Understanding Chapter 13 Bankruptcy in Indiana

When bills pile up and the phone won’t stop, Chapter 13 bankruptcy Indiana isn’t about starting over from zero—it’s about catching up with a plan you can actually follow. This chapter pauses most collections, protects essentials, and gives you a court-supervised path to fix what’s behind.

Chapter 13 in Indiana — At a Glance

- What Chapter 13 Is and how it protects essentials while you catch up.

- Eligibility: individual filer, debt limits, counseling, tax returns.

- Process: automatic stay, first payment (~30 days), 341 meeting, confirmation.

- Key Benefits: cure & maintain, vehicle re-org (Till), co-debtor stay.

- Drawbacks: multi-year plan, budget scrutiny, not all debts discharge.

- Exemptions & Plan Floor: best-interests test sets unsecured payout.

- Chapter 13 vs. 7: catch up vs. faster reset—compare scenarios.

- Costs & Fees: filing fee, trustee %, attorney fees (plan-paid).

- Life During & After: payments, approvals, staying organized.

- Credit & Finances: rebuild timeline and playbook.

- FAQ: timing, payments, exemptions, co-signers, conversions.

- Find a Chapter 13 Lawyer: local practice matters (districts/trustees).

- Success Stories: typical Indiana outcomes.

- Alternatives: DMP, settlement, consolidation, chapter 7.

- Is Chapter 13 Right for You?

Think of Chapter 13 Indiana as a structured repayment roadmap. You’ll propose a realistic 3–5 year plan based on your budget; once approved, you make one predictable payment that an Indiana chapter 13 trustee distributes to creditors while you keep your home, car, and paycheck working for you.

By filing chapter 13 bankruptcy in Indiana, the automatic stay immediately stops foreclosures, repossessions, and wage garnishments. Your case starts with a petition and a short credit-counseling course, followed by a plan that explains how you’ll cure arrears and stay current going forward.

A judge must confirm the plan before it takes effect. After confirmation, you continue making that single consolidated payment while the trustee oversees progress and ensures the plan matches your actual income and expenses.

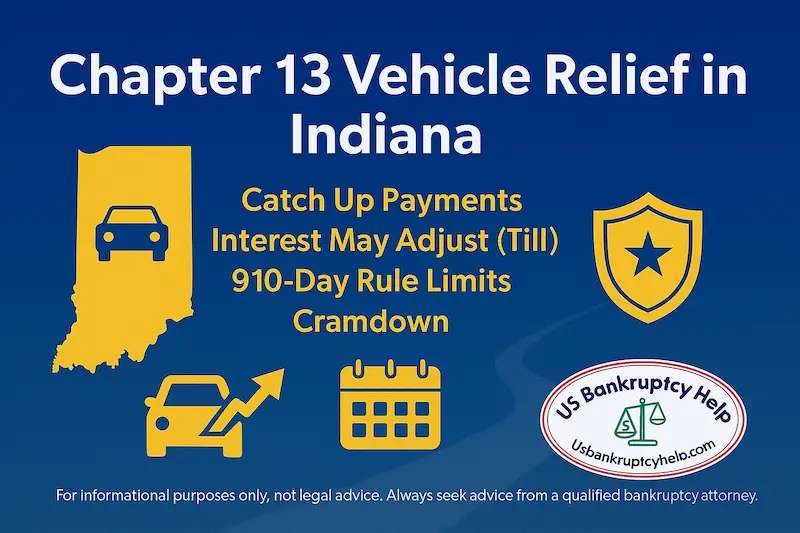

- Save Your Home: Cure past-due mortgage payments over time while you maintain current monthly payments (“cure and maintain”).

- Stabilize Your Vehicle: Catch up missed payments and often lower interest; note the 910-day rule limits cramdown on newer purchases.

- Control Unsecured Debt: Credit cards and medical bills are paid based on your budget and any non-exempt equity; eligible balances can be discharged at the end.

- Protect Co-Signers: The co-debtor stay can shield consumer co-obligors while you work the plan.

Indiana specifics matter: the state exemption scheme helps set the minimum your plan must pay unsecured creditors (the “best-interests” test). Under Indiana Code § 34-55-10-2, exemptions protect portions of your residence and other property; the more your assets are exempt, the lower that floor—so more of your cash can focus on curing arrears and staying current.

If you’re weighing filing chapter 13 in Indiana, the bottom line is simple: you keep working, keep your essentials, and use the court’s structure to get back on track—one payment at a time.

What Is Chapter 13 Bankruptcy in Indiana?

At its core, Chapter 13 bankruptcy in Indiana is a court-supervised repayment plan. You file, collections pause, and you propose one affordable monthly payment that a standing trustee distributes while you keep essential assets and steady your budget.

What makes it different is the math: your plan runs three or five years (based on median-income rules), and you commit projected disposable income during that time. The court confirms only plans you can realistically afford, and unsecured creditors must receive at least the value of any non-exempt property (the “best-interests” test).

In practice, bankruptcy chapter 13 Indiana shines when you need time to catch up: you can cure mortgage arrears while maintaining ongoing payments, reorganize vehicles (often with a lower interest rate under Till, with the 910-day rule limiting cramdown on newer purchases), and channel what’s left to unsecured debt—with eligible balances discharged at the finish line.

- Immediate Breathing Room: The automatic stay stops foreclosures, repossessions, and garnishments so you can stabilize.

- One Predictable Payment: A single monthly plan payment replaces scattered due dates and collection pressure.

- First Payment Comes Fast: Your initial plan payment is due shortly after filing, keeping momentum while the court reviews your plan.

- Co-Debtor Protection: A separate stay can shield a consumer co-signer while you work the plan.

- Indiana Angle: State exemptions help set the minimum paid to unsecured creditors; stronger protection for your property generally lowers that floor.

Indiana In Practice: Your first plan payment is due within 30 days of filing (11 U.S.C. § 1326(a)(1)). Many Southern District 341 meetings are conducted by Zoom. Standing trustees in the Northern and Southern Districts receive and distribute your single monthly payment (wage orders are common after confirmation). Your plan’s minimum payout to unsecured creditors depends on non-exempt equity under Indiana’s exemption scheme — see Indiana Code § 34-55-10-2, and check current dollar amounts posted by the state. To determine whether your plan is three or five years, compare your income to the median on the U.S. Trustee Means Testing page. For trustee contact/payment info, see the official Indiana chapter 13 trustee listings.

If you’re filing chapter 13 bankruptcy in Indiana to stop a foreclosure, end a garnishment, or keep a necessary vehicle, this chapter converts crisis into a structured, court-approved path forward—one payment at a time. If you’re filing chapter 13 in Indiana primarily to cure a default and protect key assets, you’re looking in the right place.

Eligibility Requirements for Chapter 13 Bankruptcy in Indiana

To qualify for Chapter 13, you must be an individual (including a sole proprietor) with regular income and stay within the chapter’s debt limits. If you’re filing chapter 13 bankruptcy in Indiana, the court will also look for proof you’ve met key federal prerequisites like recent credit counseling and tax-return filing.

- Individual With Regular Income: Chapter 13 is for people (wage earners, self-employed, sole proprietors)—not corporations or LLCs.

- Current Debt Limits (§ 109(e)): Your noncontingent, liquidated debts must be under the current caps (separate limits for secured and unsecured; adjusted every three years). See court notices on the April 1, 2025 update and federal adjustments.

- Credit Counseling (last 180 days): Complete a course from an approved provider before you file, with rare statutory exceptions.

- Tax Returns (§ 1308): You must have filed all returns for the four tax years ending before your case; if not, the trustee can hold the 341 meeting open briefly to let you file.

- No Recent 180-Day Bar (§ 109(g)): If a prior case was dismissed for willful noncompliance/absence—or you voluntarily dismissed after a stay-relief motion—you may have to wait 180 days to refile.

- Domestic Support & Ongoing Duties: To confirm and ultimately discharge, you must stay current on post-petition domestic support obligations and meet ongoing filing/payment requirements.

Indiana In Practice: Eligibility is federal, but your plan mechanics are local. Many Southern District 341 meetings run by Zoom, and standing trustees in the Northern and Southern Districts administer your single monthly payment (wage orders are common after confirmation). You’ll compare your household income to the Indiana median on the U.S. Trustee Means Testing page to determine a 3- or 5-year plan (applicable commitment period).

Helpful references: U.S. Courts: Chapter 13 Basics · Nov 1, 2025 means-testing tables · Tax-return rule (§ 1308) · 2025 federal dollar adjustments (incl. § 109(e))

The Chapter 13 Bankruptcy Process: Step-by-Step Guide

This is not a DIY guide. Chapter 13 is technical and deadline-driven—anyone considering it should consult an experienced Indiana bankruptcy attorney. The outline below shows how filing chapter 13 bankruptcy in Indiana typically proceeds; your attorney will tailor it to your district, division, trustee, and budget.

- Pre-Filing: Complete credit counseling (within 180 days), collect pay stubs/tax returns, and draft your petition, schedules, and plan.

- File the Case: Filing triggers the automatic stay (pausing foreclosures, repossessions, and garnishments). If the plan isn’t filed the same day, it’s usually due shortly after.

- Start Paying: Your first plan payment is typically due within 30 days of filing—don’t wait for confirmation.

- 341 Meeting of Creditors: You’ll answer questions under oath from the trustee; creditors may appear and ask limited questions.

- Confirmation: The court reviews feasibility (your budget), the best-interests test, and compliance with chapter 13 requirements before approving (confirming) your plan.

- Make Ongoing Payments: Continue monthly plan payments (wage orders are common) and keep direct-pay obligations (like mortgage) current.

- Complete & Discharge: After making all required payments and finishing debtor-education, the court enters a discharge of eligible debts.

Indiana In Practice: Indiana has two bankruptcy districts—Northern and Southern—with multiple divisions (e.g., Hammond, South Bend, Fort Wayne; Indianapolis, Evansville, New Albany, Terre Haute). 341 meeting formats and logistics can vary by division and trustee (many Southern District 341s are conducted remotely). Standing chapter 13 trustees receive and distribute your single monthly payment; some use wage orders and payment lockboxes. For court locations, divisions, and trustee contacts, see our Indiana courts hub: Indiana Bankruptcy Courts & Trustees.

Step 1: Credit Counseling and Pre-Filing Requirements

Before filing, complete a court-approved credit-counseling course (certificate valid for 180 days). Gather recent pay stubs, tax returns (last 4 years), bank statements, and a full list of debts, assets, income, and expenses.

- Course completion certificate

- Income proof & tax returns

- Draft budget showing plan feasibility

Step 2: Filing Your Petition and Required Documents

Filing opens your case and activates the automatic stay. You’ll submit the petition, schedules, statement of financial affairs, and a proposed plan. If the plan isn’t filed with the petition, it’s typically due shortly thereafter by local rule/practice.

- Petition, schedules, SOFA

- Chapter 13 plan (or filed promptly after)

- Pay stubs and tax documents as required

Step 3: The Automatic Stay and What It Means

The stay halts most collection: foreclosure sales pause, garnishments stop, and repossessions must cease. Some proceedings (e.g., criminal, certain domestic support actions) are carved out by law.

- Stops foreclosure and vehicle repossession

- Pauses wage garnishments and collection suits

- Protects co-signers on consumer debts via the co-debtor stay

Step 4: Creating and Submitting Your Repayment Plan

Your plan proposes how you’ll cure arrears and pay secured, priority, and unsecured claims over 3–5 years. The amount to unsecured creditors depends on your disposable income and non-exempt equity (the best-interests test).

- Cure-and-maintain for mortgages

- Vehicle arrears + potential interest rate adjustment

- Priority debts (e.g., certain taxes, support) paid in full

Step 5: The Role of the Chapter 13 Trustee

The trustee reviews feasibility and compliance, conducts your 341 meeting, and disburses your monthly plan payment to creditors after confirmation. Expect document requests and follow-ups—answer promptly.

- Reviews plan & budget

- Runs the 341 meeting

- Distributes payments; monitors ongoing compliance

Step 6: The 341 Meeting of Creditors

You’ll attend (often remotely, depending on division/trustee). Bring ID and proof of Social Security number. The trustee verifies your information; creditors may ask brief questions. It’s not a court hearing—no judge is present.

- Bring government ID + SSN proof

- Answer questions under oath

- Provide any documents the trustee requests

Step 7: Plan Confirmation and Making Payments

After objections (if any) are resolved, the judge decides whether to confirm your plan. You must keep making monthly plan payments (your first payment is typically due within 30 days of filing) and stay current on direct-pay obligations like your mortgage.

- Resolve trustee/creditor objections

- Wage orders are common post-confirmation

- Keep mortgage/insurance/taxes current

Step 8: Completing the Plan and Receiving a Discharge

When you finish all payments and required courses, the court grants a discharge of eligible debts. You may need to certify domestic-support compliance and complete a financial-management course before discharge.

- Complete debtor-education (financial management)

- Certify domestic-support obligation status

- Receive discharge of eligible unsecured debts

Key Benefits of Filing Chapter 13 Bankruptcy in Indiana

Chapter 13 gives you time and structure to fix what’s behind while keeping essential assets. For many Hoosiers, it’s the most reliable way to stop a foreclosure, stabilize a vehicle, and control unsecured debt under court supervision.

- Stop Foreclosure & Cure Arrears: Pause the sale, resume regular payments, and repay the past-due balance over time (“cure and maintain”).

- Protect Transportation: Catch up missed car payments; interest often adjusts under Till; the 910-day rule limits cramdown on newer purchases.

- Shield Co-Signers: A separate co-debtor stay can protect a consumer co-obligor while your plan is active.

- Right-Size Unsecured Debt: Pay what your budget and non-exempt equity require; eligible balances can be discharged at completion.

- Predictable Path: One monthly payment, trustee oversight, and a confirmation order that keeps everyone accountable.

- Indiana-Specific Edge: Indiana’s exemption scheme can lower the “best-interests” floor, directing more cash to curing arrears instead of unsecured claims.

Need court locations, divisions, or trustee contact details? Visit our Indiana Bankruptcy Courts & Trustees page for district/division info and practical logistics.

Explore Our Indiana Bankruptcy Guides

Potential Drawbacks and Risks of Chapter 13 Bankruptcy

Chapter 13 is powerful—but it isn’t painless. Before filing chapter 13 in Indiana, weigh these trade-offs so you go in with eyes open.

- Credit Impact: A chapter 13 notation can appear on your credit report for up to 7 years. You can rebuild during the case, but new credit will be tighter early on.

- Multi-Year Commitment: Plans run 3–5 years. The court expects consistent income, timely plan payments, and current post-petition obligations (mortgage, car insurance, taxes, support).

- Payment Pressure & Dismissal Risk: Missed plan payments can trigger trustee motions to dismiss or modify. If the case is dismissed, collections restart and any paused foreclosure/repossession can resume.

- Budget Scrutiny: You must commit projected disposable income and document changes. Windfalls (bonuses, settlements) may need to be disclosed and partly committed to the plan.

- Limited Autonomy During Case: New loans, selling or refinancing a home, or replacing a vehicle often requires trustee and/or court approval.

- Not All Debts Discharge: Domestic support, many recent taxes, most student loans (absent undue hardship), criminal fines/restitution, and some fraudulent debts usually survive discharge.

- Liens Can Survive: A discharge wipes personal liability, but valid liens (e.g., mortgages) generally remain unless paid or avoided through the case.

- Costs & Trustee Fee: There’s a $313 filing fee, and a standing trustee takes a small percentage from plan payments. Attorney fees are often paid through the plan (reducing upfront cost, but increasing monthly outlay).

- Indiana Practice Notes: Wage orders are common after confirmation; many trustees expect prompt delivery of tax returns each year and may require turnover of part of tax refunds to the plan (depends on your budget/plan terms).

- Repeat-Filer Limits: If you had a recent dismissal, the automatic stay may be limited or not go into effect without a court order (special timing rules apply).

Bottom line: Chapter 13 trades short-term flexibility for long-term stability. If your primary goals are to save a home, stabilize a vehicle, and structure debt under court protection, the trade can be worth it—with guidance from an experienced Indiana bankruptcy attorney.

How Indiana Exemptions Affect Your Chapter 13 Plan Payment

In chapter 13, exemptions don’t decide what you “lose”—they help set the minimum your plan must pay to unsecured creditors under the “best-interests of creditors” test (11 U.S.C. § 1325(a)(4)). In plain English: your plan must pay at least as much to unsecureds as a hypothetical chapter 7 would pay from your non-exempt equity.

- Value → Subtract Liens → Subtract Exemptions = Non-Exempt Equity: That number becomes the floor your plan must return to unsecured creditors (spread over 3–5 years).

- Indiana’s Scheme Controls the Floor: Indiana exemptions (see Ind. Code § 34-55-10-2) protect portions of your residence and other property; stronger protection = lower unsecured floor.

- Joint Filers: When both spouses own the asset and file together, many Indiana exemption amounts can be doubled—often reducing (or eliminating) non-exempt equity.

- Vehicles in Practice: Indiana doesn’t have a separate “car” exemption—most debtors cover equity with the wildcard or by accounting for the lien—so your vehicle’s equity can influence the floor.

- Retirement Accounts: Qualified retirement funds are generally protected by federal law and usually don’t factor into non-exempt equity for this test.

- Two Tests, One Plan: Your unsecured payout must satisfy both the best-interests floor (exemptions) and the disposable-income test (budget). Your confirmed plan will meet the higher of the two.

Quick Illustration: If a car is worth $12,000 with a $8,500 loan and you can exempt $3,500, the non-exempt equity is about $0. If the same car had only a $6,000 loan and $3,500 in applicable exemption, roughly $2,500 would be non-exempt—so your plan would need to return at least $2,500 to the unsecured pool (before trustee/admin costs), even if your budget is tight.

Want the full exemption list and current amounts? We’ll publish a dedicated Indiana exemptions guide soon and link it here. For court logistics and trustee contacts, visit our Indiana Bankruptcy Courts & Trustees page.

Chapter 13 vs. Chapter 7 Bankruptcy in Indiana

Deciding between chapters comes down to goals, budget, and timing. Below is a quick, practical comparison. For the deep dive, see our Indiana chapter 7 guide and the national Chapter 7 vs. Chapter 13 comparison.

- Speed: Chapter 7 is typically faster (months), while chapter 13 runs 3–5 years but lets you catch up on past-due secured debts inside a court-approved plan.

- Homes & Cars: Chapter 13 can cure and maintain a mortgage and reorganize a vehicle (interest often adjusts; 910-day rule limits cramdown). In chapter 7, you usually keep secured assets only if you’re current or can get current (e.g., reaffirmation/redemption).

- Unsecured Debt: Both chapters can discharge qualifying unsecured debts. In chapter 13, the payout to unsecured creditors is driven by your budget and any non-exempt equity (best-interests test).

- Income & Eligibility: Chapter 13 requires steady income to fund the plan. Chapter 7 uses a means test and other eligibility rules to determine if you qualify.

- Collections: Both trigger the automatic stay. Chapter 13 also provides a co-debtor stay on many consumer debts while your plan is active.

- Control vs. Fresh Start Speed: Choose chapter 13 when you need court structure to save a home/car and spread catch-up costs; choose chapter 7 when you need a faster reset and don’t need to cure long-term arrears.

Want a chapter-by-chapter walkthrough and Indiana specifics? Start with the Indiana chapter 7 guide or compare scenarios in our national guide.

Costs and Fees Associated with Filing Chapter 13 Bankruptcy in Indiana

Chapter 13 costs more than chapter 7 because it’s a multi-year case with ongoing administration. Expect a court filing fee, a trustee percentage, and attorney’s fees that reflect the plan’s complexity and the work required during and after confirmation.

- Court Filing Fee: $313 (payable at filing; installment plans are sometimes allowed).

- Attorney’s Fees (Typical Ranges): Many firms quote a base or “presumptive/no-look” fee that covers standard chapter 13 tasks through confirmation, with additional fees for extra work. Practical ranges often land around $3,500–$6,500+ for standard cases, and can climb higher ($7,500–$12,000+ over the life of the case) when issues stack up. Some attorneys bill hourly (commonly a few hundred dollars per hour) instead of, or in addition to, a base fee.

- How Fees Are Paid: In many Indiana cases, most attorney’s fees are paid through the plan (reducing upfront cost but increasing the monthly plan payment). Your retainer/down payment varies by firm.

- Trustee Percentage: The standing trustee takes a small statutory percentage from plan payments (set by the U.S. Trustee Program); this is built into your plan math.

- Required Courses: Credit counseling (pre-file) and debtor education (pre-discharge) typically cost about $20–$60 each with approved providers.

What Drives Fees Up (Common in Real Cases)

- Creditor Objections: Plan feasibility, valuation disputes, interest rate fights (Till), and “best-interests” challenges all add attorney time.

- Motions to Lift Stay: Mortgage or vehicle lenders frequently file stay-relief motions for payment defaults—responding/settling these is extra work.

- Self-Employed Debtors: Expect added documentation (e.g., business operating reports until confirmation), profit/loss analysis, and tax coordination.

- Post-Confirmation Events: Income changes, new expenses, tax refunds/turnover issues, plan payment adjustments, plan modifications, or cured-and-maintain monitoring.

- Litigation/Adversaries: Lien strips/avoids, dischargeability disputes, or contested claim objections require separate time and, sometimes, separate fee approval.

- Asset/Valuation Work: Appraisals, vehicle valuations, or business valuations can add third-party costs and attorney time.

Indiana Practice Notes

- Many chapter 13 attorneys in Indiana structure fees so most are paid through the plan, with additional fees approved by the court for extra work (plan mods, objections, stay-relief responses, etc.).

- Trustee payment percentages are applied to your plan payments automatically; your attorney can show how this affects the total you must pay in.

- Check local guidance for your division and trustee regarding “presumptive/no-look” fee guidelines and payment logistics on our Indiana Bankruptcy Courts & Trustees page.

Bottom line: chapter 13 fees are case-specific. A straightforward wage-earner case with a single mortgage cure is very different from a self-employed debtor with fluctuating income, multiple vehicles, creditor objections, and post-confirmation plan changes. Discuss likely scenarios—and how extra work is billed—with your Indiana bankruptcy attorney before filing.

Life During and After Chapter 13 Bankruptcy

Chapter 13 is a marathon, not a sprint. Day to day, your job is simple: make the plan payment on time, keep direct-pay obligations current (like your mortgage and insurance), and promptly respond to trustee requests. Do that, and the process works.

- Monthly Plan Payment: Pay on time, every time (wage orders are common after confirmation). If income changes, talk to your attorney about a plan modification before you fall behind.

- Direct-Pay Essentials: Keep mortgage, rent, car insurance, taxes, and support obligations current—missed post-petition payments can trigger stay-relief or dismissal.

- Documents & Updates: Expect to provide pay stubs/tax returns annually and report major changes (job, household size, new debts/claims). Some plans require partial turnover of tax refunds—ask how your plan handles refunds.

- No Big Moves Without Approval: New loans, refinancing, selling a home, or replacing a vehicle usually requires trustee and/or court approval. Coordinate with your attorney first.

- Stay Organized: Keep a folder with trustee letters, payment proofs, mortgage statements, and insurance declarations; it saves headaches when questions arise.

After you complete all required payments and the financial-management course, the court enters a discharge of eligible debts. Here’s how to use that fresh start:

- Verify the Finish Line: Save your discharge order, final trustee report, and any plan-completion certifications (e.g., domestic support statement). Keep them forever.

- Check Credit Reports: Pull Experian/Equifax/TransUnion and dispute obvious errors (e.g., balances that should show $0 after discharge, duplicate tradelines). A chapter 13 notation can remain up to 7 years.

- Rebuild Intentionally (Months 1–12): Use on-time payments across 3–5 open tradelines to rebuild: one secured credit card, one credit-builder loan, and one low-limit retail card can be enough—keep utilization under ~10% and pay in full.

- Protect the Budget: Build a small emergency fund first; then automate on-time payments. Avoid “fee-stacked” products and predatory offers post-discharge.

- Right-Size Insurance & Withholding: Keeping continuous auto/home coverage protects assets and satisfies lender requirements; correct tax withholding to reduce surprises.

- Plan Ahead for Big Purchases: Mortgage or auto lenders may want 12–24 months of clean history; rate shop carefully and avoid multiple hard pulls.

Bottom line: success in chapter 13 is about consistency and communication. If something changes—income, expenses, a lender issue—loop in your Indiana bankruptcy attorney early so you can adjust the plan rather than risk dismissal.

How Chapter 13 Bankruptcy Affects Your Credit and Future Finances

Chapter 13 places a public-record notation on your credit report (typically up to 7 years), but that doesn’t doom your score. In fact, many debtors finish a successful plan with decent credit because they’ve built 3–5 years of on-time payment history, stabilized debt, and avoided new delinquencies. For many Hoosiers, filing chapter 13 bankruptcy in Indiana marks the real turning point toward stronger credit and financial stability.

- At Filing: Expect an initial score dip as past-due accounts update and the case is reported. The automatic stay stops new negatives from piling on (no new charge-offs/garnishments).

- During the Plan: On-time plan payments (often via wage order) + staying current on mortgage/auto/insurance can add months and years of positive history. Missed post-petition payments hurt—communicate early if income changes.

- At Discharge: Most remaining eligible unsecured balances are zeroed out, improving utilization and DTI—both help scores rebound.

A Simple, Proven Rebuild Playbook

- Months 0–3: Pull all three credit reports; fix identity errors and obvious inaccuracies. Freeze reports to block fraud; unfreeze only when applying.

- Months 1–6: Open 1 secured card and (optionally) 1 credit-builder loan; keep utilization under ~10% and pay in full monthly.

- Months 6–12: Add one small retail/prime card if needed for mix; never carry balances for “credit building.” Keep on-time payments across 2–3 tradelines.

- Months 12–24: Consider a modest auto refinance or purchase only if it improves terms; rate-shop within a tight window and avoid multiple hard pulls.

- After 24 Months: Mortgage lenders often want 12–24 months of clean history post-discharge. Maintain low utilization, stable income, and a small emergency fund.

- Ongoing Hygiene: Set autopay for minimums, calendar due dates, and keep utilization low. Avoid “credit repair” schemes—use direct disputes for real errors only.

Key takeaways: the credit notation matters, but behavior matters more. Consistent on-time payments, low utilization, and a steady budget can put you in “fair to good” territory surprisingly fast—and many people exit chapter 13 with credit that’s already on a healthy upward climb.

Frequently Asked Questions About Chapter 13 Bankruptcy in Indiana

How long does a chapter 13 take in Indiana?

Most plans run 3–5 years. The length (applicable commitment period) depends on your income vs. Indiana median and other confirmation factors.

In Indiana, when is my first chapter 13 plan payment due?

Usually within 30 days of filing—don’t wait for confirmation (see 11 U.S.C. § 1326(a)(1)). Wage orders are common in Indiana once the plan is confirmed.

What happens to my debts in an Indiana chapter 13?

Secured arrears (home/car) can be cured over time; priority debts (like certain taxes/support) must be paid in full; unsecured debts are paid based on your budget and any non-exempt equity, with eligible balances discharged at completion.

Can I keep my home and car in chapter 13 in Indiana?

Often, yes. You can “cure and maintain” a mortgage (11 U.S.C. § 1322(b)(5)) and reorganize a vehicle (interest often adjusts under Till; the 910-day rule limits cramdown on newer purchases).

What if I miss chapter 13 plan payments in Indiana?

The trustee may move to dismiss or modify the plan. If dismissal occurs, collections can resume. Tell your attorney early if income changes—modifying the plan is better than falling behind.

Do I need an Indiana bankruptcy attorney to file chapter 13?

This is not a DIY process. Chapter 13 is technical and deadline-driven; consult an experienced Indiana bankruptcy attorney.

How do Indiana exemptions affect my chapter 13 payment?

Exemptions help set the minimum your plan must pay to unsecured creditors under the “best-interests” test (11 U.S.C. § 1325(a)(4)). Indiana’s scheme can lower that floor, keeping more cash focused on curing arrears.

Are co-signers protected in an Indiana chapter 13?

Often, yes—the co-debtor stay can protect a consumer co-obligor while your plan is active (11 U.S.C. § 1301).

Can I convert to chapter 7 from chapter 13 in Indiana?

Usually, yes, if you qualify and it aligns with your goals. For the deep dive, see our Chapter 7 vs. Chapter 13 guide and our Indiana chapter 7 guide.

In Indiana chapter 13, do I have to turn over tax refunds to the trustee?

It depends on your plan terms, budget, and trustee expectations. Some plans require partial refund turnover—ask your attorney how your division handles it.

What about credit—does chapter 13 ruin it in Indiana?

A chapter 13 notation can remain up to 7 years, but many filers finish with decent credit due to years of on-time payments and stabilized balances. Smart rebuild steps can accelerate recovery.

How are 341 meetings handled in Indiana chapter 13 cases?

You’ll attend (often remotely, depending on division/trustee). Bring ID and proof of SSN. For district/division logistics and trustee contacts, see Indiana Bankruptcy Courts & Trustees.

Chapter 13 Bankruptcy Lawyer in Indiana

Working with the right chapter 13 bankruptcy lawyer in Indiana can make all the difference. Chapter 13 is technical, deadline-driven, and filled with moving parts—local trustee expectations, plan modifications, objections, and post-confirmation events. An experienced attorney knows how to navigate those issues and keep your case on track.

Look for an attorney who regularly practices in your district and understands how the local standing trustees operate. Indiana has both Northern and Southern District bankruptcy courts, each with its own divisions, trustees, and local procedures. A lawyer familiar with those details can save you time, stress, and money.

When choosing your Indiana bankruptcy lawyer, consider:

- Experience With Chapter 13 Cases: Attorneys who routinely handle wage-earner plans understand the local trustees’ documentation requirements, plan language, and confirmation expectations.

- Knowledge of Indiana Exemptions: The state exemption scheme (Ind. Code § 34-55-10-2) affects how your plan is structured and how much unsecured creditors receive.

- Communication & Accessibility: You’ll need a lawyer who answers questions quickly, keeps you updated, and explains each step clearly.

- Ongoing Representation: Chapter 13 lasts several years. Choose someone committed to supporting you through confirmation, plan completion, and discharge.

Most Indiana bankruptcy firms offer a free or low-cost consultation—use it to ask about experience, fees, and what services are covered after confirmation. The right attorney will give you a realistic picture of your case, your payment plan, and your path to discharge.

Need help locating the courts or trustee offices? Visit our Indiana Bankruptcy Courts & Trustees page for districts, divisions, and contact information.

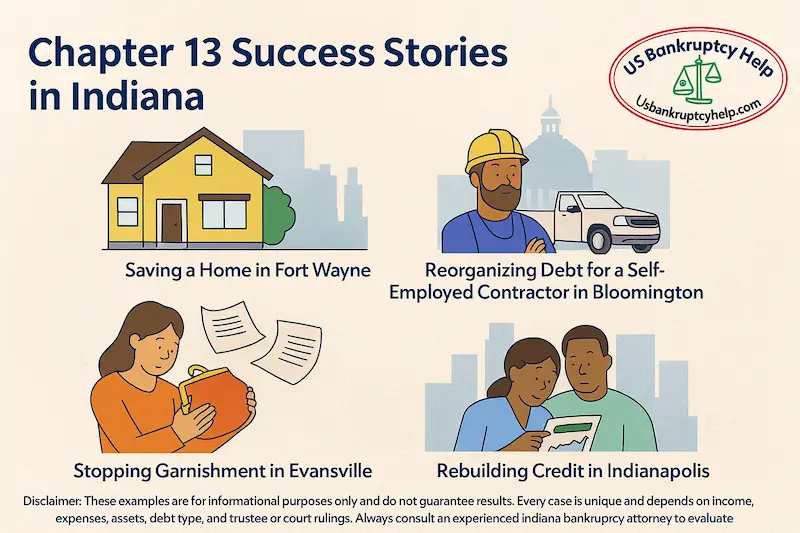

Chapter 13 Success Stories in Indiana

Chapter 13 isn’t just a theory—it works in practice for thousands of Hoosiers every year. The following examples show how everyday people across Indiana have used Chapter 13 to protect their homes, cars, and financial futures. Names and details are adjusted for privacy, but these are based on common real-world outcomes.

- Saving a Home in Fort Wayne: After a medical crisis, a family fell nearly a year behind on their mortgage. Chapter 13 stopped the foreclosure sale two days before the deadline, allowing them to repay $12,000 in arrears over 48 months while keeping the home.

- Reorganizing Debt for a Self-Employed Contractor in Bloomington: A small business owner faced tax debt and multiple vehicle loans. Through Chapter 13, he caught up on payroll taxes, restructured his truck loan with a lower interest rate, and finished his plan with a discharge of $40,000 in unsecured debt.

- Stopping Garnishment in Evansville: A single parent earning hourly wages had 25% of each paycheck garnished. Chapter 13 halted the garnishment immediately, lowered overall debt payments, and allowed her to budget for rent and childcare again.

- Rebuilding Credit in Indianapolis: A couple emerging from high-interest payday loans used Chapter 13 to consolidate their payments into one affordable plan. By making on-time payments for five years, their credit scores rose from the low 500s to the mid-600s by discharge, and they qualified for an FHA mortgage within 18 months.

Disclaimer: These examples are for informational purposes only and do not guarantee results. Every case is unique and depends on income, expenses, assets, debt type, and trustee or court rulings. Always consult an experienced Indiana bankruptcy attorney to evaluate your specific circumstances.

The common thread in these success stories is consistency—making plan payments on time, staying current on new obligations, and communicating early with your attorney. Chapter 13 gives you structure, protection, and a clear finish line—and countless Hoosiers have proven that it works.

Alternatives to Chapter 13 Bankruptcy in Indiana

Chapter 13 isn’t the only path. The right choice depends on goals (save a home/car vs. wipe out debt fast), budget, credit profile, and lawsuit risk. Here are common alternatives—what they do, their limits, and when they make sense in Indiana.

- Chapter 7 (Straightforward Fresh Start): Faster and usually less expensive than chapter 13; great for heavy unsecured debt when you’re not trying to cure a mortgage or car arrears. Compare in our Chapter 7 vs. Chapter 13 guide and the Indiana chapter 7 guide.

- Debt Management Plan (DMP) via Nonprofit Credit Counseling: One monthly payment to a 501(c)(3) agency; they seek interest-rate reductions and fee waivers. Limits: No court protection—lawsuits, garnishments, and secured creditors (mortgage/car) are not forced to cooperate.

- Consolidation Loan: Replaces multiple debts with one loan (often lower rate/longer term). Limits: Requires qualifying credit/income; moving unsecured debt to secured (e.g., home equity) puts collateral at risk; no stay—lawsuits can continue.

- Debt Settlement (Negotiated Reductions): Set aside money and settle for less than owed. Limits: No stay—creditors can sue; late fees/interest accrue; forgiven balances may be taxable (Form 1099-C), and credit damage can be significant.

- Mortgage/Auto Loss-Mitigation: Apply directly for loan modification, forbearance, or deferment. Limits: Voluntary; the lender can say no. If you need to force a cure over time, chapter 13 is built for that.

- “Do Nothing” / Wait-and-See: Sometimes used for small debts or if you’re judgment-proof. Limits: Indiana creditors can still sue, garnish wages, or levy non-exempt assets once they have a judgment; interest keeps running.

- Business/Specialty Chapters: Sole proprietors with complex operations or higher debt might consider small-business reorganization instead of chapter 13 (ask counsel what fits your facts).

Reality check: Alternatives that don’t involve the court lack an automatic stay. That means no forced pause on foreclosures, repossessions, or garnishments, and co-signers remain exposed. If your top priority is saving a home or car by curing arrears over time, chapter 13 is often the only tool with enough leverage.

This overview isn’t a DIY roadmap—talk with an experienced Indiana bankruptcy attorney about your budget, lawsuit exposure, tax angles (like 1099-C on settlements), and whether a three- to five-year plan or a faster chapter 7 better meets your goals.

Is Chapter 13 Bankruptcy Right for You?

Filing chapter 13 bankruptcy in Indiana isn’t a decision to rush—it’s a strategy to regain balance. The process demands discipline, but it also delivers structure, protection, and a real chance to rebuild. For many Hoosiers, it’s the difference between losing a home and keeping it, or between endless collections and a predictable path forward.

Chapter 13 works best for people with steady income who need time to catch up—those facing foreclosure, vehicle repossession, or unmanageable arrears. If that sounds familiar, this chapter may be the lifeline that fits your situation.

Every case is unique, and local procedures vary between Indiana’s Northern and Southern Districts. Before filing, talk with an experienced Indiana bankruptcy attorney about your goals, assets, and budget. A lawyer familiar with the trustees and courts can show you exactly how a plan would look in your district and what to expect along the way.

Whether you file or not, understanding your options puts you back in control—and that’s the first step toward financial stability and a genuine fresh start.

Explore Our Indiana Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin