the vehicle has not already been taken or sold.

- Missed car payments may be dealt with through the repayment plan.

- You may be able to keep the vehicle if the plan is feasible and meets legal requirements.

- Vehicle value, loan balance, and timing can affect how the car debt is treated.

- If a car has already been repossessed, timing becomes urgent and very fact-specific.

Chapter 13 and Tennessee Exemptions

Tennessee exemptions still matter in Chapter 13, but the issue is different than in Chapter 7. In Chapter 7, nonexempt property may create risk because a trustee can look for value for creditors. In Chapter 13, you usually keep your property, but nonexempt value can affect how much unsecured creditors must receive through the plan.

This is why property values still matter in Chapter 13. Home equity, vehicle equity, tax refunds, bank balances, lawsuits, business assets, and other property can all affect the plan if they are not fully protected by Tennessee exemptions.

Use the Tennessee Chapter 13 Plan Payment Calculator

If you are considering Chapter 13 bankruptcy in Tennessee, the practical question is whether a plan payment may be realistic. A chapter 13 payment is not based only on credit card debt. It can also be affected by Tennessee property exemption issues, mortgage arrears, vehicle arrears, tax debts, support arrears, trustee fees, attorney fees, and the value of any property that may not be fully protected.

Use the calculator below to select Tennessee and enter your income, household expenses, secured debt arrears, priority debts, attorney fees, and estimated nonexempt property value. The calculator gives Tennessee filers a way to model the numbers that commonly drive a chapter 13 plan, including whether Tennessee exemption limits may leave nonexempt property value that needs to be paid through the plan.

The Tennessee Chapter 13 calculator can help you estimate:

- Whether a proposed monthly plan payment may fit your budget

- How Tennessee mortgage arrears may affect a plan payment

- How Tennessee vehicle loan arrears may affect a plan payment

- How tax debts or support arrears may affect the plan

- How Tennessee exemption issues and nonexempt property value may affect what unsecured creditors must receive

- Whether chapter 13 deserves a closer look before deciding whether to file bankruptcy in Tennessee

The calculator is not legal advice, but it gives Tennessee filers a state-specific way to organize the income, debt, arrears, and exemption issues that often determine whether chapter 13 is realistic.

Chapter 13 Plan Payment Calculator

Chapter 13 plan payments depend on many factors, including local court and trustee practices. This tool gives an educational estimate only, not legal advice.

Median-income reference date: April 1, 2026.

Tennessee Bankruptcy Exemptions: Why They Matter Before You File

Tennessee bankruptcy exemptions help decide what property may be protected if you file bankruptcy in Tennessee. Exemptions can affect home equity, vehicle equity, bank accounts, tax refunds, household goods, tools, benefits, retirement accounts, lawsuits, and other assets.

Exemptions matter in both Chapter 7 and Chapter 13. In Chapter 7, Tennessee exemptions help determine whether a trustee may review nonexempt property for the benefit of creditors. In Chapter 13, you usually keep your property, but any nonexempt value can affect how much unsecured creditors must receive through the repayment plan.

Tennessee is generally an opt-out state, which means Tennessee filers usually use Tennessee exemptions instead of the federal bankruptcy exemption list. Exemption analysis is not just a list of dollar amounts. You still need to know what you own, what each item is worth, how much you owe against it, and whether Tennessee exemptions protect the equity or value.

Before relying on Tennessee exemptions, ask:

- Do you own a home or have equity in real estate?

- Do you own a car, truck, motorcycle, or other vehicle?

- How much money will be in your bank accounts on the filing date?

- Are you expecting a tax refund?

- Do you own tools, business property, or valuable personal property?

- Do you receive Social Security, disability, retirement, or other benefits?

- Do you have a lawsuit, injury claim, inheritance, or settlement?

- Have you recently moved to Tennessee from another state?

- Would nonexempt property make Chapter 13 feel safer than Chapter 7?

If you moved to Tennessee recently, be especially careful. Bankruptcy exemption rules can depend on how long you have lived in the state before you file. If you moved from another state, you may need a separate domicile analysis before you rely on Tennessee exemption amounts.

Where to Review Tennessee Exemption Amounts

This Tennessee home page gives the big picture. The detailed exemption analysis belongs on the dedicated Tennessee exemptions page. That page explains Tennessee exemption categories, current amounts, common risk areas, and how exemptions affect both Chapter 7 and Chapter 13.

For the full Tennessee-specific breakdown, review our Tennessee bankruptcy exemptions guide.

The main point is simple. Do not assume bankruptcy automatically protects everything you own. Before you file, review what property you have, estimate the equity or value, compare it to Tennessee exemptions, and decide whether Chapter 7 appears safe or whether Chapter 13 may offer a better way to protect property while you deal with debt.

Keeping Your House in Tennessee Bankruptcy

Many Tennessee homeowners who are thinking about bankruptcy want to know one thing first: can you file for bankruptcy and keep your house? The answer usually depends on four key points. Those points are the chapter you file, how much equity you have, whether you are current or behind on the mortgage, and whether Tennessee exemptions protect your home equity.

Bankruptcy does not automatically erase a mortgage. If you want to keep your home, you usually need to protect any equity and either stay current on the mortgage or use Chapter 13 to catch up on missed payments.

For Tennessee homeowners, the main questions are:

- What is the home realistically worth?

- How much is owed on the mortgage and any other liens?

- How much equity needs exemption protection?

- Are you current or behind on mortgage payments?

- Has foreclosure been threatened or scheduled?

- Would Chapter 7 or Chapter 13 better solve the problem?

In Chapter 7, Tennessee exemptions help show whether your home equity appears protected. If the equity is not fully covered, Chapter 7 may create property risk. In Chapter 13, you may be able to keep the home and catch up on mortgage arrears through a repayment plan, as long as the payment is realistic for your budget.

For the full Tennessee homestead exemption breakdown, including current exemption amounts and examples, review our Tennessee bankruptcy exemptions guide.

Keeping Your Car in Tennessee Bankruptcy

Many people who file bankruptcy in Tennessee need to keep a car for work, family, medical care, and everyday life. Whether bankruptcy can help you keep a vehicle depends on the chapter you file, whether you are current or behind on the loan, how much equity you have, and whether Tennessee exemptions protect that equity.

A car loan and vehicle equity are two different issues. If you want to keep a financed vehicle, you usually need to protect the equity and either stay current on the loan or use Chapter 13 to deal with missed payments.

For Tennessee vehicle owners, the main questions are:

- What is the vehicle realistically worth?

- How much is owed on the loan payoff?

- Is the vehicle paid off or still financed?

- How much equity needs exemption protection?

- Are you current or behind on payments?

- Has repossession been threatened or already happened?

- Would Chapter 7 or Chapter 13 better solve the problem?

In Chapter 7, Tennessee exemptions help show whether your vehicle equity appears protected. Tennessee generally does not use a separate motor vehicle exemption in the way many states do, so car equity is often reviewed as part of the broader Tennessee personal property exemption analysis. In Chapter 13, you may be able to keep the vehicle while you deal with missed payments through the plan.

For the full Tennessee vehicle exemption discussion, including how Tennessee personal property exemptions may apply to car equity, review our Tennessee bankruptcy exemptions guide.

What Bankruptcy Can Stop in Tennessee

Filing bankruptcy in Tennessee usually creates an automatic stay. The automatic stay is a court protection that can pause many collection actions as soon as the case is filed. This pause can give you time to breathe, get organized, and move through Chapter 7 or Chapter 13 without every creditor acting at the same time.

The automatic stay is powerful, but it is not unlimited. It does not erase every debt, and it does not permanently fix every secured debt problem. What it can do depends on the type of debt, what the creditor is doing, whether you have filed bankruptcy before, and whether Chapter 7 or Chapter 13 actually addresses the underlying issue.

| Problem | What Bankruptcy May Do | What to Watch For |

|---|---|---|

| Collection calls and letters | The automatic stay usually stops most creditors and collectors from continuing collection efforts after they receive notice of the case. | Make sure every creditor and collection agency is listed with a correct mailing address so they get notice. |

| Creditor lawsuits | Bankruptcy usually pauses lawsuits that are trying to collect dischargeable debts. | Tell your bankruptcy attorney about any pending lawsuit, court date, or judgment so it can be addressed in the case. |

| Wage garnishment | Bankruptcy can usually stop wage garnishment for dischargeable debts once the case is filed. | Your payroll department and the garnishing creditor may need notice before the garnishment actually stops. |

| Bank levies | Bankruptcy may stop or prevent certain collection-related levies after filing. | Timing matters. Money that has already been taken before filing can be harder to recover. |

| Foreclosure | Bankruptcy may stop or pause foreclosure activity if the case is filed before the sale is completed. | Chapter 7 may only pause the problem for a short time. Chapter 13 may be needed if you want a way to catch up on mortgage arrears. |

| Repossession | Bankruptcy may stop repossession efforts if you file before the vehicle is taken or sold. | If the car has already been repossessed, timing becomes urgent and very fact-specific. |

| Utility shutoff | Bankruptcy may provide temporary protection from a utility shutoff or help restore service in some situations. | The utility company may require an adequate assurance deposit or other protection after you file. |

What Bankruptcy Usually Does Not Stop Permanently

Bankruptcy can pause many collection actions, but that does not mean every problem is permanently fixed the moment you file. Some debts still require ongoing payments, special treatment, or a Chapter 13 repayment plan.

- A mortgage lender will still expect regular mortgage payments if you want to keep the home.

- A car lender will still expect the vehicle loan to be handled if you want to keep the car.

- Domestic support obligations usually continue and are not discharged.

- Some tax debts may survive bankruptcy or require special treatment.

- Criminal fines, restitution, and some government obligations may not be stopped or discharged in the same way as ordinary unsecured debt.

- Repeat bankruptcy filings can limit or change how the automatic stay applies.

If you are facing an urgent Tennessee collection problem, check:

- Has a lawsuit already been filed?

- Is there a garnishment order?

- Is a foreclosure sale scheduled?

- Has a repossession company contacted you?

- Has the car already been taken?

- Have you filed bankruptcy in the last year?

- Do you need Chapter 13 to catch up, or is Chapter 7 enough?

The main idea is that bankruptcy can often stop the immediate pressure, but the chapter you choose matters. Chapter 7 may be enough when the main problem is dischargeable unsecured debt. Chapter 13 may be a better fit when you need time to catch up on a house, car, taxes, support arrears, or other debts that require a structured repayment plan.

How to File Bankruptcy in Tennessee

Filing bankruptcy in Tennessee is a federal court process, but the choices you make before you file can affect your property, your budget, your case timeline, and whether Chapter 7 or Chapter 13 is the better fit. The goal is not just to file a case. The goal is to file the right chapter, in the right district, with accurate information and a clear plan.

Most Tennessee consumer bankruptcy cases follow a similar path. You identify the problem, compare Chapter 7 and Chapter 13, review exemptions, complete the required credit counseling course, gather documents, file the bankruptcy forms, attend the 341 meeting, complete debtor education, and then move toward discharge or Chapter 13 plan completion.

Step 1: Decide What Problem Bankruptcy Needs to Solve

Before you choose a chapter, start with the problem you need bankruptcy to fix. A person who mainly has credit card debt or medical bills may need a different approach than someone trying to stop foreclosure, prevent repossession, end a wage garnishment, or protect property with equity.

- Are credit cards, medical bills, or personal loans the main issue?

- Are you being sued or garnished?

- Are you behind on a mortgage or car loan?

- Is foreclosure or repossession urgent?

- Do you own property that may not be fully protected?

- Do you owe taxes, support arrears, or other debts that need special treatment?

Step 2: Compare Chapter 7 and Chapter 13

Chapter 7 may make sense if your main goal is to discharge qualifying unsecured debt and your property appears protected by Tennessee exemptions. Chapter 13 may make more sense if you need time to catch up on a house, car, taxes, support arrears, or nonexempt property value through a repayment plan.

This choice matters because Chapter 7 and Chapter 13 solve different problems. Chapter 7 is usually faster, but it may not give you a long-term way to catch up on secured debt. Chapter 13 takes longer, but it may give you more tools if you are behind on payments or need to protect property.

Step 3: Review Tennessee Exemptions and Property Risk

Before you file, review what property you own and whether Tennessee exemptions appear to protect it. Exemptions can affect home equity, vehicle equity, bank balances, tax refunds, household goods, tools, benefits, retirement accounts, lawsuits, inheritances, and other assets.

This step is important in both chapters. In Chapter 7, nonexempt property may create risk because a trustee can look for value for creditors. In Chapter 13, nonexempt value can affect how much unsecured creditors must receive through the repayment plan.

Step 4: Complete the Required Credit Counseling Course

Before most consumer bankruptcy cases are filed, you must complete a credit counseling course from an approved provider. The course is usually done online or by phone. After you finish, you receive a certificate that must be filed with the bankruptcy case.

Timing matters. The certificate must be current when the case is filed. If you are working with a Tennessee bankruptcy attorney, they will usually tell you when to take the course and where to send the certificate.

Step 5: Gather Financial Documents

Bankruptcy forms require a complete picture of your financial situation. Before filing in Tennessee, you should gather income records, tax returns, bank statements, debt information, property values, titles, loan balances, and documents related to lawsuits, garnishments, foreclosures, repossessions, transfers, or business ownership.

Common documents to gather before filing include:

- Recent pay stubs or other proof of income

- Recent tax returns, if required in your situation

- Bank statements

- Mortgage statements and payoff information

- Vehicle loan statements and payoff information

- Credit card, medical bill, loan, and collection account information

- Copies of lawsuits, judgments, garnishment papers, or foreclosure notices

- Vehicle titles, deeds, leases, and insurance information

- Retirement, benefit, life insurance, and investment account statements

- Information about recent transfers, sales, gifts, or payments to family members

Step 6: File in the Correct Tennessee Bankruptcy District

Tennessee bankruptcy cases are filed in federal bankruptcy court. The state has three bankruptcy districts: Eastern, Middle, and Western Tennessee. The correct district generally depends on where you live, where your main assets are located, or where your business is based.

Filing in the right district matters because each district has its own local procedures, trustees, clerk’s offices, and court practices. A Tennessee bankruptcy attorney can help you confirm the correct district and division before the case is filed.

Step 7: File the Bankruptcy Petition, Schedules, and Statements

The bankruptcy filing includes a petition, schedules, statements, income and expense information, debt lists, property disclosures, exemption claims, and other required forms. These documents must be accurate and complete.

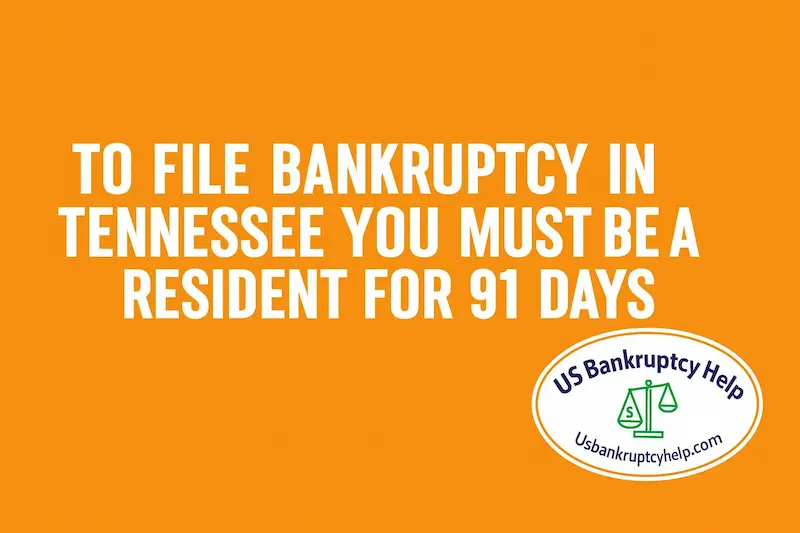

If you’re thinking about bankruptcy and recently moved, where you can file your case matters. In most situations, you can file in Tennessee if you’ve lived, worked, or kept most of your property in Tennessee for the greater part of the last 180 days (91 days). For many people, that means being in Tennessee for at least 91 of those days. Keep in mind, though, that the place where you file your case (the “venue”) is different from the rules that decide which state’s bankruptcy exemptions you can use. Those exemption rules follow separate domicile guidelines.

Once the case is filed, the automatic stay usually begins. The automatic stay can pause many collection actions, including collection calls, lawsuits, wage garnishments, foreclosure activity, and repossession efforts. The protection can be limited in some repeat filing situations, so any prior bankruptcy cases should be reviewed before you file.

Step 8: Attend the 341 Meeting of Creditors

After filing, you attend a 341 meeting of creditors. This is a required meeting where the trustee asks questions under oath about your bankruptcy papers, income, property, debts, transfers, and financial history. Creditors may attend, but in many consumer cases they do not.

The 341 meeting is not usually a courtroom trial, and there is no judge deciding your case at the meeting. Even so, it is an important part of the process. You should review your paperwork beforehand and be ready to answer questions honestly and clearly.

Step 9: Complete Debtor Education After Filing

After the case is filed, most consumer filers must complete a second course called debtor education or financial management. This course must be completed before a discharge is entered.

If the debtor education certificate is not filed on time, the court may close the case without entering a discharge. That means the debts may not be wiped out even though the case was filed.

Step 10: Move Toward Discharge or Chapter 13 Plan Completion

In a Chapter 7 case, the goal is usually a discharge after the trustee review, 341 meeting, and required deadlines have passed. In a Chapter 13 case, the case continues while you make payments under the court approved repayment plan.

The result depends on the chapter. Chapter 7 usually moves faster, while Chapter 13 requires ongoing plan payments, budget discipline, and compliance with the confirmed plan.

Before filing bankruptcy in Tennessee, make sure you have reviewed:

- Which chapter actually solves your main problem

- Whether you qualify for Chapter 7 under the Tennessee means test

- Whether Tennessee exemptions protect your property

- Whether you are current or behind on house or car payments

- Whether any lawsuit, garnishment, foreclosure, or repossession is urgent

- Whether you have recent transfers, family repayments, or unusual transactions

- Which Tennessee bankruptcy district is the correct filing court

- Whether you have completed credit counseling before filing

The main point is that filing bankruptcy in Tennessee should be a planned decision, not just a rush to file paperwork. A careful filing starts with the problem you need to solve, then reviews chapter choice, income eligibility, exemptions, court district, documents, and timing before the case is filed.

Tennessee Bankruptcy Courts: Where to File

Tennessee bankruptcy cases are filed in federal bankruptcy court, not in state court. The state is divided into three federal bankruptcy districts: the Eastern District of Tennessee, the Middle District of Tennessee, and the Western District of Tennessee.

The correct district usually depends on where you live, where your main assets are located, or where your business is based. Each district has its own clerk’s office, judges, trustees, local procedures, and hearing locations. Filing in the correct district helps you avoid delays and procedural problems.

Before filing, check:

- Which Tennessee bankruptcy district covers your county

- Whether your case belongs in the Eastern, Middle, or Western District

- Which clerk’s office or filing location applies

- Whether hearings or 341 meetings are in person, by phone, or by video

- Whether local rules or trustee procedures affect your case

Tennessee Bankruptcy Court Locations

| District | Courthouse / Location | Address | Phone | Official Website |

|---|---|---|---|---|

| Middle District of Tennessee | Nashville — U.S. Customs House / Clerk’s Office | 701 Broadway, Room 170, Nashville, TN 37203 | (615) 736-5584 | tnmb.uscourts.gov |

| Middle District of Tennessee | Columbia — Federal Building and Courthouse (unstaffed) | 815 South Garden St., Columbia, TN 38401 | Use Nashville clerk’s office | Columbia location |

| Middle District of Tennessee | Cookeville — L. Clure Morton Post Office and Courthouse (unstaffed) | 9 E Broad St., Cookeville, TN 38503 | Use Nashville clerk’s office | Cookeville location |

| Western District of Tennessee | Memphis — Clerk’s Office | 200 Jefferson Ave., Suite 500, Memphis, TN 38103 | (901) 328-3500 | tnwb.uscourts.gov |

| Western District of Tennessee | Jackson — U.S. Courthouse / Clerk’s Office | 111 South Highland Ave., Suite 107, Jackson, TN 38301 | (731) 421-9300 | tnwb.uscourts.gov |

| Eastern District of Tennessee | Chattanooga — Historic U.S. Courthouse | 31 East 11th Street, Chattanooga, TN 37402-2722 | (423) 752-5163 | Chattanooga location |

| Eastern District of Tennessee | Knoxville — Howard H. Baker Jr. U.S. Courthouse | 800 Market Street, Suite 330, Knoxville, TN 37902 | (865) 545-4279 | tneb.uscourts.gov |

| Eastern District of Tennessee | Greeneville — James H. Quillen United States Courthouse | 220 West Depot Street, Suite 218, Greeneville, TN 37743-4924 | (423) 787-0113 | Greeneville location |

| Eastern District of Tennessee | Winchester — U.S. Post Office and Courthouse (unstaffed) | 200 South Jefferson Street, Second Floor Courtroom, Winchester, TN 37398 | (423) 752-5163 | Winchester location |

Court locations and procedures can change. Before you file or appear for a hearing, confirm the correct district, address, hearing format, and clerk’s office instructions on the official court website or with a Tennessee bankruptcy attorney.

Filing Readiness Checklist for Tennessee Bankruptcy Cases

Before you file bankruptcy in Tennessee, it helps to pause and make sure the major issues have been reviewed. A bankruptcy case can provide strong protection, but mistakes with income, property, exemptions, documents, or timing can create problems after the case is filed.

This checklist is not a do-it-yourself filing guide. It is a practical way to organize the information that usually matters before you choose Chapter 7, Chapter 13, or another strategy.

Before filing bankruptcy in Tennessee, review:

- Your main reason for filing: whether the real problem is credit cards, medical bills, lawsuits, garnishment, foreclosure, repossession, tax debt, support arrears, or something else.

- Chapter choice: whether Chapter 7 or Chapter 13 better solves the problem you are actually facing.

- Chapter 7 eligibility: whether your household income appears to fit within the Tennessee Chapter 7 means test rules.

- Chapter 13 feasibility: whether a repayment plan could realistically fit your monthly income and expenses.

- Home equity: what your home is worth, what you owe, and whether Tennessee exemptions appear to protect the equity.

- Vehicle equity: what your car is worth, the loan payoff, and whether Tennessee exemptions appear to protect the equity.

- Bank accounts and cash: how much money is likely to be in your accounts on the filing date.

- Tax refunds: whether you are expecting a federal or state refund that may need exemption protection.

- Lawsuits and claims: whether you have a personal injury claim, employment claim, insurance claim, inheritance, or settlement.

- Recent transfers: whether you sold, gave away, retitled, or transferred property shortly before filing.

- Family repayments: whether you recently repaid relatives, friends, business partners, or other insiders.

- Secured debts: whether you are current or behind on your mortgage, car loan, furniture loan, or other secured debts.

- Priority debts: whether you owe recent taxes, domestic support obligations, or other debts that may need special treatment.

- Required courses: whether you have completed approved credit counseling before filing and understand the debtor education requirement after filing.

- Correct court district: whether your case belongs in the Eastern, Middle, or Western District of Tennessee.

Documents to Gather Before Filing

A Tennessee bankruptcy case requires a full picture of your income, expenses, property, debts, and recent financial activity. Gathering documents early can help you avoid delays and reduce surprises after filing.

- Recent pay stubs or other proof of income

- Benefit letters or proof of Social Security, disability, unemployment, or retirement income

- Recent federal tax returns

- Recent bank statements for all accounts

- Mortgage statements, payoff figures, and any foreclosure notices

- Vehicle loan statements, payoff figures, titles, and any repossession notices

- Credit card, medical bill, personal loan, and collection account information

- Lawsuit, judgment, garnishment, or other collection paperwork

- Retirement, investment, life insurance, and benefit account statements

- Property deeds, leases, business records, or title documents

- Documents showing recent property sales, transfers, gifts, or family repayments

Red Flags to Review Before Filing

Some issues should be reviewed before a Tennessee bankruptcy case is filed because they can affect timing, exemptions, trustee questions, or chapter choice.

- A foreclosure sale date is already scheduled.

- Your vehicle has been repossessed or repossession is very close.

- Your wages are being garnished or a garnishment order has been entered.

- You recently moved to Tennessee from another state.

- You own a home, paid off vehicle, business, tools, or other valuable property.

- You are expecting a tax refund, lawsuit recovery, inheritance, or settlement.

- You recently paid back a family member or transferred property.

- Your income recently changed because of overtime, job loss, bonuses, commissions, or self-employment.

- You have filed bankruptcy before.

The main idea is that a good Tennessee bankruptcy filing begins before the paperwork is submitted. Review the problem you need to solve, gather the documents, check eligibility and exemptions, identify red flags, and make sure the chapter you choose matches your actual goals.

Common Tennessee Bankruptcy Mistakes

Bankruptcy can be a powerful tool, but mistakes made before filing can make a Tennessee case harder than it needs to be. Many problems come from waiting too long, guessing at property values, ignoring exemptions, moving money around, or choosing Chapter 7 when Chapter 13 would have been safer.

The goal is not to scare you away from bankruptcy. The goal is to help you spot issues early, before they create problems with the trustee, the court, or the property you want to protect.

1. Waiting Until the Last Minute

Many people wait until a garnishment has started, a foreclosure sale is near, or a repossession is about to happen before asking for help. Bankruptcy may still help in an emergency, but waiting too long can limit your options.

If a lawsuit, garnishment, foreclosure, or repossession is already moving ahead, timing matters. A planned filing is usually safer than a rushed emergency filing.

2. Choosing Chapter 7 Without Reviewing Chapter 13

Chapter 7 may be a strong option when unsecured debt is the main problem and your property appears protected. However, Chapter 7 usually does not give you a long-term way to catch up on mortgage arrears, car arrears, priority taxes, or support arrears.

If you are behind on a house or car, facing foreclosure or repossession, or trying to protect property that may not be fully exempt, Chapter 13 should be reviewed before you file.

3. Assuming Tennessee Exemptions Protect Everything

Tennessee exemptions can protect important property, but they are not unlimited. Home equity, vehicle equity, bank balances, tax refunds, lawsuits, business assets, tools, and other property usually need a careful exemption review.

Do not assume property is safe just because it is ordinary, necessary, or important to you. Bankruptcy looks at ownership, value, liens, exemptions, and which chapter you use.

4. Guessing at Home or Vehicle Values

Property values matter in both Chapter 7 and Chapter 13. If you guess too low, you may create trustee questions or property risk after filing. If you guess too high, you may talk yourself out of an option that could have worked.

Use realistic values for your home, car, truck, motorcycle, business property, tools, and other valuable items. Also check payoff balances for mortgages, car loans, and other liens.

5. Forgetting Bank Accounts, Cash, or Tax Refunds

People often focus on houses and cars, but money in bank accounts, cash on hand, and expected tax refunds can also count as assets in bankruptcy.

The balance on the filing date can matter. If you are expecting a tax refund, lawsuit recovery, inheritance, bonus, commission, or other payment, it should be reviewed before you file.

6. Leaving Out Lawsuits, Claims, or Inheritances

A lawsuit, personal injury claim, employment claim, insurance claim, inheritance, or settlement can be an asset even if you have not received any money yet. Leaving it off the bankruptcy papers can create serious problems.

Tell your bankruptcy attorney about any claim, possible claim, inheritance, probate issue, accident, employment dispute, insurance dispute, or settlement discussion before you file.

7. Transferring Property Before Filing

Selling, giving away, retitling, or transferring property before bankruptcy can create trustee issues. This includes moving vehicles, homes, land, business interests, bank funds, or valuable personal property to family members or friends.

A transfer that seems harmless outside bankruptcy may become a serious issue once a case is filed. Review transfers before you file instead of trying to fix them after the case starts.

8. Repaying Family Members Before Filing

Many people feel pressure to repay relatives or friends before filing. In bankruptcy, those payments can cause problems because trustees may treat certain insider repayments differently from ordinary creditor payments.

If you recently repaid a parent, spouse, sibling, friend, business partner, or other insider, disclose it and review the timing before you file.

9. Ignoring the Chapter 7 Means Test

Tennessee filers who are considering Chapter 7 need to review the means test. The means test uses Tennessee median income figures and other income and expense rules to help decide whether Chapter 7 is available.

Passing the means test does not automatically make Chapter 7 the right choice. Ignoring the means test, however, can lead to bad planning, delays, or a case that really should have been filed under Chapter 13 instead.

10. Assuming Bankruptcy Fixes Every Debt

Bankruptcy can discharge many unsecured debts, but not every debt is treated the same. Domestic support obligations, many recent taxes, criminal fines, restitution, some student loans, and debts based on fraud or certain wrongful conduct may survive or require special handling.

Before you file, identify which debts are likely dischargeable, which debts may survive, and which debts may need to be paid through a Chapter 13 plan.

11. Filing Without Reviewing Prior Bankruptcy Cases

If you filed bankruptcy before, the timing of that case can affect your options now. It may affect whether you can receive a discharge, how the automatic stay applies, and whether Chapter 7 or Chapter 13 is available or useful.

Prior bankruptcy cases should be reviewed before you file a new Tennessee case, especially if the earlier case was filed within the last year or ended without a discharge.

Before filing bankruptcy in Tennessee, try to avoid these common problems:

- Waiting until a foreclosure, garnishment, or repossession is at the door

- Choosing Chapter 7 without comparing Chapter 13

- Assuming Tennessee exemptions protect all property automatically

- Guessing at home, vehicle, or business property values

- Forgetting bank balances, cash, tax refunds, lawsuits, or claims

- Transferring property shortly before filing

- Repaying family members or insiders before filing

- Ignoring the Tennessee Chapter 7 means test

- Assuming every debt will be discharged

- Failing to disclose a prior bankruptcy case

Most bankruptcy mistakes are easier to prevent than to fix. Before you file in Tennessee, review your income, property, debts, exemptions, recent transfers, and timing. A careful review can help you choose the right chapter, protect the property that matters most, and avoid surprises after the case is filed.

What Happens After Filing Bankruptcy in Tennessee?

After a bankruptcy case is filed in Tennessee, the court process begins right away. The exact path depends on whether you file Chapter 7 or Chapter 13, but most cases pass through the same early stages: the automatic stay, trustee review, document requests, the 341 meeting of creditors, required debtor education, and then either a Chapter 7 discharge or a Chapter 13 plan process.

Filing the case is not the end of the story. It is the point where the court, the trustee, your creditors, and your bankruptcy paperwork all come together. What happens next depends on your chapter, your documents, your property, your debts, and whether any creditor or trustee concern needs to be resolved.

The Automatic Stay Usually Starts

In most Tennessee bankruptcy cases, filing triggers the automatic stay. The automatic stay can pause many collection actions, including collection calls, creditor lawsuits, wage garnishments, foreclosure activity, repossession efforts, and other attempts to collect debts.

The automatic stay can be limited in some repeat filing situations, so prior bankruptcy cases should be reviewed before you file. For many first-time filers, however, the stay is one of the most immediate protections bankruptcy provides.

A Trustee Is Assigned to the Case

After filing, a bankruptcy trustee is assigned. In a Chapter 7 case, the trustee reviews your assets, exemptions, income, debts, and financial history to see whether there is any nonexempt value for creditors. In a Chapter 13 case, the trustee reviews your proposed repayment plan, income, expenses, claims, and whether the plan meets bankruptcy requirements.

The trustee may request documents, ask questions, or ask you to clarify information about income, property, transfers, tax refunds, lawsuits, bank accounts, or other issues. Responding promptly and honestly helps keep the case moving.

You May Need to Provide Additional Documents

Even after filing, the trustee may ask for additional records. This is common and does not automatically mean something is wrong. The trustee may need documents to verify income, property values, exemptions, mortgage balances, vehicle payoff amounts, tax refunds, transfers, or other parts of your case.

After filing, be ready to provide documents such as:

- Recent pay stubs or other proof of income

- Bank statements that cover the filing date

- Tax returns or tax transcripts

- Mortgage statements and payoff information

- Vehicle loan payoff information

- Proof of insurance, titles, deeds, or leases

- Documents related to lawsuits, claims, settlements, or inheritances

- Information about recent transfers, sales, gifts, or family repayments

You Attend the 341 Meeting of Creditors

The 341 meeting of creditors is a required meeting where the trustee asks questions under oath about your bankruptcy papers and financial situation. It is not usually a courtroom hearing, and a judge is not typically present.

The trustee may ask about your income, expenses, property, debts, exemptions, recent transfers, tax refunds, lawsuits, and whether the information in your bankruptcy papers is accurate. Creditors can attend and ask questions, but in many consumer cases they do not.

- You must answer truthfully under oath.

- You may need identification and proof of your Social Security number.

- The trustee may ask for follow-up documents.

- Your attorney, if you have one, usually attends with you.

- The meeting is often short if your paperwork is complete and no major issues appear.

You Complete Debtor Education

After filing, most consumer filers must complete a debtor education or financial management course before receiving a discharge. This is separate from the credit counseling course that is required before filing.

If the debtor education certificate is not filed on time, the court may close the case without entering a discharge. That can be a serious problem because the case can end without the debts being wiped out.

What Happens in a Tennessee Chapter 7 Case?

In a Tennessee Chapter 7 case, the trustee reviews your paperwork, documents, exemptions, and financial history. If there are no major issues, no creditor objections, and no nonexempt assets to administer, the case may move toward a discharge after the 341 meeting and the required deadlines.

A Chapter 7 discharge generally wipes out qualifying unsecured debts such as credit cards, medical bills, personal loans, and many collection accounts. Some debts may survive bankruptcy, and secured debts such as mortgages and car loans still require attention if you want to keep the property that secures the loan.

After filing Chapter 7 in Tennessee, watch for:

- Trustee document requests

- The 341 meeting date and instructions

- Deadlines for creditor or trustee objections

- Reaffirmation, redemption, or surrender decisions for secured debts

- Questions about Tennessee exemptions or nonexempt property

- The debtor education certificate deadline

- The discharge order

What Happens in a Tennessee Chapter 13 Case?

In a Tennessee Chapter 13 case, filing is the start of a longer plan process. You propose a repayment plan, begin making plan payments, attend the 341 meeting, and work toward plan confirmation. If the plan is confirmed, you continue making payments for the required plan period.

Chapter 13 can help you catch up on mortgage arrears, deal with car loans, pay certain tax debts, handle support arrears, and address property that may not be fully protected by Tennessee exemptions. The plan must still be feasible, which means it has to fit your actual income and expenses.

After filing Chapter 13 in Tennessee, watch for:

- Starting plan payments on time

- Staying current on any ongoing mortgage or car payments if required

- Trustee objections or requests for plan changes

- Creditor claims that are filed in the case

- The plan confirmation process and any hearings

- Tax return and refund requirements during the case

- Budget changes that could affect whether the plan remains feasible

The Case Moves Toward Discharge or Plan Completion

In Chapter 7, the goal is usually to receive a discharge after trustee review, the 341 meeting, required deadlines, and debtor education are complete. In Chapter 13, the goal is to complete the court approved repayment plan and then receive a discharge at the end of the plan.

The discharge is the court order that eliminates personal liability for qualifying debts. It is one of the main reasons people file bankruptcy, but it only applies to debts that are legally dischargeable and properly handled inside the case.

After filing bankruptcy in Tennessee, your main job is to:

- Read court and trustee notices carefully

- Provide requested documents quickly

- Attend the 341 meeting

- Complete debtor education

- Stay current on required payments

- Tell your attorney about income, address, property, or debt changes

- Follow chapter-specific deadlines until discharge or plan completion

The main point is that filing bankruptcy starts the court process, but the case still has to move through trustee review, required meetings, deadlines, and chapter-specific requirements. A clean Tennessee bankruptcy case depends on accurate paperwork, timely documents, honest answers, and a clear understanding of what needs to happen after you file.

Debts That Can and Cannot Be Discharged in Tennessee

Bankruptcy discharge rules come from federal law, so Tennessee does not have its own separate list of which debts can or cannot be wiped out. Even so, the facts of a Tennessee case still matter. The chapter you file, the type of debt, whether the debt is secured, whether a lawsuit or judgment exists, and whether a creditor objects can all affect the result.

A bankruptcy discharge generally eliminates your personal liability for qualifying debts. That means the creditor can no longer collect the discharged debt from you personally. Not every debt is discharged, however, and liens on property can sometimes survive even when personal liability is discharged.

Debts Commonly Discharged in Tennessee Bankruptcy

Many Tennessee filers use bankruptcy to deal with unsecured debts. These are debts that are not tied to collateral like a house or a car.

| Debt Type | Common Bankruptcy Treatment | What to Watch For |

|---|---|---|

| Credit cards | Often dischargeable in Chapter 7 or Chapter 13. | Recent charges, cash advances, luxury purchases, or fraud allegations can create issues. |

| Medical bills | Usually treated as general unsecured debt and often dischargeable. | List all providers, hospitals, collection agencies, and medical debt buyers. |

| Personal loans | Often dischargeable if they are not tied to collateral and do not involve fraud. | Co-signers may remain liable if they do not file bankruptcy. |

| Old utility bills | Often dischargeable if they are prebankruptcy debts. | Utility companies may still require an adequate assurance deposit for future service after filing. |

| Collection accounts | Often dischargeable if they are based on dischargeable unsecured debt. | List the original creditor, any collection agency, and any debt buyer if you can. |

| Deficiency balances | Often dischargeable after repossession, foreclosure, or surrender. | Confirm whether the creditor has a remaining balance after selling the collateral. |

Debts That Usually Are Not Discharged

Some debts usually survive bankruptcy or need special treatment. These rules come from federal bankruptcy law, including the exceptions to discharge in11 U.S.C. § 523.

| Debt Type | Typical Treatment | What to Watch For |

|---|---|---|

| Child support and alimony | Usually not discharged. | Domestic support obligations generally continue and may need to be paid through a Chapter 13 plan if you are behind. |

| Recent or priority tax debts | Often not discharged, although some older income taxes may qualify. | Tax year, filing date, assessment date, whether returns were filed, and the type of tax all matter. |

| Most student loans | Usually not discharged unless the borrower proves undue hardship. | Student loan discharge typically requires an additional lawsuit inside bankruptcy called an adversary proceeding. |

| Criminal fines and restitution | Usually not discharged. | Bankruptcy generally does not erase criminal punishment or restitution obligations. |

| Debts from fraud or false pretenses | May be nondischargeable if a creditor objects and proves the required elements. | A creditor may need to file an adversary proceeding by the applicable deadline. |

| Willful and malicious injury debts | May be nondischargeable, especially in Chapter 7. | The result can depend on the chapter, the judgment, and the specific facts. |

| Certain debts not listed in the case | May survive if the creditor was not properly listed or notified. | List every creditor, collection agency, lawsuit creditor, and debt buyer with a correct address. |

Secured Debts Need Separate Attention

Mortgages, car loans, furniture loans, title loans, and similar secured debts are different from ordinary unsecured debts because they are tied to collateral. Bankruptcy may discharge personal liability on a secured debt, but the lien can still matter if you want to keep the property.

- If you want to keep a house, you usually need to stay current or use Chapter 13 to catch up on mortgage arrears.

- If you want to keep a vehicle, you usually need to stay current, reaffirm, redeem, or use Chapter 13 depending on the facts.

- If you surrender collateral, any remaining deficiency balance may be dischargeable as long as it is not based on fraud or another exception.

- If a lien survives bankruptcy, the creditor may still have rights against the property even if personal liability is discharged.

Chapter 7 and Chapter 13 Can Treat Some Debts Differently

The discharge is not exactly the same in Chapter 7 and Chapter 13. Chapter 13 can sometimes provide a broader discharge for certain debts, but it also requires that you complete a repayment plan before the discharge is entered. Some debts may still remain owed after a Chapter 13 case if they are not fully paid through the plan or if they fall into an exception.

Before assuming a debt will be discharged, check:

- Is the debt secured or unsecured?

- Does it involve support, taxes, student loans, fraud, injury, or criminal related?

- Is there a lawsuit, judgment, or pending court date?

- Was the creditor listed correctly in the bankruptcy papers?

- Has the creditor filed or threatened an objection?

- Would Chapter 7 or Chapter 13 handle the debt more effectively?

The main idea is that Tennessee bankruptcy can discharge many ordinary unsecured debts, but it does not erase every obligation. Before you file, sort your debts into broad groups: debts that are likely to be discharged, debts that may survive, secured debts that are tied to property, and debts that may need special treatment in a Chapter 13 plan.

Tennessee Bankruptcy Trends

Bankruptcy filing trends can help show how financial stress is changing, but they should not determine whether you personally should file. A Tennessee bankruptcy decision still depends on your income, debts, property, exemptions, lawsuits, garnishments, foreclosure risk, repossession risk, and your chapter options.

Nationally, bankruptcy filings have been rising from the unusually low levels seen after 2020. The Administrative Office of the U.S. Courts reported that total bankruptcy filings rose about 11 percent for the 12 month period ending December 31, 2025, with both business and nonbusiness filings increasing. Even with that increase, national filings remained far below the historical highs seen after the Great Recession.

Tennessee bankruptcy filings are best reviewed by federal judicial district: the Eastern District of Tennessee, the Middle District of Tennessee, and the Western District of Tennessee. The U.S. Courts publishes quarterly bankruptcy filing statistics, including district level data and county level bankruptcy tables.

When reviewing Tennessee bankruptcy trends, watch for:

- Whether consumer bankruptcy filings are rising or falling statewide

- Differences between Eastern, Middle, and Western Tennessee filings

- Whether Chapter 7 or Chapter 13 filings are increasing faster

- Local signs of stress, such as garnishments, foreclosure activity, repossessions, and collection lawsuits

- Whether rising filings reflect broader economic pressure or a delayed return to more typical filing levels

Source: U.S. Courts bankruptcy filing statistics. The U.S. Courts publishes quarterly bankruptcy data tables for 12 month periods ending March 31, June 30, September 30, and December 31.

The practical takeaway is that trends can provide helpful context, but they do not answer the personal question. If you are facing a Tennessee lawsuit, garnishment, foreclosure, repossession, or unmanageable debt, the more useful question is whether Chapter 7, Chapter 13, or a nonbankruptcy option gives you the safest path forward.

What This Means for You

Bankruptcy in Tennessee is not just a question of whether you have too much debt. The better question is what problem you need to solve and which path gives you the safest way forward. Chapter 7 and Chapter 13 can both help, but they solve different kinds of problems.

If your main issue is credit cards, medical bills, personal loans, collection accounts, or wage garnishment, Chapter 7 may be worth reviewing if your income fits the Tennessee means test and your property appears protected by Tennessee exemptions. If you are behind on a mortgage or car loan, facing foreclosure or repossession, dealing with taxes or support arrears, or trying to protect property that may not be fully exempt, Chapter 13 may deserve a closer look.

Before deciding whether to file bankruptcy in Tennessee, ask:

- What debt or collection problem is creating the most pressure?

- Is there an urgent lawsuit, garnishment, foreclosure, or repossession issue?

- Would Chapter 7 actually solve the problem, or do you need Chapter 13?

- Does your household income fit the Tennessee Chapter 7 means test?

- Do Tennessee exemptions appear to protect your home, car, bank accounts, and other property?

- Are you current or behind on secured debts such as a mortgage or vehicle loan?

- Have you recently transferred property, sold assets, or repaid family members?

- Which Tennessee bankruptcy district would handle your case?

The most useful next step is to organize the facts that matter: your income, household size, debts, property values, loan balances, payment arrears, lawsuits, garnishments, tax issues, and recent financial transactions. Those details usually determine whether Chapter 7, Chapter 13, or a non bankruptcy option makes the most sense.

Use this Tennessee bankruptcy guide as a starting point. Then review the Tennessee-specific pages for the issues that matter most to you, including Chapter 7, Chapter 13, exemptions, keeping a house, keeping a car, and stopping collections. The goal is not just to file a case. The goal is to understand your options, avoid preventable mistakes, and choose a path that actually helps you move forward.

Tennessee Bankruptcy FAQs

These Tennessee bankruptcy FAQs cover common questions about Chapter 7, Chapter 13, exemptions, costs, court locations, property, and what happens after you file. The exact answer in your situation still depends on your income, debts, property, exemptions, filing history, and which Tennessee bankruptcy district handles your case.

What is the difference between Chapter 7 and Chapter 13 bankruptcy in Tennessee?

Chapter 7 is usually the faster chapter and is often used when the main problem is unsecured debt such as credit cards, medical bills, personal loans, and collection accounts. Chapter 13 is a repayment plan case that usually lasts three to five years and may help if you need time to catch up on a mortgage, car loan, taxes, support arrears, or other debts.

The better choice depends on what you need bankruptcy to do. If unsecured debt is the main issue and your property is protected, Chapter 7 may be worth reviewing. If you are behind on a house or car, facing foreclosure or repossession, or trying to protect property that may not be fully exempt, Chapter 13 may be the better fit.

Can I file Chapter 7 bankruptcy in Tennessee?

You may be able to file Chapter 7 in Tennessee if you meet the eligibility rules, pass or otherwise satisfy the Chapter 7 means test, and Chapter 7 fits your situation. The means test uses Tennessee median income figures for your household size and may then review allowed expenses if your income is above median.

Passing the means test does not automatically mean Chapter 7 is the right choice. You still need to review Tennessee exemptions, property values, recent transfers, lawsuits, tax refunds, secured debts, and whether Chapter 7 solves the problem you are trying to fix.

What is the Tennessee Chapter 7 means test?

The Chapter 7 means test is a federal formula that uses Tennessee-specific median income figures. It generally looks at your household income during the six months before filing, annualizes that income, and compares it to the Tennessee median income for a household of your size.

If your income is below the applicable Tennessee median income, Chapter 7 may be easier to evaluate. If your income is above median, the test continues by subtracting allowed expenses to see whether there may be enough disposable income to repay creditors through Chapter 13.

Does Tennessee use state or federal bankruptcy exemptions?

Usually not. Tennessee has opted out of the federal § 522(d) exemption set, so debtors entitled to use Tennessee law generally must use Tennessee exemptions. However, federal domicile rules may point to another state’s law, and the federal exemption set may become available in the unusual situation where those rules leave the debtor ineligible for any exemptions.

Can I keep my house if I file bankruptcy in Tennessee?

Many Tennessee filers keep their homes, but the answer depends on home equity, mortgage status, Tennessee exemptions, and whether Chapter 7 or Chapter 13 is the better fit. If your equity is protected and you are current on the mortgage, Chapter 7 may be easier to evaluate.

If you are behind on mortgage payments and want to keep the home, Chapter 13 may be more useful because it may let you catch up on mortgage arrears through a repayment plan while you resume regular mortgage payments.

Can I keep my car if I file bankruptcy in Tennessee?

Many Tennessee filers keep their vehicles, but the answer depends on vehicle value, loan payoff, equity, payment status, exemptions, and chapter choice. If the vehicle equity is protected and you are current on the loan, Chapter 7 may be worth reviewing.

If you are behind on the car loan or facing repossession, Chapter 13 may provide more structure. If filed in time, Chapter 13 may stop repossession and allow missed payments or vehicle debt treatment to be handled through the plan.

Will bankruptcy stop wage garnishment in Tennessee?

Filing bankruptcy usually triggers the automatic stay, which can stop many wage garnishments for dischargeable debts. Once the case is filed, the creditor, the court, and your payroll department may need notice before the garnishment actually stops.

Garnishments for domestic support obligations and some other debts may be treated differently. The type of debt matters.

Will bankruptcy stop foreclosure in Tennessee?

Bankruptcy may stop or pause foreclosure if the case is filed before the sale is completed. Chapter 7 may create a temporary pause, but it usually does not give you a long-term way to catch up on missed mortgage payments.