Tennessee Chapter 7 Bankruptcy: What to Expect

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

When bills keep piling up and collection pressure does not let up, filing chapter 7 may give you some immediate breathing room. In many cases, filing triggers the automatic stay, which generally stops wage garnishments, collection calls, lawsuits, and some repossession or foreclosure activity while the bankruptcy case moves forward. This page explains the Tennessee-specific parts of chapter 7, including exemptions, current median income figures, and where cases are filed.

What’s Different in Tennessee for Chapter 7

Most chapter 7 rules are federal, but a few important parts of your case depend on Tennessee law and where you live in the state.

- Tennessee exemptions apply in most cases: Tennessee is an opt-out state, so people filing bankruptcy here usually use Tennessee exemptions instead of the federal bankruptcy exemption set. That matters because exemptions help determine what property you may be able to keep. Review Tennessee exemptions.

- The means test uses Tennessee income figures: Chapter 7 eligibility often starts with a comparison between your household income and Tennessee’s median income for your household size. Those figures update periodically, so it is better to rely on the current table on this page than on an older number. Go to the Tennessee median income table.

- Where you file depends on your district: Tennessee bankruptcy cases are filed in the Eastern, Middle, or Western District of Tennessee, depending on the county where you live. See Tennessee districts and court sites.

- Property questions may need a closer Tennessee-specific review: Rules about what property is protected can be more complicated than the general chapter 7 process itself, especially when you are reviewing home equity, vehicles, or other valuable personal property. That is why the exemption section matters so much for Tennessee filers. See how Tennessee exemptions work.

- Most other chapter 7 rules are federal: The main forms, filing process, deadlines, and many core definitions come from federal bankruptcy law. After you review the Tennessee-specific points here, use our National Chapter 7 guide for the broader process.

This page focuses on the Tennessee rules that most often change the answer: exemptions, current median income figures, and where you file.

Use this quick summary to check which Tennessee-specific rules matter first before you rely on general chapter 7 information.

- Exemptions: Tennessee is an opt-out state, so most people filing here use Tennessee exemption laws instead of the federal bankruptcy exemption set. Before filing, make sure the property you want to keep is protected. Review Tennessee exemptions.

- Means test income figures: Tennessee median income numbers are used in the chapter 7 means test, but they change over time. Use the current table on this page rather than relying on an older number. Go to the Tennessee median income table.

- Where you file: Tennessee bankruptcy cases are filed in the federal bankruptcy court for the district that covers your county. Eastern District, Middle District, or Western District. See Tennessee filing districts.

- How to use this page: Start with the Tennessee-specific rules here, then use our national Chapter 7 guide for the broader chapter 7 process, definitions, and next steps.

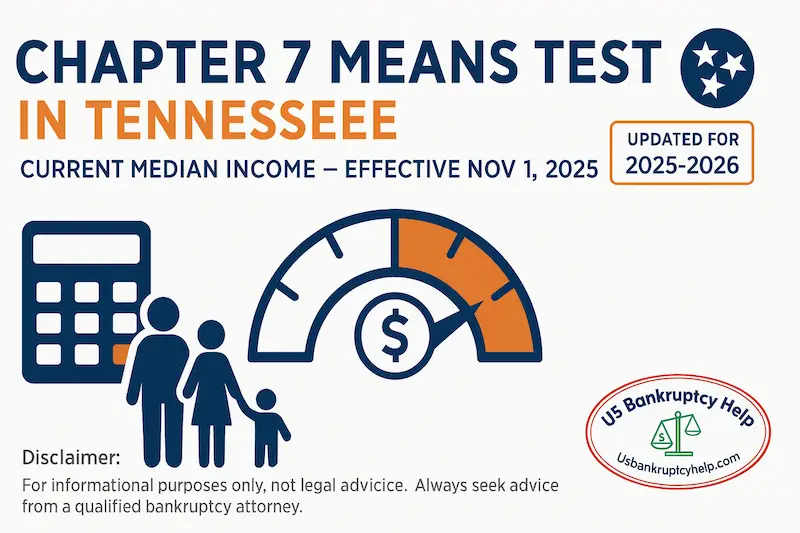

Tennessee Median Income for Chapter 7 Means Test

This table helps with the first step of the chapter 7 means test. You compare your household's current monthly income, based on the six full calendar months before filing, to the Tennessee median income for your household size.

These figures change periodically, so the filing date matters. Use the current table for your case rather than relying on older numbers from another site or an older article.

| Household Size | Annual Median Income | Monthly Median Income |

|---|---|---|

| 1 | $62,339 | $5,195 |

| 2 | $80,722 | $6,727 |

| 3 | $95,011 | $7,918 |

| 4 | $106,775 | $8,898 |

| Each additional person | + $11,100 | + $925 |

These figures apply to cases filed on or after November 1, 2025, and are published by the U.S. Trustee Program for use in the bankruptcy means test. Always confirm the current numbers here: U.S. Trustee Program Median Income Table.

This table is only the starting point. For a fuller explanation of how the means test works, including what happens if your income is above the median, see our chapter 7 means test guide.

Tennessee Chapter 7 Exemptions

In chapter 7, exemptions are the rules that help determine what property you may be able to keep. Tennessee is an opt-out state, so people filing here usually use Tennessee exemption laws instead of the federal bankruptcy exemption set.

- Start with the Tennessee-specific rules: Tennessee bankruptcy exemptions explained.

- Why exemptions matter: In chapter 7, exemption questions often come down to the property you list, its fair market value, your equity in it, and whether a lender already has a lien. That is why using the correct Tennessee exemption rules is so important.

- What people usually review first: Many Tennessee filers start by looking at exemptions that may affect a home, personal property, cash, and retirement funds, then compare those rules to the property they actually own.

This page keeps the overview simple and sends detailed exemption amounts and exceptions to the dedicated Tennessee exemptions guide so the information is easier to verify and maintain.

Tennessee Bankruptcy Guides

Explore Tennessee bankruptcy basics, how chapter 7 works in Tennessee, and the Tennessee exemption rules that may affect what property you can protect.

Protecting a Home and Car

For many Tennessee filers, the biggest practical question is whether a home or car is protected in chapter 7. In most cases, that depends on three things: the property's fair market value, the balance of any mortgage or auto loan, and the Tennessee exemptions that may protect your equity.

- Home equity:Tennessee's homestead rules may protect some equity in a principal residence. The starting point is usually how much equity you have, whether the property qualifies, and which Tennessee homestead rules apply.

- Car equity:Tennessee does not use a separate motor-vehicle exemption in the same way some states do, so vehicle protection often comes down to the car's value, the loan balance, and whether available Tennessee personal-property exemptions cover your equity.

- Loan status still matters:Even if your equity is exempt, a mortgage or car lender's lien usually survives bankruptcy unless a separate legal basis changes that result. In other words, protecting equity and staying current on secured debt are often two different issues.

- Best Tennessee-specific next step: Review the Tennessee exemptions guide.

For the broader national overview of how chapter 7 treats secured debts and collateral, see our National Chapter 7 guide.

Where You File in Tennessee

Chapter 7 cases in Tennessee are filed in the federal bankruptcy court district that covers your county. Tennessee has three bankruptcy districts: Eastern, Middle, and Western.

- Eastern District of Tennessee: Official court site

- Middle District of Tennessee: Official court site

- Western District of Tennessee: Official court site

Use your district’s official site to confirm court locations, county or division coverage, filing instructions, local forms, and current court procedures before you file.

How Chapter 7 Usually Works

On this Tennessee page, the state-specific parts are mostly exemptions, median income figures, and where you file. Most of the chapter 7 process itself is federal, so this section gives a short overview and then points you to the full national guide.

- Before filing: People usually gather information about their income, debts, assets, expenses, and recent financial history. Most individual filers also need to complete an approved pre-filing credit counseling course.

- When the case is filed: The bankruptcy case begins, the automatic stay generally stops many collection efforts, and a chapter 7 trustee is appointed to administer the case.

- After filing: You usually attend a 341 meeting, where the trustee places you under oath and asks questions about your forms, finances, and property. You may also need to provide identification, tax returns, pay stubs, or other requested documents.

- Before discharge: Most individual filers need to complete an approved debtor education course after filing and before a discharge is entered.

- For the full process: Read the National Chapter 7 guide.

Tennessee-Specific FAQs

How do I qualify for chapter 7 in Tennessee?

For many people, the first screening step is the chapter 7 means test. That usually starts by comparing your household income to the current Tennessee median income for your household size. If your income is above the median, that does not automatically mean you cannot file chapter 7, but it usually means the means test needs a closer review. Go to the Tennessee median income table or read our means test guide.

Do I use Tennessee exemptions or federal exemptions?

In most Tennessee cases, people use Tennessee exemptions rather than the federal bankruptcy exemption set. Those rules matter because they help determine what property may be protected in your case. See Tennessee exemptions.

Where do I file a chapter 7 case in Tennessee?

Tennessee chapter 7 cases are filed in the Eastern, Middle, or Western District of Tennessee, depending on your county. This page links to the official court sites here: Where you file in Tennessee.

Can Tennessee exemptions help protect a car or home?

Sometimes, but the answer usually depends on how much equity you have, the balance of any mortgage or car loan, and which Tennessee exemptions apply. Exemption protection and lender lien rights are not always the same issue, so home and car questions often need a closer property-by-property review. Review Tennessee exemptions.

Where can I read the full chapter 7 process that applies nationwide?

This Tennessee page focuses on the state-specific differences. For the broader chapter 7 process, timelines, and federal rules, use the National Chapter 7 guide.

What to Read Next

This Tennessee page covers the main state-specific issues: exemptions, median income, and where you file. From here, the best next step depends on the question you still need to answer.

- If you want the full chapter 7 process: Read the National Chapter 7 guide.

- If you are focused on protecting property: See Tennessee exemptions.

- If you want the broader Tennessee overview: Visit the Tennessee bankruptcy overview.

- If you are comparing bankruptcy chapters: Compare Chapter 7 and Chapter 13.

Explore More National Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin