Can You File Bankruptcy on Medical Bills?

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

Legal Disclaimer

This guide is for educational purposes only and does not constitute legal or financial advice. Bankruptcy laws and discharge eligibility depend heavily on your specific debt structure, asset profile, and court district. Reading this content does not create an attorney-client relationship. Consult a licensed bankruptcy attorney before making filing decisions.

Medical bills, or medical debt, can sneak up on you and build quickly, especially after an unexpected illness or a hospital stay. Medical debt is one of the leading reasons people turn to bankruptcy, according to the American Bankruptcy Institute.

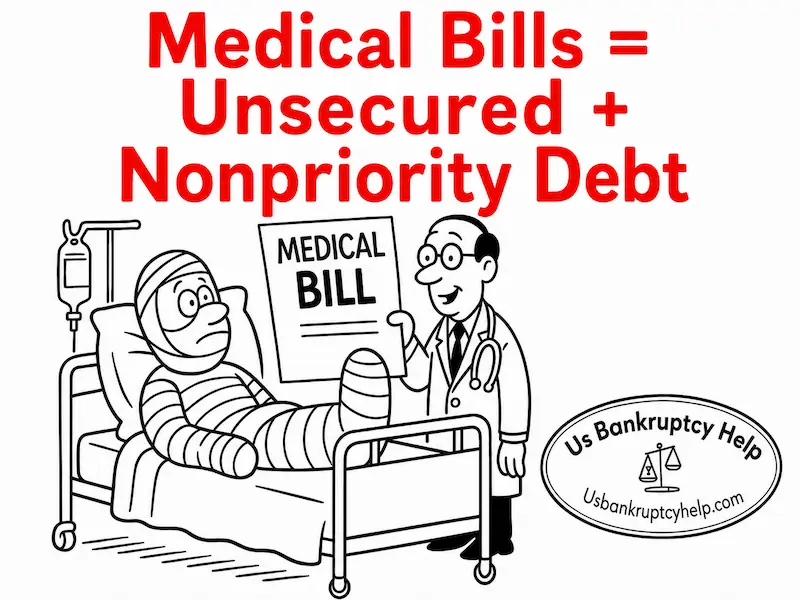

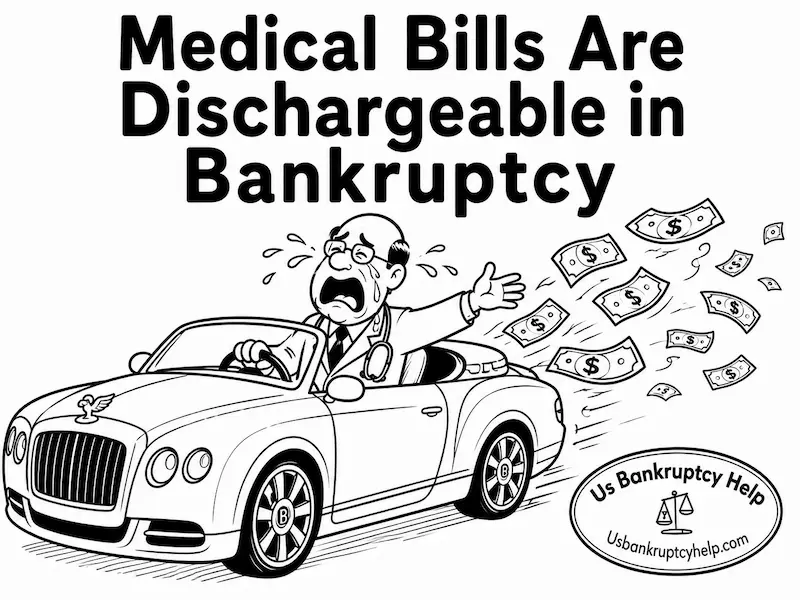

Are Medical Bills Dischargeable in Bankruptcy?

The vast majority of medical debt is treated as unsecured, nonpriority debt under 11 U.S.C. § 507, because it is not secured by collateral and is not included in the priority debt categories listed in the bankruptcy code. This holds true regardless of whether the medical debt stems from emergency room trauma, overnight hospital stays, ambulance fees, or elective medical procedures.

What about medical credit cards? If you paid for medical treatments using a medical credit card (such as CareCredit) or a standard personal loan, that debt is also treated as unsecured, nonpriority debt. Like standard hospital bills, medical credit card balances are equally eligible for discharge.

For these reasons, medical bills are almost always eligible for discharge in bankruptcy. How and when the discharge happens differs depending on the chapter of bankruptcy you file.

Drowning in Medical Debt and Collection Calls?

You don't have to face aggressive hospital billing departments alone. Speak with an experienced bankruptcy attorney to evaluate your options and protect your paycheck.

Chapter 7 vs Chapter 13: Which Is Right for Me if I Have Medical Bills?

If you have medical bills, they are dischargeable in both chapter 7 and chapter 13. Which chapter is right for you depends on your unique circumstances.

Medical debt is only one factor to consider when deciding which chapter may be best for your financial situation. To evaluate your income, assets, and goals side-by-side, use our interactive Chapter 7 vs Chapter 13 Decision Tool. It is entirely free, completely confidential, and does not require any contact information to view your results.

Chapter 7 for Medical Bills

If you have a lot of medical debt and qualify for discharge under the means test, chapter 7 can wipe the slate clean by discharging unsecured debts like medical bills in a relatively short period of time. For this reason Chapter 7 could be a good option for those who need a fresh start.

Chapter 13 for Medical Bills

Chapter 13 can be a good option if you don't qualify for chapter 7, or your situation would be better suited for the benefits of a chapter 13 bankruptcy. Medical bills are dischargeable in chapter 13 bankruptcy, but the discharge usually happens after the three to five year plan payment period.

Chapter 7 vs Chapter 13 and Medical Debt Treatment Comparison

Below is a practical comparison to help you understand how each chapter typically treats medical debt. If you want a deeper, side-by-side explanation (beyond medical bills), see our detailed comparison of Chapter 7 vs. Chapter 13 bankruptcy. It walks through common factors like income, property, and goals in plain English.

| Factor | Chapter 7 | Chapter 13 |

|---|---|---|

| How medical bills are treated | Medical bills are treated as nonpriority unsecured debts and can be discharged. | Medical bills may be included in a 3–5 year repayment plan if funds are available. Any remaining balance can be discharged after plan completion. |

| Timeframe | 3 to 6 months on average, assuming no complications. | 3 to 5 years |

| Eligibility / who it may fit | Often used when a filer qualifies under income rules (including the means test) and can protect property using available exemption laws. | Filers must have regular income. Often filed by people who don't qualify for chapter 7, have nonexempt assets, or want to use other chapter 13 benefits. |

| What happens to collections | Filing triggers the automatic stay, which pauses most collection activity while the case is pending. | The automatic stay also applies. Payments are made through the chapter 13 trustee under the plan while the case is active. |

Once your case successfully concludes, the medical debts are not just temporarily paused—they are permanently wiped out by the discharge injunction (11 U.S.C. § 524). This statute legally prohibits medical providers and collection agencies from ever attempting to collect those discharged debts as a personal liability.

What Happens to Medical Collections, Lawsuits, and Garnishments After You File?

If you are experiencing collection actions from creditors, you may be wondering what happens when you file for bankruptcy and whether creditors will stop contacting you. While laws like the Fair Debt Collection Practices Act (FDCPA) limit how third-party debt collectors can harass you, bankruptcy provides a much stronger, immediate shield.

When your bankruptcy case is filed, an automatic stay (11 U.S.C. § 362) generally goes into effect. This court-ordered protection strictly stops most collection activity while your case is pending. This includes wage garnishments and other medical creditor actions, including collection lawsuits and judgments.

Under 11 U.S.C. § 362(k), if a medical collection agency or debt buyer willfully violates the automatic stay by continuing dunning calls or lawsuits after receiving notice, the bankruptcy court can order them to pay actual damages, legal costs, and attorney fees.

My Real-World Experience: Halting Aggressive Medical Collections

"In my practice, some of the most relentless phone calls and collection lawsuits my clients face come from third-party medical debt buyers. The moment we file a bankruptcy petition, the automatic stay triggers an immediate legal halt to those calls, letters, and pending court judgments. If a medical bill collector attempts to contact you after your case is filed, notifying them of the bankruptcy case number forces them to stop immediately.

*Note: Creditors must receive proper notice of the bankruptcy filing for the automatic stay to take full effect on active lawsuits.*"

Frequently Asked Questions About Bankruptcy and Medical Bills

If I File Bankruptcy on Medical Bills, Can My Doctor Stop Treating Me?

Private doctors and medical providers may be able to stop treating you for non-emergency care if you have an outstanding balance that is discharged in bankruptcy. However, some providers may still choose to treat you, especially if you continue using them after the bankruptcy case.

Will a Hospital Deny Me Treatment If I File Bankruptcy on Medical Bills?

Under the federal Emergency Medical Treatment and Active Labor Act (EMTALA, 42 U.S.C. § 1395dd), hospitals with emergency rooms generally cannot deny emergency treatment because of an unpaid medical bill or a bankruptcy filing.

Non-emergency departments within a hospital may have different policies, and some may choose not to provide non-emergency services if you have an outstanding balance that is discharged in bankruptcy. However, many hospitals have financial assistance programs and may work with you to find a solution.

Can I Leave a Medical Bill Out of Bankruptcy?

Some people want to know if they can choose not to list a medical provider they like or want to continue using. However, bankruptcy requires you to list all creditors in your bankruptcy filing under oath. You generally cannot choose to leave out a medical provider if you owe that provider money.

Is Bankruptcy the Right Solution for Your Medical Debt?

Bankruptcy can provide meaningful relief from overwhelming medical bills, but whether it is right for you depends on your unique financial situation. The decision should be based on your full financial picture and not just the size of your medical debt.

For some people, medical debt is temporary and manageable through payment plans, insurance appeals, or hospital financial assistance programs. For others, especially when medical bills are combined with credit cards, personal loans, or lost income, bankruptcy may offer a more complete reset.

It is always a good idea to consult a qualified bankruptcy lawyer in your local area to discuss your specific circumstances.

Ready to Eliminate Your Medical Debt?

Don't let medical bills dictate your financial health. Speak with an experienced bankruptcy attorney to evaluate your options and map out your fresh start.

Explore More National Bankruptcy Guides and Tools

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin