Bankruptcy Chapter 7 Colorado: What You Need to Know

- Colorado exemptions control what you can protect: In most cases, Colorado filers use Colorado bankruptcy exemptions to protect essentials (like a home, a vehicle, and personal property). What’s protected depends on the category and your specific facts.

- The “median income” screen is a quick starting point: You can jump to the Colorado median income table on this page. These numbers are updated over time, so the filing-date version matters.

- Where you file depends on the Colorado federal district: Use the “Where you file in Colorado” section to find the official court information for your area (court details and meeting formats can change).

- What the process usually looks like: Most Chapter 7 cases follow the same core steps—paperwork, a trustee review, a required meeting, and (if eligible) a discharge. For the full federal overview, see the national guide: Chapter 7 bankruptcy basics.

- Best way to use this page: Focus first on (1) exemptions, (2) the median income snapshot, and (3) where you file. Those are the parts that tend to change outcomes the most for Colorado residents.

Soft next step: See if your property is protected by Colorado exemptions → Colorado bankruptcy exemptions

If you’re looking at Chapter 7 in Colorado, you probably don’t need another generic explanation—you need clarity on what could happen to the things that keep life running: your paycheck, your housing, your car, and the property you rely on day to day. This page focuses on the Colorado-specific pieces that tend to matter most (exemptions, the median-income snapshot, and where you file) so you can get oriented quickly. This is general information (not legal advice).

What’s Different About Chapter 7 in Colorado

The big worries are usually the same: Will I lose my home or car? Can I keep my paycheck? Where do I even file? The helpful part is that the Colorado-specific answers tend to cluster in a few places—so you don’t have to read a “one-size-fits-all” guide to get value from this page.

- What you keep is mainly about Colorado exemptions: Most Colorado residents rely on Colorado bankruptcy exemptions to protect everyday necessities (often things like home equity, a vehicle, household goods, and certain benefits). Small details—like how property is titled or classified—can affect how an item fits into an exemption category.

- Eligibility often starts with a quick Colorado income check: The first checkpoint is usually whether your household income is under or over the Colorado median for your household size. You can jump straight to the Colorado median income snapshot on this page.

- Where you file is Colorado-specific (and it’s worth using official links): Your case is filed in the federal bankruptcy court that serves Colorado, and the practical details (clerk info, addresses, current procedures) are best verified on the official court site. Use the Where You File Chapter 7 in Colorado section for the official resources.

- The overall steps are mostly federal: Things like the automatic stay, trustee review, the required meeting, and the discharge rules come from federal law. If you want the full “how it works” overview, use the national guide: Chapter 7 bankruptcy basics.

If you’re trying to save time, start with exemptions and where you file. Those two areas are most likely to change what happens in real life.

Colorado Median Income Snapshot

This is the quick “starting point” for the Chapter 7 means test: how your household income compares to the Colorado median for the same household size. If you’re under the median, you often clear the first screen more easily. If you’re over the median, it doesn’t automatically mean you can’t file—it usually means the next step is the full means test calculation.

If you want the step-by-step breakdown, see our means test guide.

Reliability note: these median-income figures are updated from time to time, so the version that matches your filing date is the one that matters. The source link below is the best place to confirm the current numbers.

| Household Size | Annual Median Income (USD) |

|---|---|

| 1 | $85,685 |

| 2 | $106,690 |

| 3 | $127,495 |

| 4 | $149,566 |

| Median income figures are updated periodically. Always confirm the current numbers for your filing date. | |

Source: U.S. Trustee Program — Median Family Income [updated February 2, 2026]

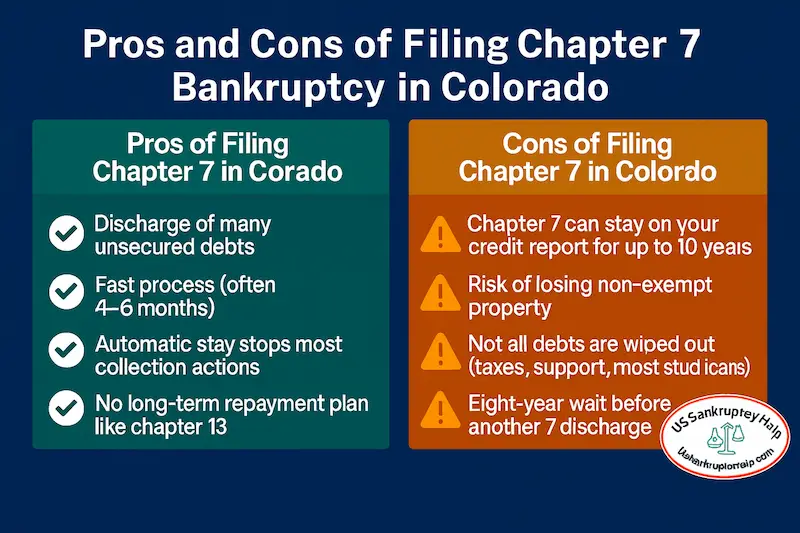

Protecting a Home and Car in Chapter 7 in Colorado

For many Colorado filers, the biggest property concerns are a home and a vehicle. In Chapter 7, the practical question is usually about equity—the value of the property minus any loans—because exemptions often protect equity up to certain limits and within certain categories.

- Home equity: Colorado’s homestead-related protections may help protect equity in a primary residence. Whether your home is protected depends on your equity, how the exemption applies to your situation, and whether there are any special issues (like co-owners or recent transfers).

- Car equity: Vehicle protection often depends on how much equity you have and how the vehicle exemption applies. A paid-off vehicle can have more equity exposure than a financed one, depending on its value and your loan balance.

- If you’re making payments: Bankruptcy can address personal liability for many debts, but it doesn’t automatically change a lender’s rights in collateral. If you want to keep a financed home or car, staying current (or getting current) is often part of the picture.

- Small details can change the outcome: Title, co-borrowers, recent refinancing, and how property is used can all affect how exemptions apply.

The most practical next step is to compare your estimated equity to the Colorado exemption categories that could apply. For a Colorado-focused overview of those categories, see our Colorado exemptions guide.

Where You File Chapter 7 in Colorado

If you’re wondering where a Chapter 7 case actually gets filed, Colorado cases go through the United States Bankruptcy Court for the District of Colorado. The most useful next step is to use the court’s official site to confirm the current addresses, clerk’s office contact info, and filing instructions—because these logistics can change and you don’t want to rely on outdated third-party pages.

- Official court website: U.S. Bankruptcy Court — District of Colorado

- Court locations and mailing address: Court Locations (District of Colorado)

- Filing information (including resources for people filing without an attorney): Filing Without an Attorney

- Electronic filing (CM/ECF) info: Electronic Filing Information

- Contact the court: Contact Us

Court procedures and logistics can change over time. For anything time-sensitive (like addresses, submission methods, or meeting formats), rely on the court’s official pages and the notices issued in a specific case.

Chapter 7 Process in Colorado

If you’re feeling overwhelmed, it helps to know what the process usually looks like in plain English. Most cases follow the same basic path—your job is mainly to be organized, meet deadlines, and understand what the trustee is looking for.

- Step 1: Gather the basics: Recent pay stubs or income records, tax returns, bank statements, a list of debts, and a list of what you own. This is what the forms are built from.

- Step 2: File the case: Your petition and schedules are filed with the bankruptcy court. After filing, you’ll get official case notices with key dates and instructions.

- Step 3: The automatic stay starts: Most collection activity must stop while the case is pending. If you’re facing active collections, the court notice is what matters most.

- Step 4: Trustee review: A Chapter 7 trustee reviews what was filed and may ask for follow-up documents. This is also where exemptions matter—because exemptions determine what property is treated as protected.

- Step 5: Attend the required meeting: You attend a short required meeting where the trustee asks standard questions and confirms identity documents. Most people find it more routine than they expect.

- Step 6: Finish the required items: After that, many routine cases move toward a discharge of qualifying debts once deadlines pass and required steps are completed.

If you want the full federal walkthrough (including the means test, required courses, and what debts are typically affected), you can use our Chapter 7 bankruptcy basics guide.

Colorado Chapter 7 FAQs

These are the questions people in Colorado ask most when they’re trying to figure out “Will this actually work for me?” If you’re short on time, you can skim the headings and jump to the one that matches your situation.

How long does a Chapter 7 case usually take in Colorado?

Many Chapter 7 cases move from filing to discharge in a few months, but the timeline depends on document readiness, trustee requests, and whether anything in the case needs extra review. Your case notices will always show the key dates that matter.

Do I have to be under the Colorado median income to file Chapter 7?

Not necessarily. Being under the Colorado median income is often a simpler starting point, but being over the median doesn’t automatically mean you can’t file. If you’re comparing your household income, start with the Colorado median income snapshot above, and use the national guide for the full means test overview.

Can I keep my home or car in a Colorado Chapter 7?

The practical question is usually about equity and how Colorado exemption categories apply. Many filers are able to protect common essentials, but outcomes depend on the facts (value, loan balances, title, and exemptions). Start with the Colorado exemptions page:

How much cash can I protect in Colorado?

Colorado exemptions can protect certain types of funds and money sources, but the category and how the funds are held can matter (for example, wages, benefits, or funds traceable to exempt sources). For a Colorado-focused overview of the categories to check, see the exemptions page linked above.

Do both spouses have to file Chapter 7 in Colorado?

No. Some households file jointly, and others file with one spouse only. The right approach often depends on who owes which debts, whether debts are joint, and how property is titled.

Where do I file a Chapter 7 case in Colorado?

Chapter 7 cases are filed in the U.S. Bankruptcy Court that serves Colorado. For official court links and current procedures, use the Where You File Chapter 7 in Colorado section on this page.

For broader questions about how Chapter 7 works nationwide (including the full process and what debts are typically affected), see Chapter 7 bankruptcy basics.

If you’re under the median for your household size, that’s usually a simpler starting point. If you’re over the median, you may still qualify after the full means test calculation. For the full federal overview of how the means test works, see Chapter 7 bankruptcy basics.

Next Steps After Reading This Colorado Chapter 7 Guide

If you’re stressed and trying to make a decision, here’s a practical way to use what you just read. These are the three checks that most often change the outcome for Colorado residents: what you can protect, whether the means test needs a deeper look, and the official court instructions for filing.

- Check Colorado exemptions first: Compare what you own (and your estimated equity) against Colorado’s exemption categories.

- Confirm the Colorado median income snapshot: Use the filing-date version and keep the source in mind if your case timing changes.

- Use official court links: For addresses, filing procedures, and current requirements, rely on the District of Colorado court pages in the “Where You File” section.

If Chapter 7 isn’t a fit (for example, because of income, property concerns, or the need to catch up on secured payments), Chapter 13 is the most common court-supervised alternative in Colorado. You can read that overview here: Colorado Chapter 13 bankruptcy.

If you want the broader nationwide overview of Chapter 7, you can use our Chapter 7 bankruptcy basics guide.

Reminder: This page provides general information, not legal advice. For the most reliable procedural details, always rely on official court notices and the court’s website.

Trust and Sources

This page is general information, not legal advice. For the most reliable, up-to-date details on procedures and official requirements, use primary sources like the bankruptcy court and the U.S. Trustee Program.

- Colorado bankruptcy court: U.S. Bankruptcy Court — District of Colorado

- U.S. Trustee Program (trustees and case administration): U.S. Trustee Program

- Private Trustee Locator: Private Trustee Locator

- U.S. Trustee Region 19 (Colorado-related administration): Region 19 — Chapter 7 (U.S. Trustee Program)

If anything on this page conflicts with a court notice or an official court/UST posting, rely on the official source for the most current direction.

Explore Our Colorado Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin