Understanding Chapter 7 Bankruptcy in Indiana

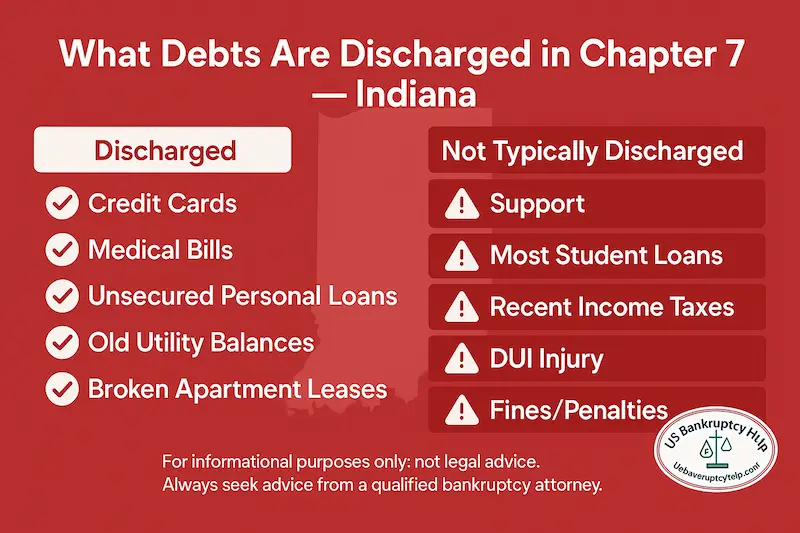

If you’re dealing with nonstop calls, past-due notices, or the fear of a garnishment or lawsuit, you’re not alone. Chapter 7 bankruptcy in Indiana is a federal court process that may help by pausing most collection activity through the automatic stay and, for eligible filers, eliminating many unsecured debts (like credit cards, medical bills, and personal loans) at the end of the case. What you can keep often comes down to Indiana exemptions, and eligibility often starts with the means test using Indiana median income figures—both of which we link to official sources on this page so you can verify details for your filing date.

- Exemption system: Indiana uses Indiana exemptions to protect certain property in a Chapter 7 case (with key references like Indiana Code § 34-55-10-2 and related adjustments like 750 IAC 1-1-1).

- Indiana median income snapshot: Jump to the Indiana median income table (based on the official U.S. Trustee figures).

- Where you file: Indiana cases are filed in the Northern or Southern District. Jump to Where You File in Indiana for court links and district guidance.

- State resources: Start at the Indiana bankruptcy hub for related state guides and updates.

- National guide (deeper overview): For the full federal process overview, see our Chapter 7 guide.

What’s Different in Indiana for Chapter 7

If you’re considering Chapter 7 in Indiana, the most helpful “Indiana-specific” pieces are practical: what property protections apply, which median income numbers the means test uses, and which court handles your case. This section keeps the focus on those items and points you to primary sources you can verify.

- Property protection depends on Indiana exemptions. Exemptions are the rules that determine what property is protected in a Chapter 7 case. For a regularly updated, plain-English overview, use our Indiana exemptions guide. For the underlying legal references this page cites, you can cross-check Indiana Code § 34-55-10-2 and the periodic amount tables referenced at 750 IAC 1-1-1.

- The “means test” uses Indiana median income figures from the U.S. Trustee. The median income table changes over time, so we link to the official source and show the current snapshot on this page. Jump to Indiana median income snapshot and verify numbers against the U.S. Trustee median income table.

- Where you file is Indiana-specific (Northern vs. Southern District). Your filing district affects where case notices come from and where your 341 meeting information is posted. We collect direct court resources (including 341 schedules and trustee lists) in Where You File in Indiana.

- People-first note on reliability: Costs, timelines, and “what you keep” depend on your facts (income, assets, equity, and recent transactions). This page avoids promising outcomes. When a number or rule matters, we prioritize official sources (U.S. Trustee Program and court sites) so you can confirm details for your filing date.

- If you want the broader federal overview: The steps and legal standards are primarily federal. For a deeper explanation of the overall process (without Indiana-only details), see our Chapter 7 guide.

Indiana Median Income Snapshot

If you’re trying to figure out whether Chapter 7 is even on the table, this is usually the first place people start. The means test looks at your household incomeover the last six months, then compares it to the Indiana medianfor your household size. These numbers change over time, so we show a snapshot here and link to the official source so you can double-check it for your filing date.

| Household Size | Annual Median Income (USD) |

|---|---|

| 1 | $62,808 |

| 2 | $79,884 |

| 3 | $93,175 |

| 4 | $112,691 |

| Add $11,100 for each person over 4. | |

Effective for cases filed on or after November 1, 2025. Source: UST Median Family Income by Family Size.

How to Read This Without Getting Lost

- Use the last 6 months (not last year): The means test starts with your most recent six months of household income, then “annualizes” it (turns it into a yearly number).

- Household size is a common sticking point: People often aren’t sure who counts. If you financially support someone, that can matter—use care and be consistent with your real situation.

- If you’re under the median: Many filers clear the first income screen of the means test.

- If you’re over the median: That does not automatically mean you “don’t qualify.” The next step typically looks at allowed expenses to see what (if any) disposable income is left.

- Reliable check: If you’re doing a quick estimate, verify the table at the official U.S. Trustee link above—especially if you’re close to the line.

For a step-by-step explanation of the means test (and what “allowed expenses” refers to), see our Chapter 7 guide.

Exemptions in Chapter 7 in Indiana

One of the biggest worries people have is, “Will I lose everything?” In many Indiana Chapter 7 cases, people are able to keep the things they need because exemptions protect certain property up to specific limits. Exemptions are about what’s protected— not about “gaming the system”—and they’re a normal, built-in part of how Chapter 7 works.

If you want the most detailed, regularly updated breakdown (with categories and limits), start here: Indiana bankruptcy exemptions.

What Exemptions Do (Plain-English)

- They protect equity, not the “item.” For example, the question is usually how much equity you have in a car or home (value minus loans), not just whether you own one.

- They help determine whether a case is “no-asset.” If everything fits within the available exemptions (or isn’t worth administering), there may be nothing to distribute to creditors.

- They’re claimed on your schedules. Listing property accurately (and valuing it realistically) is a key part of using exemptions correctly.

Primary Sources (So You Can Verify)

- Indiana’s core exemptions statute referenced on this page: Indiana Code § 34-55-10-2

- Administrative amount tables referenced for updates: 750 IAC 1-1-1

- Court explainer (useful plain-English cross-check): Southern District of Indiana — What Are Exemptions?

How to Get Your Numbers Ready (Quick Checklist)

- Make a simple property list: home, vehicles, bank accounts, retirement, household goods, and anything you’re unsure about.

- Estimate equity realistically: what it could sell for today minus what you still owe.

- Use the exemptions guide to cross-check categories: it’s an easier starting point than reading statutes first.

Next, we’ll zoom in on the two items people worry about most—home and car—and how to think about them in an Indiana Chapter 7 case.

Indiana Home & Car Reality Check for Chapter 7

When people ask “Will I lose my house or car?”, the most reliable way to answer is to slow down and look at equity, liens, and the Indiana exemption rules—not rumors or rough guesses. This section is a practical worksheet you can use before you talk to anyone.

Step 1: Calculate Equity the Simple Way

- Home equity: (What it could sell for today) − (mortgage payoff) − (other liens, if any).

- Car equity: (Current value) − (auto loan payoff, if any).

- Why this is more reliable: Indiana exemptions generally protect equity up to certain limits—so equity is the number that drives risk.

Step 2: Match Your Equity to Indiana’s Exemption Sources

Indiana exemptions are the starting point for “what you keep” discussions. If you want to verify the underlying rules, the page cites these Indiana sources:

- Indiana Code (exemptions statute referenced here): Indiana Code § 34-55-10-2

- Administrative updates referenced for exemption dollar amounts: 750 IAC 1-1-1

- Plain-English overview with links and updates: Indiana exemptions guide

Step 3: Home and Car “Keep It” Checklist

- Home: Write down the mortgage payoff, any second mortgage/HELOC, and any other liens you know about. Those lien amounts change the equity number fast.

- Car: Get the payoff quote (if financed) and a realistic value estimate. If the car is paid off, equity is basically the value.

- Payments matter: If you want to keep collateral that has a loan attached, being current (or having a plan for catching up) is often as important as the exemption question.

- If your equity is “close”: That’s the moment to stop guessing—small valuation changes can affect risk. Use the statute and the updated amounts (links above) to confirm what applies.

Next, we’ll lay out where you file in Indiana (Northern vs. Southern District) and provide direct court links so you can verify trustee/341 meeting information from official sources.

Where You File in Indiana

Indiana Chapter 7 cases are filed in federal bankruptcy court. Indiana is split into two districts—the Northern District of Indiana and the Southern District of Indiana. Which one applies depends on where you’ve been living (venue rules). If you’re unsure, the most reliable approach is to confirm using the court’s own pages and your address history.

Northern District of Indiana (Court Resources)

- 341 meeting locations/info (court site): Northern District — 341 Meeting Locations/Info

- Trustee list (court site): Northern District — List of Case Trustees

Southern District of Indiana (Court Resources)

- Court calendars / 341 calendar (court site): Southern District — Court Calendars

- 341 meeting Zoom/info (court site): Southern District — Section 341 Meeting Info

U.S. Trustee Program (Trustee Roster)

- Chapter 7 panel trustee roster (search by district/state): UST — Chapter 7 Panel Trustee Roster

If You’re Trying to Decide Which District Applies

- Use your address history: venue is based on where you’ve lived recently, not where you “prefer” to file.

- Verify with official sources: when in doubt, use the court’s own pages above (and any district/division guidance they publish).

Next, we’ll give a short process overview (focused on what matters most) and link out to the national guide for the full federal step-by-step.

What to Expect Next (A Simple Chapter 7 Roadmap)

If you’re feeling overwhelmed, it helps to think of Chapter 7 as a short, structured checklist: gather documents, file, attend a brief 341 meeting, complete two courses, and then wait for the discharge timeline to run (assuming there are no follow-up requests). This is a broad overview only—not legal advice.

The Core Steps (Indiana)

- Before filing: collect the basics—income proof, tax returns, bank statements, a full creditor list, and a property list.

- Income screen: compare your last six months of household income to the Indiana median income table and verify figures at the U.S. Trustee source.

- File in the correct district: Northern or Southern District of Indiana. Use Where You File in Indiana to find court links and 341 meeting information.

- Attend the 341 meeting:a short trustee-run Q&A about your paperwork. Each district posts logistics online (links are in the section above).

- Complete the two required courses: credit counseling (before filing) and debtor education (after filing) from approved providers. Official lists: Credit Counseling and Debtor Education.

- Use exemptions correctly: exemptions help define what property is protected. Start with our Indiana exemptions guide and verify the cited statute reference Indiana Code § 34-55-10-2.

Next Link (Full Federal Walkthrough)

For a deeper step-by-step explanation of the federal process (forms, timelines, discharge rules, and common questions), see our Chapter 7 guide.

Indiana-Specific FAQs

These FAQs focus on the Indiana-specific items people ask about most—median income numbers, Indiana exemptions, and which court resources to trust. This is general information only, not legal advice.

Do I qualify if my income is below Indiana’s median?

Often, being below the Indiana median income for your household size clears the first income screen of the means test. You can compare your numbers to the Indiana median income snapshot on this page and verify against the official U.S. Trustee median income table. If you’re above the median, that doesn’t automatically mean you can’t file—there’s typically a second step that considers allowed expenses.

Will I lose my house or car in Chapter 7?

Many Indiana filers keep their home and vehicle, but it depends on equity and how Indiana’s exemptions apply. A reliable starting point is to calculate equity (value minus loans/liens), then review the Indiana exemptions resources and cited statute reference: Indiana Code § 34-55-10-2. Our plain-English hub is here: Indiana exemptions guide.

Which court handles my Indiana case?

Indiana is split into the Northern District and Southern District bankruptcy courts. If you’re unsure which applies, use the Where You File in Indiana section above for official court links (including 341 meeting information) and verify based on your address history.

Where do I find reliable 341 meeting info and trustee lists?

Use official court pages for your district. This page links directly to Northern and Southern District 341 resources and trustee lists in the Where You File in Indiana section, plus the U.S. Trustee Program’s panel trustee roster.

Do I have to take classes?

Yes—credit counseling before filing and debtor education after filing are typically required. The most reliable way to find approved providers is the U.S. Trustee Program lists: Approved Credit Counseling Agencies and Approved Debtor Education Providers.

Where can I get a bigger-picture overview without Indiana-only details?

For a step-by-step explanation of the overall federal process (and common terms you’ll see in court notices), see our Chapter 7 guide.

Next Steps and Options

If you’re deciding what to do next, the most helpful move is usually to gather a few facts you can verify (income, equity, district) and then use trusted sources. The links below are meant to keep you oriented—Indiana-specific where it matters, and national where the rules are mostly federal.

Indiana Guides (State-Specific)

Explore Our Indiana Bankruptcy Guides

National Guides (Bigger Picture)

Explore Some of Our National Bankruptcy Guides

Quick “Do This Next” Checklist

- Check your household income against the Indiana median income snapshot and verify the table at the U.S. Trustee link on that section.

- List your home and car values, loan payoffs, and liens so you can estimate equity before you make decisions.

- Use the Indiana exemptions guide and cross-check the statute reference this page cites (Indiana Code § 34-55-10-2) if you want the primary source.

- Confirm which district applies using Where You File in Indiana and the court links provided there.

National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin