Colorado Bankruptcy

If you’re thinking about filing bankruptcy in Colorado, you’re not alone—and you’re not the first person to feel overwhelmed by the process. Colorado bankruptcy can feel intimidating, but understanding how the system works is the first step toward getting your life back.

Colorado Bankruptcy — At a Glance

- How Colorado and Federal Law Work Together: The federal Bankruptcy Code (Title 11) sets the structure of your case, while Colorado bankruptcy laws and exemptions in the Colorado Revised Statutes decide what property you can keep when you file.

- Where You File: All personal and business cases are filed with the United States Bankruptcy Court for the District of Colorado in Denver, which applies federal law, the Federal Rules of Bankruptcy Procedure, and local Colorado rules.

- Main Colorado Bankruptcy Options: Most individuals filing bankruptcy in Colorado use chapter 7 (faster discharge of qualifying unsecured debt) or chapter 13 (3–5 year repayment plan), with chapter 11 and chapter 12 reserved for businesses, high-debt individuals, and family farmers.

- Eligibility and the Means Test: Chapter 7 eligibility depends heavily on the federal means test and Colorado median income figures, while chapter 13 requires regular income and staying within the debt limits of 11 U.S.C. § 109(e).

- How Much It Costs to File Bankruptcy in Colorado: Court filing fees are currently about $338 for chapter 7 and $313 for chapter 13, plus modest costs for required courses and credit reports. Attorney fees are usually the largest component, with payment plans and, in some cases, fee waivers or installments available.

- Big-Picture Filing Steps: Evaluate your situation, complete pre-filing credit counseling, work with a Colorado bankruptcy attorney, file your petition and schedules, obtain the automatic stay, attend your 341 meeting of creditors, complete debtor education, and receive a discharge.

- Documents and Timeline: Expect to provide tax returns, pay stubs, bank statements, and a full asset/debt list. A typical Colorado chapter 7 case takes about 3–6 months; chapter 13 cases usually run 3–5 years under a court-approved repayment plan.

- Trustee and 341 Meeting: A court-appointed trustee reviews your paperwork, runs the 341 meeting (often by Zoom), and administers any non-protected assets or chapter 13 plan payments—most people never appear in front of a judge.

- What Happens to Your House, Car, and Other Property: Federal rules and Colorado exemptions work together so that most filers keep the property they need to live and work; chapter 7 focuses on non-protected assets, while chapter 13 uses a payment plan instead of liquidation.

- Automatic Stay Protection: Filing bankruptcy in Colorado triggers the automatic stay under 11 U.S.C. § 362, which usually stops most collection calls, garnishments, repossessions, and foreclosure efforts while your case is active.

- Required Courses and Official Resources: Pre-filing credit counseling and post-filing debtor education must come from U.S. Trustee–approved providers, with official lists available through the U.S. Trustee Program website for Colorado.

- Alternatives and FAQs: Non-bankruptcy options like nonprofit debt-management plans and negotiated settlements may help some people, but many still choose Colorado bankruptcy for its predictable legal protection, clear endpoint, and structured fresh start.

Colorado bankruptcy laws work alongside federal law, but they aren’t identical. Colorado has its own rules about what property you can keep, what creditors can take, and how your case moves through the system. Knowing how Colorado bankruptcy laws fit together with federal rules helps you make informed, confident decisions instead of guessing.

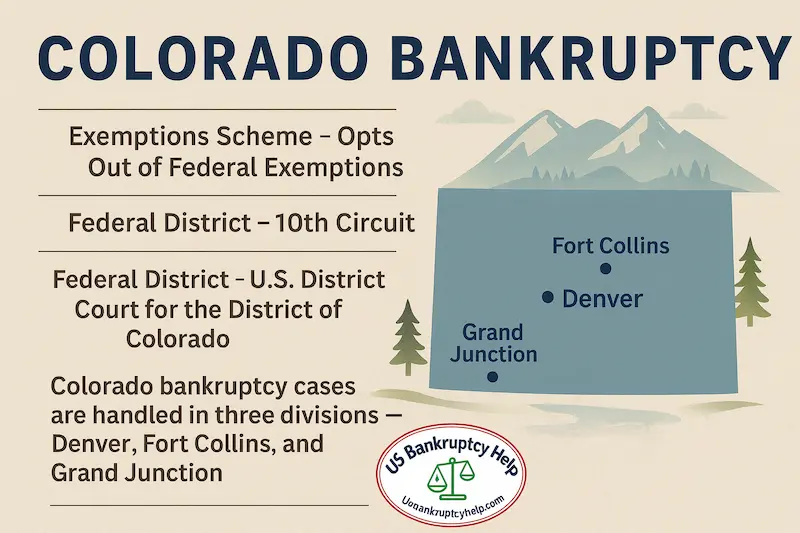

All personal and business bankruptcy cases are handled by the United States Bankruptcy Court District of Colorado. This is the court where you file your paperwork, attend hearings, and move your case forward. Understanding the role of the United States Bankruptcy Court District of Colorado is a key part of answering a common question: How do you file for bankruptcy in Colorado?

Most people considering bankruptcy Colorado are looking at chapter 7 or chapter 13. Each chapter has its own eligibility rules, timelines, and pros and cons. Choosing the right chapter—chapter 7, chapter 13, or another option—can make a major difference in how quickly you recover and what happens to your property.

A common concern is cost: How much does it cost to file bankruptcy in Colorado? The total cost of filing bankruptcy in Colorado includes court filing fees and, in many cases, attorney fees. Knowing these numbers upfront helps you plan, budget, and avoid surprises.

Bankruptcy will affect your credit score and your short-term financial picture, but for many people, it’s also the tool that finally stops the bleeding. Weighing the pros and cons honestly is crucial before you move forward.

In some situations, alternatives to bankruptcy—like debt settlement, negotiation, or consolidation—may be available. Exploring these options alongside Colorado bankruptcy gives you a fuller picture of your choices.

This guide walks you through the realities of bankruptcy in Colorado from start to finish: how the process works, what it costs, what happens to your property, and what life can look like on the other side. Understanding your options is the first step toward a real fresh start.

Understanding Colorado Bankruptcy Law

Bankruptcy in the United States is rooted in federal law—specifically Title 11 of the U.S. Code, commonly called the Bankruptcy Code. Congress created this system to give financially stressed individuals and businesses a structured, lawful way to eliminate or reorganize debt. Every Colorado bankruptcy case, whether chapter 7 or chapter 13, is governed first by this federal framework.

But federal law doesn’t answer every question. Under 11 U.S.C. § 522(b), states have the right to create their own exemption systems—the rules that determine what property you can protect when filing bankruptcy. Colorado has chosen to “opt out” of the federal exemption scheme, which means residents must use Colorado exemptions set by state law.

These Colorado-specific protections come from the Colorado Revised Statutes (C.R.S.), including:

- C.R.S. § 38-41-201 — Colorado’s homestead exemption, protecting equity in a primary residence.

- C.R.S. § 13-54-102 — Personal property exemptions (vehicles, household goods, tools of the trade, and more).

- C.R.S. § 13-54-104 — Limits on wage garnishment.

These statutes illustrate how Colorado bankruptcy laws interact with federal rules. The Bankruptcy Code controlshow the process works—filing requirements, trustee duties, discharge rules—while Colorado law determineswhat property you get to keep. For example, if you're filing bankruptcy in Colorado and you own a home, the Colorado homestead exemption decides how much of your equity is protected from creditors.

Choosing the right type of bankruptcy is another critical decision. The most common options include:

- Chapter 7: A liquidation-based process under 11 U.S.C. Chapter 7, where a trustee may sell non-exempt assets and qualifying debts are discharged.

- Chapter 13: A repayment plan under 11 U.S.C. Chapter 13, allowing individuals with regular income to reorganize debt over three to five years.

- Chapter 11: A reorganization chapter—usually for businesses—under 11 U.S.C. Chapter 11.

Eligibility depends on your income, assets, debts, and overall financial picture. Tools like the federal “means test” and Colorado’s exemption statutes play a major role. Speaking with an experienced Colorado bankruptcy attorney can help you understand how both sets of laws apply to your unique situation and guide you toward the chapter that aligns with your goals.

The United States Bankruptcy Court District of Colorado

Every Colorado bankruptcy case—whether Chapter 7, Chapter 13, or Chapter 11—is administered through theUnited States Bankruptcy Court for the District of Colorado. This court is part of the federal judiciary created under 28 U.S.C. § 151, which establishes bankruptcy courts as units of the U.S. District Courts. When people talk about “filing bankruptcy in Colorado,” this is the court where it all happens.

Although the Bankruptcy Code is federal law, the Colorado bankruptcy court applies a combination offederal statutes, Federal Rules of Bankruptcy Procedure, andLocal Bankruptcy Rules for the District of Colorado. This blend of national standards and Colorado-specific rules gives cases structure while ensuring they move efficiently through the system.

Individuals and businesses file their petitions electronically through the court’s CM/ECF system, and from that moment forward, the Colorado bankruptcy court oversees every stage of the process—reviewing filings, issuing orders, setting deadlines, and ensuring compliance with both federal law and Colorado bankruptcy laws (such as state exemptions under C.R.S.).

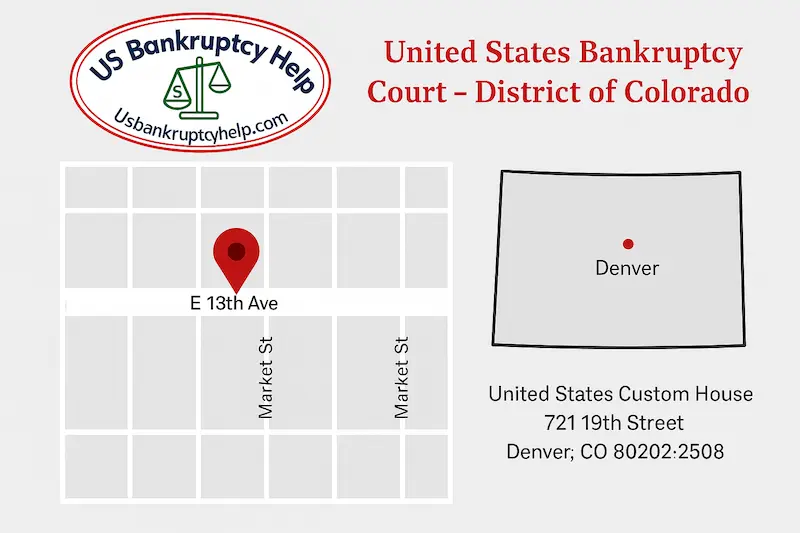

The main Colorado bankruptcy courthouse is located in downtown Denver at the U.S. Custom House. Here is the primary contact information for the United States Bankruptcy Court District of Colorado:

| Location | Street Address | Phone | Website |

|---|---|---|---|

| Denver (Main Office) | United States Bankruptcy Court U.S. Custom House 721 19th Street Denver, CO 80202 | 720-904-7300 | www.cob.uscourts.gov |

Key functions of the United States Bankruptcy Court District of Colorado include:

- Reviewing bankruptcy petitions, schedules, and financial disclosures to ensure accuracy and completeness under 11 U.S.C. requirements.

- Conducting the 341 meeting of creditors (required under 11 U.S.C. § 341), where debtors must answer questions under oath about their finances.

- Overseeing trustee appointments and ensuring trustees fulfill their duties—including asset review, exemption evaluation, and distribution of funds when required.

- Enforcing debtor education requirements so filers complete both pre-filing credit counseling and post-filing financial management courses.

- Issuing orders and discharges that formally wipe out qualified debts once all legal requirements are met.

Understanding how the United States Bankruptcy Court District of Colorado functions—its procedures, rules, and standards—helps filers navigate the process confidently. Whether you’re evaluating exemptions, preparing schedules, or working through a repayment plan, this court is the central hub where your Colorado bankruptcy case is managed and ultimately resolved.

Colorado Bankruptcy Laws: State vs. Federal Rules

When people ask about Colorado bankruptcy laws, what they’re really asking is how Colorado’s rules fit together with the federal Bankruptcy Code. Federal law in Title 11 of the U.S. Codecontrols the structure of your case—what chapters are available, how the discharge works, what the trustee does, and the basic procedures for filing bankruptcy in Colorado.

Colorado law, by contrast, has the most impact on what happens to your property. Because Colorado has opted out of the federal exemption scheme under 11 U.S.C. § 522(b), most filers must use exemptions found in theColorado Revised Statutes (C.R.S.). Those exemptions decide how much equity you can protect in your home, vehicle, household goods, and other assets when you file.

In practice, that means federal law sets the playing field, and Colorado law sets many of the rules about what you can keep. For example, if you own a home with equity in Denver and a paid-off car:

- Federal law determines which chapter you file under (chapter 7 vs. chapter 13), what the trustee’s duties are, and how the discharge is entered.

- Colorado law determines how much of your home equity is protected by the homestead exemption and how much vehicle equity you can shield from creditors.

Because both systems are working at the same time, understanding this state–federal balance is crucial before filing bankruptcy in Colorado. A knowledgeable Colorado bankruptcy attorney can help you apply the federal rules and Colorado exemptions in a way that maximizes protection and avoids unpleasant surprises.

Types of Bankruptcy in Colorado: Chapter 7, Chapter 13, and More

When people talk about Colorado bankruptcy, they are usually choosing between a few main “chapters” of the Bankruptcy Code. The right chapter depends on your income, assets, and goals—whether you need a faster fresh start, time to catch up on payments, or a way to reorganize a struggling business.

For most individuals filing bankruptcy in Colorado, the two most common options are chapter 7 and chapter 13. At a high level:

- Chapter 7 – A faster process where a trustee reviews your assets, sells any non-exempt property if necessary, and wipes out qualifying unsecured debts. It’s generally best suited for people with limited income and significant unsecured debt.

- Chapter 13 – A three- to five-year repayment plan that lets you catch up on arrears (like a mortgage or car loan) while protecting your property, as long as you can afford the required monthly plan payment.

- Chapter 11 – A reorganization chapter most often used by businesses or individuals with complex or higher-debt cases. For a deeper dive, see the national chapter 11 guide.

- Chapter 12 – A specialized chapter designed for family farmers and family fishermen.

The chapter you choose also interacts with Colorado bankruptcy exemptions, which determine what property you can protect. For detailed Colorado-specific rules, examples, and strategy, it’s usually best to review the dedicated chapter 7 guide, chapter 13 guide, and Colorado exemptions page.

Used together, these pages form the core of your Colorado bankruptcy roadmap: this overview page explains the big picture, while the chapter-specific and exemption pages—and your national chapter 11 resource page—walk through the details for each path.

Who Is Eligible for Bankruptcy in Colorado?

Not everyone who is struggling with debt will qualify for every type of Colorado bankruptcy. Eligibility depends on your income, the type and amount of your debt, your recent financial history, and even whether you have filed bankruptcy before. Understanding these rules up front can save time, stress, and missteps when you are thinking about filing bankruptcy in Colorado.

For most individuals, the first major hurdle is whether you qualify for chapter 7. Under the “means test” in 11 U.S.C. § 707(b), your household income is compared to the Colorado median income for a household of your size. If your income is below the applicable Colorado median, you generally pass the first part of the means test and may qualify for chapter 7, subject to other requirements. If your income is above the median, a more detailed calculation of allowed expenses and disposable income is required before a chapter 7 case can move forward.

Chapter 13 eligibility works differently. To file under chapter 13, you need:

- A regular source of income sufficient to support a repayment plan.

- Debt levels within the limits set by 11 U.S.C. § 109(e) for secured and unsecured debts.

In addition to income and debt limits, there are other eligibility rules that apply no matter which chapter you choose. You must complete an approved credit counseling course before filing, you cannot have had certain recent bankruptcy discharges, and you must meet basic honesty and documentation requirements—accurate schedules, full disclosure of assets and debts, and no recent intentional fraud.

Essential eligibility criteria for most Colorado bankruptcy cases include:

- Passing the chapter 7 means test or showing that your disposable income is insufficient to repay creditors.

- Having regular income and staying within the chapter 13 debt limits if you propose a repayment plan.

- Completing required credit counseling before filing and debtor education before receiving a discharge.

- Providing truthful, complete financial information and meeting prior-filing and waiting-period rules.

Because these rules combine federal law with Colorado-specific median income figures and practical court expectations, eligibility is rarely as simple as “do I make too much?” A knowledgeable Colorado bankruptcy attorney can walk through your income, debts, assets, and goals to help you determine whether chapter 7, chapter 13, or another path is realistically available—and whether filing bankruptcy in Colorado is truly the right next step for you.

How Much Does It Cost to File Bankruptcy in Colorado?

One of the first practical questions people ask is, “How much does it cost to file bankruptcy in Colorado?” The total cost of a Colorado bankruptcy has several parts: the federal court filing fee, required credit counseling and debtor education courses, the cost of pulling credit reports and documents, and, if you hire one, your attorney’s fee. Knowing these pieces up front makes it easier to decide whether filing bankruptcy in Colorado is realistic for your budget.

The court filing fee for a personal chapter 7 case is currently $338 nationwide, and for a chapter 13 case it is $313. These amounts are set at the federal level (under 28 U.S.C. § 1930) and are the same in the United States Bankruptcy Court for the District of Colorado as they are in every other bankruptcy court in the country. The total includes the basic filing fee, an administrative fee, and, for chapter 7, a small trustee surcharge. Because these numbers can change occasionally, it’s always smart to confirm the current amount on the official U.S. Courts website or directly with the Colorado bankruptcy court clerk before you file.

In addition to the filing fee, you must complete a pre-filing credit counseling course and apost-filing debtor education course from approved providers. Each course typically costs between about $10 and $50, and some providers offer reduced fees or waivers based on income. Many filers also pay a modest amount for a tri-merge credit report or similar service to make sure all creditors are captured accurately in their Colorado bankruptcy paperwork.

For most people, the largest part of the overall cost of bankruptcy Colorado is the attorney fee. Nationally, straightforward consumer chapter 7 cases often fall in a general range of roughly $1,500 to $2,500 or more, while chapter 13 attorney fees are typically higher, frequently in the $2,500 to $5,000+ range depending on complexity. Where your case lands in that range depends heavily on factors like how many creditors you have, whether the means test is simple or close, whether any exemptions are tight, and whether there are business interests, tax issues, or other complications that will require additional attorney time.

Beyond these major components, there can be smaller additional costs, such as fees for property appraisals, obtaining tax transcripts, or gathering certain financial records. These usually add up to a relatively modest amount but are still worth budgeting for when you are planning a Colorado bankruptcy filing.

Here’s a quick breakdown of common costs when filing bankruptcy in Colorado:

- Court filing fee: about $338 for chapter 7 and $313 for chapter 13 (same nationwide).

- Credit counseling and debtor education: usually around $10–$50 per course, sometimes reduced or waived based on income.

- Credit reports and document-gathering costs: typically a modest additional amount.

- Attorney fees: often the largest component, with chapter 7 consumer cases commonly in the low-thousands range and chapter 13 cases higher due to the length and complexity of the repayment plan.

If you truly cannot afford the filing fee all at once, the court may allow you to pay the fee in installments, and in some low-income chapter 7 cases the filing fee can be partially or fully waived if you meet the federal poverty and hardship standards. Many Colorado bankruptcy attorneys also offer payment plans for their own fees, especially in chapter 13, where part of the fee can often be built into the repayment plan itself.

Budgeting for these costs in advance—and asking specific questions about fees and payment options during your consultation—can make filing bankruptcy in Colorado much more manageable and predictable, rather than one more financial surprise.

Step-by-Step Guide to Filing Bankruptcy in Colorado

When people ask, “How do you file for bankruptcy in Colorado?” it’s easy to imagine a simple set of forms and a quick trip to the courthouse. In reality, a Colorado bankruptcy is a detailed legal process that involves federal statutes, Colorado exemption laws, strict deadlines, and mandatory disclosures. For most people, this is not a true DIY project.

While this overview can help you understand the basic steps, it is not a substitute for legal advice. A knowledgeable Colorado bankruptcy attorney can explain how the law applies to your specific situation, help you avoid costly mistakes, and guide you from the first consultation through discharge.

Before You File: Assessing Your Situation

The process of filing bankruptcy in Colorado generally unfolds in stages. First, assess your overall financial situation. Take an honest inventory of your debts, income, assets, and recent financial history. This is where a Colorado bankruptcy attorney can begin to help you understand whether bankruptcy makes sense at all, and if so, whether chapter 7 or chapter 13 is more realistic for your goals.

Next, meet with a qualified Colorado bankruptcy lawyer. An attorney can evaluate how the means test applies to you, how Colorado exemptions may protect your property, and whether there are any red flags (like recent transfers, lawsuits, or tax issues) that need to be addressed before filing. Trying to navigate these issues alone can lead to case dismissal, loss of assets, or even allegations of fraud if things are not disclosed correctly.

Preparing Your Colorado Bankruptcy Case

Once you’ve decided to move forward, you’ll need to gather the required documents: recent pay stubs, tax returns, bank statements, information about all debts and creditors, leases, titles, and any lawsuits or garnishments. Accurate, complete documentation is crucial in a Colorado bankruptcy case; your attorney will typically give you a detailed checklist and help you understand what is needed.

Before filing, you must complete a pre-filing credit counseling course from an approved provider. This is mandatory under federal law and must be done within a specific timeframe before your case is filed. Your attorney can help you choose a provider and make sure the certificate is properly filed with the court.

Filing With the Colorado Bankruptcy Court

After these steps, your attorney will prepare and file the bankruptcy petition, schedules, and related documents with theUnited States Bankruptcy Court for the District of Colorado. This filing officially starts your case and triggers the automatic stay, which generally stops most collection actions, garnishments, and lawsuits while the case is pending.

Once the case is filed, you will be scheduled for a 341 meeting of creditors. At this meeting, the bankruptcy trustee will ask you questions under oath about your finances, assets, and paperwork. A Colorado bankruptcy lawyer will prepare you for this meeting, attend with you, and help address any trustee concerns that arise.

Throughout the case, there may be additional steps—responding to trustee requests, amending schedules, providing updated documents, or addressing creditor objections. Having an experienced attorney guiding you through each phase can make the difference between a smooth path to discharge and a stressful, error-filled process.

Key Steps to Follow:

- Assess your overall financial situation and goals.

- Consult with an experienced Colorado bankruptcy attorney before filing anything on your own.

- Gather required documents (income, debts, assets, tax returns, bank statements).

- Complete an approved pre-filing credit counseling session.

Filing Process:

- File your petition and schedules with the United States Bankruptcy Court for the District of Colorado (usually through your attorney).

- Receive automatic stay protection that temporarily stops most collection activity.

- Attend your 341 meeting of creditors, with your Colorado bankruptcy lawyer by your side.

This step-by-step outline is meant to orient you, not to replace professional advice. Because every case is different, speaking directly with a Colorado bankruptcy attorney is the safest way to make sure you are filing in the right chapter, protecting as much property as possible, and moving toward the fresh start the law is designed to provide.

Required Documents and the Bankruptcy Timeline

No matter which chapter you file under, a Colorado bankruptcy case rises or falls on the quality of your paperwork. The trustee, the United States Bankruptcy Court for the District of Colorado, and your creditors all rely on the documents you provide to understand your income, assets, and debts. Having the right records organized before you file can make the process smoother, faster, and far less stressful.

In most Colorado bankruptcy cases, you will be expected to provide several months of income information, recent tax returns, bank statements, and a complete list of what you own and what you owe. Your Colorado bankruptcy attorney will typically give you a detailed checklist and help you gather and organize these documents so they match what the trustee and court expect to see.

Essential Documents to Prepare

Exact requirements can vary slightly by chapter and by trustee, but most people filing bankruptcy in Colorado should be ready to gather at least the following:

- Recent federal and state tax returns (often the last 2 years, sometimes more for complex cases).

- Pay stubs or other proof of income for the last 6 months (including wages, self-employment, pensions, or benefits).

- Bank statements for all accounts for several months leading up to filing.

- A complete list of debts, including credit cards, medical bills, personal loans, taxes, judgments, and collection accounts.

- Asset documentation: vehicle titles, property deeds, retirement account statements, life insurance policies, and documentation for any business interests.

- Information about leases, car loans, mortgages, and any co-signers or guarantors.

- Copies of lawsuits, garnishment orders, foreclosure notices, and other court papers, if any.

- Proof of identity and Social Security number (used for your 341 meeting and trustee verification).

Providing accurate, complete documents not only helps your attorney advise you correctly, it also builds trust with the trustee and reduces the chances of delays, objections, or requests for additional information after you file.

Typical Colorado Bankruptcy Timeline

The overall bankruptcy timeline in Colorado depends on the chapter you file and how complicated your case is, but there are some common benchmarks. For a straightforward chapter 7 case, it often takes about three to six monthsfrom the date of filing until discharge. Chapter 13 cases last much longer—typically three to five years— because you are completing a court-approved repayment plan.

In a typical Colorado chapter 7 case, the timeline often looks something like this:

- Pre-filing: Several weeks of document gathering, credit counseling, and attorney preparation.

- Filing day: Your petition is filed, and the automatic stay goes into effect.

- About 4–6 weeks after filing: You attend your 341 meeting of creditors with your attorney.

- Roughly 60 days after the 341 meeting: Deadlines pass for most objections to discharge.

- Within about 3–6 months of filing: If all requirements are met, the court enters your discharge.

For chapter 13, the early steps are similar—preparation, filing, the automatic stay, and a 341 meeting—but the case continues while you make monthly plan payments over three to five years, with a confirmation hearing to approve your repayment plan and ongoing court oversight.

A Colorado bankruptcy attorney can walk you through how these general timelines apply to your specific situation, taking into account trustee practices, local rules, and any unique issues in your case. Knowing what documents you’ll need and how long the process is likely to take can make filing bankruptcy in Colorado feel much more predictable and manageable.

The Role of the Bankruptcy Trustee and the 341 Meeting

When you file for bankruptcy in Colorado, you don’t deal directly with the judge in most of the day-to-day process. Instead, a court-appointed bankruptcy trustee oversees your case. The trustee’s job is to review your paperwork, verify your financial information, and make sure the process is fair to both you and your creditors under the Bankruptcy Code.

Every individual bankruptcy case also includes a brief but mandatory hearing called the 341 meeting of creditors, named after 11 U.S.C. § 341. This meeting is usually your only live appearance in the case. In Colorado, these meetings are typically held by video (or occasionally by phone), and the trustee—not the judge—runs the meeting.

What the Bankruptcy Trustee Does

The trustee is a neutral party, but they are also a watchdog. In a Colorado bankruptcy case, the trustee will:

- Review your petition, schedules, tax returns, pay stubs, and bank statements for accuracy and completeness.

- Confirm that you have disclosed all assets, income, debts, and recent transfers.

- Evaluate your claimed Colorado exemptions to see what property is protected.

- Determine whether there are any non-exempt assets that could be sold for the benefit of creditors (in chapter 7).

- Monitor plan payments and feasibility in chapter 13 cases.

- Communicate with creditors and the U.S. Trustee Program when issues arise.

A Colorado bankruptcy attorney will typically communicate with the trustee on your behalf, respond to document requests, and address any concerns before they turn into formal objections or litigation.

What To Expect at Your 341 Meeting in Colorado

The 341 meeting is usually scheduled about a month after your case is filed. It is not a trial, and there is no judge present. Instead, you, your attorney, and the trustee appear—often by Zoom—so the trustee can verify your identity and ask questions about your paperwork.

- You will present a valid photo ID and proof of your Social Security number.

- You will be placed under oath and must answer questions honestly about your income, assets, debts, and recent financial history.

- The trustee may ask follow-up questions about any unusual transactions, large payments, or property transfers.

- Creditors have the right to attend and ask limited questions, but in many consumer cases, no creditors appear.

- Most 341 meetings in straightforward chapter 7 and chapter 13 cases last only a few minutes if your paperwork is complete and accurate.

Your Colorado bankruptcy lawyer will prepare you for the 341 meeting in advance, explain the typical questions, and attend the meeting with you so you are not navigating the process alone.

How To Find Your Trustee and 341 Meeting Information

After you file, you will receive an official Notice of Bankruptcy Case from the court. That notice lists the name of your assigned trustee and the date, time, and format (usually Zoom) of your 341 meeting. If you misplace the notice or want to double-check information:

- You can look up Chapter 7 panel trustees for Colorado on the U.S. Department of Justice’s U.S. Trustee Program Region 19 page, which covers the District of Colorado.

- You can review current information about 341 meetings, including Zoom procedures and calendars, on the Colorado bankruptcy court’s website, starting with its First Meeting of Creditors page.

- Your attorney can also access your case docket and trustee information through the court’s electronic filing system and confirm any updates or changes to your 341 meeting.

Using these official resources—and working closely with a Colorado bankruptcy attorney—helps ensure you know exactly who your trustee is, when and how to attend your 341 meeting, and what to expect at each step in the process.

What Happens to Your Assets in Colorado Bankruptcy?

One of the biggest worries people have about Colorado bankruptcy is, “Am I going to lose everything?” The good news is that the system is not designed to leave you with nothing. Federal law and Colorado-specific protections work together so that, in most consumer cases, people keep the property they actually need to live and work.

In a chapter 7 case, a trustee reviews your property to see whether there is anything that is not protected under Colorado law. If all of your assets are covered by applicable protections, your case is often treated as a “no-asset” case—meaning there is nothing for the trustee to sell for the benefit of creditors. If something is not protected, the trustee may consider selling it or negotiating a buy-back, but this is highly fact-specific and depends on the value of the property and the cost of liquidation.

In a chapter 13 case, the analysis is different. Instead of selling property, you usually keep your assets and propose a three- to five-year repayment plan. The amount you must pay unsecured creditors is influenced by what would have been available to them in a hypothetical chapter 7 case. In other words, the value of any non-protected property can affect how much you have to pay into your plan, even if you’re not actually giving that property up.

Rather than going deep into the details here, the specifics of Colorado protection rules are covered on a dedicated page. For a closer look at how Colorado law treats homes, vehicles, personal property, and wages, see our Colorado bankruptcy exemptions guide.

Key Points to Consider

- In chapter 7, a trustee reviews your property and may administer only items that are not protected by Colorado law.

- In chapter 13, you usually keep your property, but the value of non-protected assets can influence how much you must pay unsecured creditors.

- The exact protection rules are Colorado-specific and can change, so it’s important to review current law and resources.

- A Colorado bankruptcy attorney can analyze your home equity, vehicles, retirement accounts, and other assets and help you choose a path that protects as much as possible.

The Automatic Stay in Colorado Bankruptcy: Protection From Creditors

One of the most powerful immediate benefits of a Colorado bankruptcy filing is the automatic stay. As soon as you file your case with the United States Bankruptcy Court for the District of Colorado, federal law under 11 U.S.C. § 362 generally requires most creditors to stop collection activity. Whether you are filing bankruptcy in Colorado under chapter 7 or chapter 13, the automatic stay is often the answer to a very real, practical question: “What happens to the calls, lawsuits, and garnishments once I file?”

In a typical bankruptcy Colorado case, the automatic stay can immediately pause wage garnishments, foreclosure sales, repossessions, and many types of collection lawsuits. It is not permanent—it lasts while your case is active and has important exceptions—but it often provides the breathing room people need to make thoughtful decisions about how to move forward under Colorado bankruptcy laws instead of reacting in crisis mode.

Benefits of the Automatic Stay

- Stops most collection calls and letters from creditors and debt collectors.

- Temporarily halts many wage garnishments so your paycheck is not drained while your Colorado bankruptcy is pending.

- Can pause foreclosure, repossession, and certain civil lawsuits, giving you time to explore your options.

- Prevents most utility shutoffs for a limited time, so essential services are not cut off immediately after filing.

The automatic stay does have limits—for example, it does not stop certain family-support obligations or criminal proceedings, and creditors can sometimes ask the court to lift the stay. Because these rules blend federal law with local practices in the Colorado bankruptcy court, it is important to get advice that fits your situation.

If you are considering filing bankruptcy in Colorado and want to understand exactly how the automatic stay would apply to your garnishments, lawsuits, or foreclosure, speaking with an experienced Colorado bankruptcy attorney is the best way to get clear, case-specific guidance before you take the next step.

Credit Counseling and Debtor Education Requirements

Two often-overlooked parts of filing bankruptcy in Colorado are the required credit counseling course before you file and the debtor education (financial management) course after you file. These are not optional add-ons—they are built into federal law and apply in every Colorado bankruptcy case, whether chapter 7 or chapter 13.

Under 11 U.S.C. § 109(h), most individuals must complete an approved credit counseling session in the 180 days before filing. This session helps you review your budget, look at alternatives to bankruptcy, and confirm that a bankruptcy Colorado filing is the right step. If you file without a valid, timely credit counseling certificate on file, your case can be dismissed even if everything else is correct.

After your case is filed, you must also complete a separate debtor education or financial management course before you can receive a discharge. For chapter 7 cases, this requirement appears in 11 U.S.C. § 727(a)(11); for chapter 13, it appears in 11 U.S.C. § 1328(g). The focus of this course is forward-looking: tools for budgeting, using credit wisely, and avoiding the kinds of problems that led to filing bankruptcy in Colorado in the first place.

What Each Course Does and Where To Find Providers

Not every online “course” will satisfy these requirements. You must use providers approved by the U.S. Trustee Program. Here’s a quick overview:

| Course | When & What It Covers | Approved Providers |

|---|---|---|

| Credit Counseling (Pre-Filing) | When: Within 180 days before filing your Colorado bankruptcy case. Covers: Income, expenses, and debts; basic budgeting; non-bankruptcy options; certificate required to file. | U.S. Trustee Program list of approved credit counseling agencies (choose “Colorado”) on the U.S. Trustee Program website. |

| Debtor Education / Financial Management (Post-Filing) | When: After filing and before discharge. Covers: Budgeting, rebuilding credit, using credit wisely, planning ahead after bankruptcy. | U.S. Trustee Program list of approved debtor education providers (select “Colorado”) on the U.S. Trustee Program website. |

Essential Steps

- Complete an approved credit counseling session within 180 days before filing your Colorado bankruptcy case.

- Provide the credit counseling certificate to your attorney so it can be filed with or shortly after your petition.

- After filing, complete an approved debtor education (financial management) course.

- Make sure the debtor education certificate is filed before the court enters your discharge.

Failing to complete either of these requirements can delay your case, lead to dismissal, or prevent you from receiving a discharge. A Colorado bankruptcy attorney will typically build these courses into your overall filing plan, remind you of deadlines, and ensure the certificates are properly filed so these technical steps don’t derail your fresh start.

The Impact of Bankruptcy on Your Credit and Financial Future

Filing for bankruptcy in Colorado will show up on your credit reports and can cause an initial drop in your credit score. A chapter 7 case can remain on your report for up to 10 years, and a chapter 13 typically remains for about7 years. That sounds scary, but it’s only part of the story—and not always the most important part.

For many people considering Colorado bankruptcy, their credit is already damaged by late payments, maxed-out cards, collections, and lawsuits. In that situation, eliminating unmanageable debt through bankruptcy can actually be the turning point where credit starts to recover, not permanently collapse. Lenders look at more than just the presence of a bankruptcy—they also look at what you’ve done since.

Key Impacts on Credit

- Expect a noticeable initial drop in your credit score when you file bankruptcy in Colorado, especially if you started with relatively high scores.

- The bankruptcy entry can remain on your report for up to 7–10 years, depending on the chapter, but its impact usually fades over time—especially if you rebuild positive history.

- Eliminating old, unpayable debt can actually make it easier to manage your budget, pay bills on time, and build healthier credit going forward.

In other words, bankruptcy Colorado is not the end of your financial story; it’s a reset point. What you do in the months and years after your case matters just as much as the filing itself.

Practical Tips for Rebuilding After Colorado Bankruptcy

The most encouraging news: many people see their scores begin to improve within 12–24 months after a discharge if they follow consistent, basic steps. Here are practical ways to move your credit in the right direction after a Colorado bankruptcy:

- Check your credit reports regularly. After your discharge, pull reports from all three major bureaus to ensure discharged debts are reported correctly and old balances are showing as included in bankruptcy or zeroed out.

- Build a clean on-time payment history. Pay every remaining bill—rent, utilities, cell phone, car, student loans—on time, every month. Consistent on-time payments are one of the strongest positive signals in modern scoring models.

- Consider a secured credit card or credit-builder loan. Used carefully (low balances, paid in full monthly), these can help you reestablish revolving or installment credit without overspending.

- Keep credit utilization low. If you have or obtain a card after bankruptcy, try to keep your reported balance under about 30% of the limit—and lower is usually better.

- Avoid new high-interest debt traps. Be cautious with offers that target recent filers, such as high-fee cards or loans. Focus on simple, affordable tools that genuinely build credit instead of draining your budget.

- Create and follow a realistic budget. Use the breathing room from your Colorado bankruptcy discharge to build savings, plan for emergencies, and stay out of the paycheck-to-paycheck cycle.

A Colorado bankruptcy attorney can’t promise a specific credit score, but they can help you understand what lenders typically look at after a bankruptcy and how to position yourself for a stronger financial future. When combined with consistent habits, bankruptcy can be the starting line—not the finish line—of rebuilding your credit and long-term financial health.

Alternatives to Bankruptcy in Colorado

A Brief, Attorney-Led Overview

Bankruptcy isn’t the only path to dealing with debt in Colorado, but when you’re facing wage garnishments, repossession threats, or a looming foreclosure, a Colorado bankruptcy filing is often the most predictable legal tool on the table. If you’re exploring options, do it with an experienced Colorado bankruptcy lawyer so you don’t trade short-term relief for long-term damage.

A good attorney will walk you through both non-bankruptcy options and what filing bankruptcy in Coloradowould look like under the Colorado bankruptcy laws that apply to your home, car, wages, and other assets.

When Non-Bankruptcy Options May Help

- Nonprofit Credit Counseling / DMP: A structured plan that can lower interest rates and consolidateunsecured credit cards into one monthly payment through a nonprofit agency. A good on-time payment record can help with credit rebuilding, but these plans usually do not stop lawsuits, garnishments, or foreclosure activity once it has started.

- Direct Negotiation / Settlements: Case-by-case lump-sum or installment settlements with individual creditors. This can make sense if you have a limited number of accounts and access to funds for realistic offers. You still face lawsuit and garnishment risk while negotiations drag on, and forgiven balances may create taxable income.

- Refinance / Consolidation Loans: Sometimes lowers interest and simplifies payments if you qualify for a decent rate. But rolling credit cards into a home-equity loan or car note can turn a credit-card problem into a house-or-car problem if you later default—especially risky when Colorado housing costs and car prices are high.

- Short-Term Hardship Arrangements: Temporary forbearance or reduced payments after a job loss, medical issue, or other short-term setback. This can help when your income is likely to recover soon; it’s less helpful when the numbers simply don’t work anymore and the debt is structurally unpayable.

Red Flags With For-Profit “Debt Relief” Companies

- Pressure to pay large upfront fees or ongoing “program fees” before any meaningful results are delivered.

- Advice to stop paying all your creditors so accounts “go delinquent” and become “easier to settle”—often leading to lawsuits, judgments, and garnishments here in Colorado while you’re still in the program.

- Promises of guaranteed results, “one payment solves everything,” or claims that “bankruptcy is never necessary” without a careful review of your entire financial picture.

- No clear, written explanation of tax consequences, lawsuit risk, or the fact that creditors are free to refuse settlements and keep collecting.

Why Many Coloradans Still Choose Bankruptcy

- Immediate legal protection: Once you file a case with the United States Bankruptcy Court District of Colorado, the automatic stay can stop most collection lawsuits, garnishments, repossessions, and foreclosure actions while your Colorado bankruptcy case is pending.

- Predictable end point: Chapter 7 typically leads to a discharge of qualifying debts in a matter of months, while chapter 13 provides a structured, court-enforced repayment plan with a clear three- to five-year timeline.

- Built-in asset rules: Federal law and Colorado bankruptcy laws (including the Colorado exemption system) create a transparent framework for what you keep and what, if anything, must be paid to creditors—much more predictable than one-off negotiations with each creditor.

Best Practice: Compare Paths With Colorado Counsel

Before you commit to a for-profit “debt consolidation” or “debt relief” program, have a Colorado bankruptcy attorney review your debts, income, assets, and goals. If a nonprofit debt-management plan, targeted settlement strategy, or other non-bankruptcy option truly beats a chapter 7 or chapter 13 outcome in your situation, a good lawyer will tell you that—and help you avoid companies that put their fees ahead of your long-term financial health.

On the other hand, if filing bankruptcy in Colorado under chapter 7 or chapter 13 provides more predictable protection and a faster path to a fresh start, your attorney can explain how the process works in the District of Colorado, how the exemptions apply to your property, and what life typically looks like after a Colorado bankruptcy discharge.

Choosing a Bankruptcy Attorney in Colorado

If you’ve decided that filing bankruptcy in Colorado might be the right move, choosing the right lawyer is one of the most important decisions you’ll make. A skilled Colorado bankruptcy attorney does far more than “fill out forms”— they help you choose the right chapter, apply Colorado bankruptcy laws to protect as much property as possible, and guide you through the United States Bankruptcy Court District of Colorado with fewer surprises and headaches.

You’ll want someone who understands both the federal Bankruptcy Code and the Colorado-specific rules on exemptions, garnishments, and local court practices. Experience with the trustees and judges who regularly handle bankruptcy Colorado cases can make the process smoother, because your lawyer will know which issues tend to draw extra scrutiny and how to address them in advance.

Consider the Following When Hiring a Colorado Bankruptcy Lawyer

- Specialization in bankruptcy law: Look for an attorney whose practice focuses heavily on consumer bankruptcy rather than someone who only occasionally takes these cases. Membership in bankruptcy sections or bar associations can be a good sign of commitment to this area.

- Colorado-specific experience: Ask how many chapter 7 and chapter 13 cases they file each year in the District of Colorado, and whether they regularly appear before the local trustees and judges who will likely handle your case.

- Experience with cases like yours: If you own a small business, have tax debt, are behind on a mortgage, or have substantial retirement or investment accounts, ask whether the attorney has handled similar situations and how those cases were resolved.

- Communication and accessibility: You should feel comfortable asking questions and confident that the attorney (and their team) will explain deadlines, documents, and court requirements in plain language—not legal jargon.

- Fees and payment options: Make sure you understand the total fee, what’s included, and whether payment plans are available—especially important in chapter 13, where some attorney fees may be paid through the repayment plan.

- Initial consultation: Many Colorado bankruptcy attorneys offer a free or reduced-cost consultation. Use that time to ask about filing bankruptcy in Colorado, compare chapter 7 vs. chapter 13, and decide whether the attorney feels like the right fit for you and your goals.

The right lawyer can make a complex Colorado bankruptcy feel manageable and predictable—from your first strategy session to the day you receive your discharge.

Common Myths and Mistakes in Colorado Bankruptcy

Misunderstandings about Colorado bankruptcy can lead people to delay too long, file in the wrong chapter, or make avoidable mistakes that cost them money or assets. A few myths and missteps show up again and again when people are considering bankruptcy Colorado for the first time.

Persistent Myths

- “All my debts will be wiped out.” In reality, certain obligations—like most student loans, recent taxes, child support, and alimony—are usually not discharged. Assuming everything disappears can create painful surprises unless you review your specific debts with a Colorado bankruptcy attorney.

- “I’ll lose everything if I file.” Colorado law includes an exemption system specifically designed so you can keep essential property while dealing with unaffordable debt. Most well-planned consumer cases are structured so people keep their basic household goods, modest vehicles, and protected equity.

- “Filing means I’ve failed financially.” Job loss, medical issues, divorce, business closures, and rising living costs are common triggers. Bankruptcy is a legal tool built into the system—not a moral judgment—and for many people, it’s the first real step toward stability.

Costly Mistakes to Avoid When Filing Bankruptcy in Colorado

- Transferring or “hiding” assets before filing: Signing a car over to a relative, moving money out of accounts, or selling property for far less than it’s worth right before a Colorado bankruptcy can trigger “fraudulent transfer” issues and put both you and the recipient at risk.

- Paying back friends or family right before filing: Large payments to insiders shortly before a case can be treated as “preferential transfers,” and the trustee may try to claw that money back. Always talk to counsel before paying anyone off in the months leading up to a filing.

- Draining retirement accounts to pay unsecured debt: Many retirement accounts are protected in bankruptcy, but once you cash them out to pay credit cards or medical bills, that money loses its protection. This is one of the most common and painful pre-bankruptcy mistakes.

- Filing without understanding Colorado bankruptcy laws: Using generic online forms or “do-it-yourself” advice that ignores Colorado-specific exemptions and local practices can lead to lost property, case dismissal, or denial of discharge.

- Waiting too long to get advice: People often wait until after a garnishment, foreclosure sale date, or judgment lien to speak with an attorney. Early advice usually provides more options and better outcomes than last-minute emergency filings.

- Not seeking professional legal advice at all: The Bankruptcy Code is federal, but how it interacts with Colorado bankruptcy laws and local court procedures is complex. A Colorado bankruptcy attorney can help you avoid these traps and choose a strategy that actually improves your long-term financial picture.

Taking time to separate myths from reality—and to avoid common mistakes—can make your experience with filing bankruptcy in Colorado far less stressful and far more effective in delivering the fresh start the law is meant to provide.

Frequently Asked Questions About Bankruptcy in Colorado

What types of bankruptcy can I file in Colorado?

Most individuals filing bankruptcy in Colorado choose between chapter 7 and chapter 13. Chapter 7 is generally for people with limited disposable income who need a faster discharge of qualifying unsecured debts, while chapter 13 is a three- to five-year repayment plan for those with regular income who need time to catch up on secured debts like a mortgage or car loan. Chapter 11 and chapter 12 exist as well, but are used far less often for typical consumers.

How do you file for bankruptcy in Colorado?

At a high level, filing bankruptcy in Colorado involves: (1) completing an approved credit counseling course; (2) meeting with a Colorado bankruptcy attorney to choose the right chapter and review Colorado bankruptcy laws and exemptions; (3) gathering documents like tax returns, pay stubs, bank statements, and a full list of debts and assets; (4) having your attorney prepare and file your petition and schedules with the United States Bankruptcy Court for the District of Colorado; and (5) attending a 341 meeting of creditors. The detailed step-by-step process is covered in the “Step-by-Step Guide to Filing Bankruptcy in Colorado” section above.

How much does it cost to file bankruptcy in Colorado?

The basic court filing fee is currently about $338 for chapter 7 and $313 for chapter 13, the same nationwide. In addition, you will pay for required credit counseling and debtor education courses (often $10–$50 each), plus attorney fees, which are usually the largest cost and vary based on the complexity of your case. Many filers in Colorado use payment plans for attorney fees, and in some chapter 7 cases, the court can allow installment payments or even waive the filing fee if income is very low. For a more detailed breakdown, see the “How Much Does It Cost to File Bankruptcy in Colorado?” section.

How long does the bankruptcy process take?

In a typical Colorado chapter 7 case, it often takes about three to six months from filing to discharge, assuming there are no significant complications. A chapter 13 case lasts much longer—usuallythree to five years—because you make monthly plan payments over time before receiving your discharge.

Will all my debts be discharged?

No. While many unsecured debts such as credit cards, personal loans, and medical bills can be discharged, some debts usually are not. Common non-dischargeable debts include most student loans, recent income taxes, child support, alimony, and certain court-ordered obligations. A Colorado bankruptcy attorney can review your specific debt list and explain which obligations are likely to survive a Colorado bankruptcy and which are not.

What happens to my credit score?

A Colorado bankruptcy filing will usually cause an initial drop in your credit score and will appear on your credit reports for 7–10 years, depending on the chapter. However, many people are already struggling with late payments and collections before filing, and eliminating unmanageable debt often makes it easier to rebuild. With on-time payments, low balances, and careful use of new credit, many filers see their scores begin to improve within 12–24 months after discharge.

What is the role of the bankruptcy trustee?

The trustee is a neutral third party appointed to oversee your Colorado bankruptcy case. The trustee reviews your petition and documents, conducts the 341 meeting of creditors, evaluates your claimed exemptions, determines whether any non-protected assets can be administered for the benefit of creditors, and in chapter 13 cases monitors your plan payments. The trustee does not work for you or for your creditors—they are responsible for making sure the case complies with the Bankruptcy Code and Colorado-related rules.

Do I have to go to court in person in Colorado?

Most individuals never appear before a judge in a courtroom. Instead, you must attend a 341 meeting of creditors, which in Colorado is often conducted by Zoom or telephone and is run by the trustee, not the judge. Your attorney will attend with you. In more complex cases, there may be additional hearings, but your lawyer will typically handle most of the speaking in court.

Can I keep my house or car if I file bankruptcy in Colorado?

Many people filing bankruptcy in Colorado are able to keep their home and vehicle, as long as the equity fits within applicable protection rules and they can keep up with required payments. Whether you file chapter 7 or chapter 13, Colorado bankruptcy lawsand exemptions play a major role in this analysis. The details are covered more fully in the sections on assets and in the Colorado exemptions guide, but this is a question you should always discuss in detail with a Colorado bankruptcy attorney before filing.

Is Bankruptcy in Colorado the Right Move for You?

Deciding whether to move forward with a Colorado bankruptcy is a serious, personal decision. It’s not just about forms and court dates—it’s about your home, your paycheck, your family, and your long-term financial stability. Bankruptcy can’t fix everything, and it does come with consequences for your credit and future borrowing, but for many people it is also the moment when the constant crisis finally stops and a real rebuilding plan begins.

As you weigh your options, it can help to ask a few focused questions: Are you realistically able to pay down your debts in the next few years without falling behind on essentials? Are garnishments, lawsuits, or collection pressure making it impossible to catch up? Do the protections built into Colorado bankruptcy laws—including exemptions and the automatic stay—offer you more stability than another round of balance transfers or “debt relief” programs? Honest answers to those questions often clarify whether filing bankruptcy in Colorado is a tool you should seriously consider.

You don’t have to figure this out alone—or based only on what you read online. A conversation with an experienced Colorado bankruptcy attorney can turn a jumble of rules, fears, and “what-ifs” into clear options: what chapter 7 or chapter 13 would look like for you, how your assets would likely be treated, what it might cost, and how your credit could be rebuilt afterward. Whether the best path is bankruptcy, a non-bankruptcy alternative, or a combination of strategies, getting grounded, state-specific advice is often the first real step toward the financial reset you’ve been hoping for.

Explore Our Colorado Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin