Understanding Michigan Chapter 13 Bankruptcy Process

At a Glance: Michigan Chapter 13 Bankruptcy

- Immediate relief: The automatic stay typically pauses foreclosures, repossessions, garnishments, and most lawsuits after filing (11 U.S.C. § 362).

- One predictable payment for 36–60 months: Court-supervised plan with confirmation and disposable-income tests (11 U.S.C. § 1325;U.S. Courts).

- Debt limits (eligibility): Unsecured $526,700 • Secured $1,580,125 (noncontingent, liquidated) for cases filed Apr 1, 2025–Mar 31, 2028 (11 U.S.C. § 109(e)).

- Keep what matters: Cure mortgage arrears in the plan; restructure vehicle interest/term—note the 910-day rule on newer personal-use vehicles (see the “hanging paragraph” to § 1325(a)). For details on car treatment, read our vehicle cramdown guide.

- Co-debtor stay (consumer debts): Can protect a co-signer while the plan provides for the account (11 U.S.C. § 1301).

- Required courses: Pre-filing credit counseling & post-filing debtor education from approved providers (DOJ/UST).

- Michigan venue matters: File in the Eastern or Western District; local procedures and standing trustees shape timelines (e.g., conduit vs. direct mortgage) (E.D. Mich. /W.D. Mich.).

- What the plan must pay: Trustee/admin + priority debts (taxes/support) + secured claims you’re keeping; unsecured debts get what your confirmed budget and legal tests require (U.S. Courts).

- Keys to success: Realistic budget, on-time trustee payments (payroll deduction helps), current home/auto insurance, and fast responses to trustee requests.

- Exemptions set your floor: Your plan must at least match non-exempt value. See Michigan bankruptcy exemptions.

If your budget has started to feel like a game of whack-a-mole, Michigan Chapter 13 bankruptcy gives you room to breathe. It’s a court-supervised plan—usually 36 to 60 months—that pauses most collections right away and routes payments through a trustee so you can stabilize housing, transportation, and family finances.

Chapter 13 fits people with steady income who want to keep what matters and catch up over time. In Michigan, that typically means proving current income, keeping insurance in force on your home and car, and making on-time plan payments (many filers use payroll deduction so nothing slips through the cracks). For many filers, Michigan chapter 13 is the path that protects key assets while you reorganize and catch up over time.

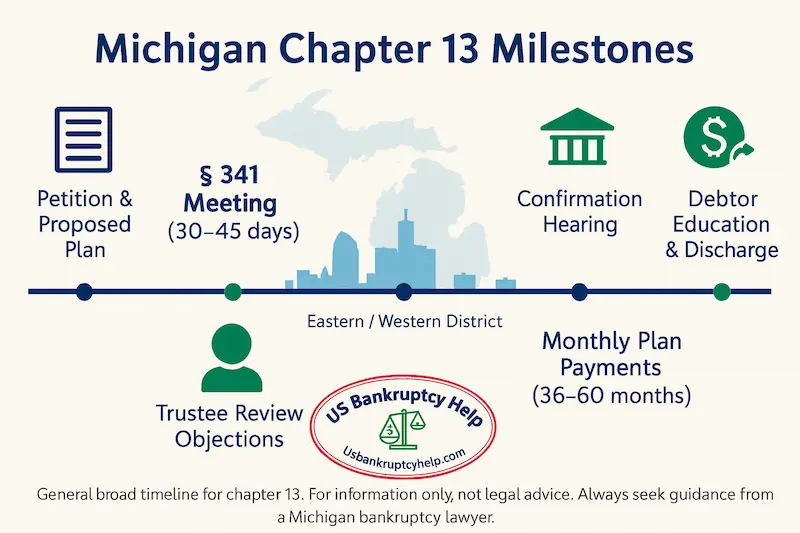

Filing starts with a petition and a proposed repayment plan. Michigan cases are filed in either the Eastern District of Michigan (Detroit, Flint, Bay City) or the Western District of Michigan (Grand Rapids, Kalamazoo, Lansing, Marquette). Your division determines where your §341 meeting happens, which standing trustee is assigned, and the local procedures you’ll follow.

Once filed, the automatic stay usually stops foreclosure activity, repossessions, wage garnishments, and most lawsuits. A standing Chapter 13 trustee reviews your plan, collects monthly payments, and disburses funds to creditors. You’ll complete credit counseling before filing and a debtor-education course before discharge—both are standard parts of the process.

Why many people choose Michigan bankruptcy chapter 13: you can cure missed mortgage payments while you keep the house, restructure a car loan to a reasonable rate (subject to the 910-day rule for newer vehicles), pay recent taxes over time, and often protect a co-signer on consumer debts through the co-debtor stay. The goal is forward momentum—not perfection on day one.

What Is Michigan Chapter 13 Bankruptcy?

Picture a single, predictable payment that calms the chaos. Michigan chapter 13 is a 36–60 month, court-supervised plan that lets you reorganize debt while you keep the essentials you live in and drive. Instead of a fire sale, it’s a reset: catch up on arrears, pay what your budget can truly support, and protect the things that matter.

Who Chapter 13 Is Built For

It’s made for people with steady income who want to keep a home or vehicle, bring accounts current over time, and stop juggling ten different due dates. In plain language, chapter 13 bankruptcy Michigan is how you stabilize cash flow and buy time to get whole again.

Core Protections You Get

- • Automatic stay: Most collections (foreclosures, repossessions, garnishments, lawsuits) pause while you are in your plan.

- • One payment, many problems solved: You send a single monthly payment to the standing Chapter 13 trustee; the trustee pays creditors by court order.

- • Co-debtor stay (consumer debts): Your plan can shield a cosigner on qualifying consumer accounts while payments are being made.

What Chapter 13 Can Accomplish

- • Cure mortgage arrears: Spread missed payments across the plan while you resume the regular mortgage payment.

- • Restructure vehicle debt: Bring an unreasonable APR down to a fair rate, or even reduce principal to fair market value through a vehicle cram down. Pay vehicle arrears through your plan, and come out of chapter 13 with a fully paid off vehicle.

- • Handle priority debts:Stop the bleeding of penalties and fees, and pay back taxes that are not eligible for discharge.

- • Right-size unsecured debt: Credit cards and medical bills often receive only what your confirmed budget allows; any eligible remainder can be discharged at completion.

Michigan Chapter 13 Bankruptcy Examples: Real Outcomes

- • Detroit homeowner (mortgage arrears): Five months behind? The plan spreads arrears over 36–60 months while regular payments resume, pausing foreclosure activity after filing.

- • Grand Rapids auto (high-APR reset): An 18% car loan is reduced to a reasonable rate and amortized over the plan; the 910-day rule can limit cramdown on newer personal-use vehicles.

- • Lansing priority taxes: Recent Michigan/IRS income taxes (priority) are paid in full through the plan on a fixed schedule; general unsecured cards receive a budget-based dividend.

- • Ann Arbor co-signer protection: A parent who co-signed a consumer card is protected by the co-debtor stay while the plan provides for that account.

- • Flint medical debt relief: Large hospital balances move into the unsecured pool; you pay what the budget supports and discharge the eligible remainder at the finish line.

What It Isn’t

- • Not a quick wipeout like Michigan chapter 7— chapter 13 plans run three to five years and require on-time payments.

- • Not one-size-fits-all—your plan must meet feasibility, good-faith, best-interest, and disposable-income tests at confirmation.

- • Not a guarantee to keep every asset—outcomes depend on values, liens, and your Michigan exemption strategy.

If you’re filing bankruptcy chapter 13 Michigan, think of it as a steady, court-guided path to protect key assets, regain control of cash flow, and finish with a discharge—without rehashing the step-by-step mechanics we’ll cover later.

Related Guide

- Chapter 7 vs. Chapter 13: Which One Fits Your Situation? — A quick, plain-English comparison to help you choose the right chapter before you file.

How Chapter 13 Bankruptcy Works in Michigan

What to expect next: After you file in your Michigan division, a standing Chapter 13 trustee is appointed, your first plan payment comes due in ~30 days, and your case moves toward a §341 meeting and plan confirmation on the court’s calendar. Think “steady runway,” not “instant fix.”

Michigan Chapter 13 Trustees (Official Listings)

Use the official trustee pages linked below for the most current addresses, phone numbers, payment portals, and document-delivery instructions.

| Jurisdiction / Division | Trustee | Official Page | Notes |

|---|---|---|---|

| Eastern District — Detroit Division | Krispen S. Carroll (Standing Trustee) | det13ksc.com | Official Detroit Division trustee site. |

| Eastern District — Detroit Division | Tammy L. Terry (Standing Trustee) | det13.net | Online payment info and appearance guidance. |

| Eastern District — Detroit Division | David Wm. Ruskin (Standing Trustee) | det13.com | Official Detroit Division trustee site. |

| Eastern District — Flint Division | Melissa A. Caouette (Standing Trustee) | flint13.com | Flint Division trustee portal. |

| Eastern District — Bay City Division | Thomas W. McDonald, Jr. (Standing Trustee) | 13Network (Saginaw Trustee Portal) · Court’s Trustee List | Bay City/Saginaw office; official resources. |

| Western District — Grand Rapids / Lansing / Traverse City | Elizabeth Clark (Standing Trustee) | rodgersch13.com | Official site for the Grand Rapids-based trustee. |

| Western District — Kalamazoo / Marquette | Kurt A. Steinke (Standing Trustee) | chpt13.com | Official site for the Kalamazoo-based trustee. |

Verified with the Eastern & Western District of Michigan trustee pages and the U.S. Trustee Program directory. Please confirm details on the linked official sites. Last updated: Oct 29, 2025

Before you file: complete a short credit-counseling course from an approved provider and gather today’s numbers—pay stubs (typically last 60 days), your most recent tax return, mortgage and car statements, bank statements, and proof of insurance. Real, current documents = a plan the trustee can actually confirm.

When you file: the automatic stay usually pauses foreclosures, repossessions, garnishments, and most lawsuits. A Michigan Chapter 13 trustee reviews your plan, collects one monthly payment, and pays creditors under a court order. Your first plan payment is due ~30 days after filing—even before confirmation—so many filers use payroll deduction to stay perfectly on time.

Key Milestones You’ll See

- • Petition & proposed plan: Filed with accurate income/expense schedules and a full creditor list.

- • § 341 meeting (about 30–45 days): Quick Q&A with the trustee (no judge). Bring government ID, SSN proof, and any items requested on your notice.

- • Trustee review & objections: Requests for clarification are normal—respond fast to keep your confirmation date on track.

- • Confirmation hearing: The court decides if your plan meets feasibility, good-faith, best-interest, and disposable-income tests. Many issues resolve by consent once you supply support.

Michigan-Specific Practicalities

- • Adequate protection for vehicles: Early plan dollars often earmark car payments so you keep driving while the case is pending.

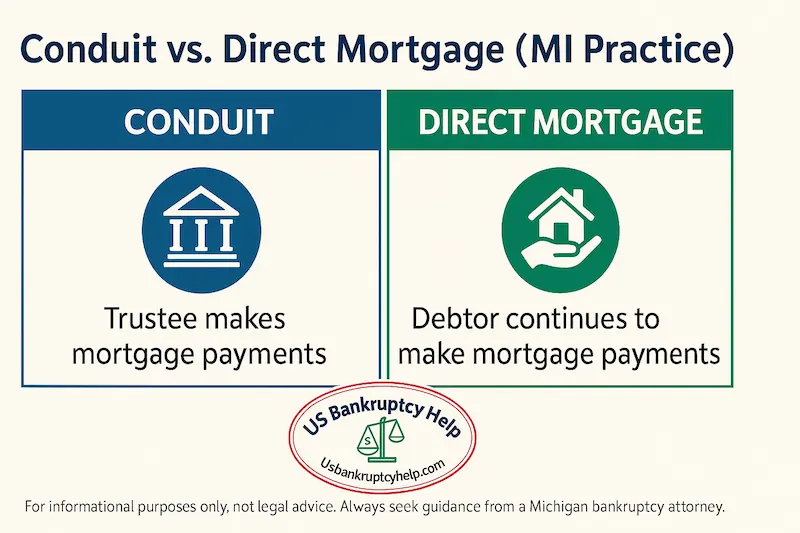

- • Mortgage handling (conduit vs. direct): Some divisions prefer the trustee to pay the ongoing mortgage when you’re curing arrears; others allow you to pay it directly—follow your trustee’s local guidance.

- • Insurance is non-negotiable: Keep homeowners and auto coverage active; lapses can trigger stay relief and asset risk.

- • Documentation discipline: Michigan trustees commonly ask for pay stubs, tax returns, bank statements, and proof of income changes. Timely uploads prevent continuances.

What Success Looks Like

- • 3–5 year runway: You catch up on mortgage arrears, right-size a car loan, and pay priority taxes on schedule with one predictable payment.

- • Budget-based treatment: Unsecured debts (cards, medical) get exactly what your confirmed budget supports; any eligible remainder can be discharged at completion.

- • Stay current, finish strong: On-time trustee payments + on-time direct obligations (like an ongoing mortgage, if not conduit) = a clean path to discharge.

Bottom line: Michigan chapter 13 works best when the plan is realistic, documents are complete, and you communicate quickly with the trustee’s office. That combination turns the stay into real breathing room—and a confirmed plan into a reliable roadmap to the finish line.

Eligibility Requirements for Michigan Chapter 13

Chapter 13 works when two things are true: you have steady income and a feasible plan. In real life, that means your budget can support one predictable payment each month while you stay current on housing, transportation, insurance, and taxes.

Quick Michigan Checklist

- • Regular income: W-2 wages, self-employment, pension/retirement, benefits—or a mix—so long as it’s reliable.

- • Debt within legal limits: Your total noncontingent, liquidated debts must fit Chapter 13 caps (see current figures below).

- • Up-to-date documentation: Recent pay stubs, last tax return, bank/mortgage/auto statements, and proof of insurance.

- • Feasible plan: Numbers that actually work for 36–60 months—on paper and in your household budget.

Income & Feasibility (What the Court Looks For)

You don’t need perfect credit; you need a workable budget. Michigan trustees and judges zero in on whether the proposed payment is realistic after rent/mortgage, car, utilities, groceries, insurance, and taxes. Many filers choose payroll deduction so the trustee payment is automatic—less chance a busy month derails the case.

Debt Limits (Current Figures)

Chapter 13 eligibility includes federal caps under 11 U.S.C. §109(e). For cases filed April 1, 2025 – March 31, 2028, the limits are:

- • Unsecured debt: $526,700 (noncontingent, liquidated)

- • Secured debt: $1,580,125 (noncontingent, liquidated)

These amounts are measured on the day you file and adjust periodically. Always verify the current limits against the Code/UST guidance for your filing date.

Who Can File

- • Individuals and married couples (including sole proprietors). Corporations/LLCs do not file Chapter 13.

- • Michigan residents file in the Eastern or Western District based on residence; local trustee practices and division procedures apply.

Pre-Filing Requirements

- • Credit counseling: Complete a brief course from an approved provider within 180 days before filing; you’ll file the certificate with your petition.

- • Tax return readiness: Have your most recent return available; trustees commonly request it along with recent pay stubs and bank statements.

- • Insurance in force: Keep homeowners and auto coverage active—lapses can risk stay relief on collateral.

Bars & Common Tripwires

- • Recent dismissal: A case dismissed within the last 180 days for willful failure to appear/comply can temporarily bar refiling.

- • Unfiled returns: Missing tax returns can stall confirmation; file promptly if any are outstanding.

- • Unrealistic budgets: If pay stubs and bank statements don’t match the schedules, expect objections and delays.

Bottom line: If your income is steady and your debts fit within the current Chapter 13 limits, you’re likely eligible. A Michigan Chapter 13 attorney can confirm the caps for your filing date, run the feasibility math, and tailor a plan a local trustee can confirm.

Key Benefits of Filing Chapter 13 in Michigan

Instead of repeating the basics, here’s when Chapter 13 tends to be the right tool in Michigan—and the signals it may not be. Use this as a quick decision lens before you dig into the process sections below.

When Chapter 13 Is Usually the Better Fit

- • You’re behind on a mortgage and want to keep the home while curing arrears over 36–60 months.

- • Your auto loan math needs fixing: a high APR or short term threatens your budget, and you need a trustee-managed, court-approved reset (subject to the 910-day rule for newer personal-use vehicles).

- • Recent income taxes are due: priority taxes must be paid in full—Chapter 13 gives you a predictable schedule.

- • A co-signer needs protection: the co-debtor stay can shield a parent/partner on qualifying consumer debts while your plan pays.

- • Your budget works monthly but not all at once: one structured payment to the trustee is realistic; lump-sum settlements are not.

Green Flags for a Confirmable Plan

- • Reliable income and a documented budget that leaves room for a single plan payment.

- • Current insurance on home/vehicle; you can stay current on ongoing obligations after filing.

- • Docs ready: recent pay stubs, last tax return, mortgage/auto statements, and bank statements match your schedules.

Yellow Flags (Consider Another Path or Adjust)

- • Income is too variable to support a fixed monthly trustee payment.

- • Large non-exempt equity plus a tight budget makes plan feasibility tough without downsizing or concessions.

- • Recent case dismissal for missed appearances or orders—this can temporarily limit refiling and stay protections.

Bottom line: Chapter 13 in Michigan shines when you need time and structure to protect a home or car, pay priority debts, and keep a co-signer safe—and your numbers support one predictable monthly payment. If those boxes are checked, you’re looking at the right chapter.

Step-by-Step Guide to Filing Bankruptcy Chapter 13 Michigan

Note: The outline below is a high-level overview of Michigan chapter 13. Because this chapter is technical and time-sensitive—and local procedures differ by division—you’ll want guidance from an experienced Michigan bankruptcy attorney to prepare, file, and confirm a plan that actually works.

Think of Michigan chapter 13 as a short runway to get airborne: prep, file, stabilize, confirm, then cruise. Here’s the flow most filers actually experience—what happens, when it happens, and what to have in hand.

Pre-Filing: Prep for a Clean Launch

- • Credit counseling (required): Complete a brief course from an approved provider within 180 days before filing; you’ll file the certificate with your petition.

- • Document pack: Recent pay stubs (typically 60 days), last tax return, mortgage/auto/bank statements, insurance proof, and a full creditor list with balances and addresses.

- • Budget reality check: Build a plan payment that survives rent/mortgage, car, utilities, food, insurance, and taxes—on paper and in real life.

- • Pick payment method: Most Michigan filers use payroll deduction so the trustee payment goes out automatically each month.

Filing Day: Start the Case

- • Petition + proposed plan: File in the proper Michigan division (Eastern or Western). The case opens and your proposed plan is on record.

- • Automatic stay begins: Foreclosures, repossessions, garnishments, and most lawsuits typically pause.

- • Fees: Pay the court filing fee or request installments if eligible.

Early Case: Stabilize

- • Trustee assigned: A standing Chapter 13 trustee reviews your plan and requests standard documents.

- • First plan payment due: ~30 days after filing—even before confirmation. Make it on time (payroll deduction helps).

- • Vehicle “adequate protection”: Early plan dollars often earmark car payments so you keep driving while the case is pending.

341 Meeting & Confirmation Track

- • § 341 meeting (about 30–45 days): Brief Q&A with the trustee (no judge). Bring government ID, Social Security proof, and any items listed on your notice.

- • Trustee questions/objections: Clarifications are normal—respond quickly with pay stubs, bank statements, mortgage/auto details, or plan tweaks as requested.

- • Confirmation hearing: The court decides whether your plan meets good-faith, feasibility, best-interest, and disposable-income tests. Many issues resolve by consent once support is provided.

Life During the Plan

- • One predictable payment: You pay the trustee monthly; the trustee pays creditors by court order.

- • Stay current on “direct” bills: If your division allows you to pay the ongoing mortgage directly (non-conduit), never miss it.

- • Insurance is non-negotiable: Keep homeowners and auto coverage active; lapses can risk stay relief on collateral.

- • Report changes: If income or expenses shift, loop in your attorney promptly—plans can be modified when warranted.

Finish Line (Plan Completion)

- • Debtor-education course: Complete the second course before the end of your case to avoid discharge delays.

- • Discharge: After all required payments are made and certifications filed, eligible remaining unsecured balances can be discharged.

Michigan Tips That Save Headaches

- • Conduit vs. direct mortgage: Some divisions prefer conduit (trustee pays ongoing mortgage when you’re curing arrears); others allow direct pay. Follow your trustee’s local guidance.

- • Tax returns & pay stubs: Missing or stale documents delay confirmation—keep them current and upload promptly.

- • Plan realism beats ambition: A plan you can actually sustain for 36–60 months is what gets confirmed—and keeps you protected.

Key point: Filing gets you breathing room; confirmation turns that relief into a durable roadmap. Stay organized, pay on time, and communicate quickly with the trustee’s office, and Michigan chapter 13 does exactly what it’s built to do.

The Chapter 13 Repayment Plan Explained

Your Michigan chapter 13 plan is a simple promise on paper: one predictable payment each month that the trustee uses to pay what the law requires—no more, no less. Here’s what drives the numbers and what has to pass before the court will confirm it.

What Must Be Paid (In Order of Priority)

- • Trustee fees & approved attorney fees: Built into your monthly payment.

- • Priority debts: Recent income taxes and domestic support obligations are generally paid in full.

- • Secured claims you’re keeping: Cars and mortgages you retain are paid per the plan (interest and “adequate protection” rules apply; newer personal-use vehicles are affected by the 910-day rule).

- • Unsecured claims: Credit cards, medical bills, and similar debts receive what your budget and the legal tests require; any eligible remainder can be discharged at completion.

The Legal Tests Your Plan Must Pass

- • Feasibility: Can you actually afford the payment after normal living expenses?

- • Best-interest test: Unsecured creditors must receive at least what they’d get in a hypothetical chapter 7.

- • Disposable-income test: If a creditor or trustee objects, you must commit projected disposable income for the required term (usually 36–60 months).

- • Good faith & completeness: Honest schedules, realistic values, current tax returns/insurance, and consistent documents.

How the Monthly Payment Is Built

- • Income and expenses: W-2, self-employment, pensions/benefits vs. ordinary living costs (rent/mortgage, car, utilities, food, insurance, taxes).

- • Plan term: 36–60 months, based on income and case strategy.

- • Local practice details: In some Michigan divisions, ongoing mortgages are paid through the trustee when you’re curing arrears (conduit); others allow you to pay them directly. Follow your division’s guidance.

- • Payment mechanics: Many filers use payroll deduction so the trustee payment is always on time.

Modifications, Refunds & Finishing Strong

- • Plan modifications: Income/expense changes can justify increasing or reducing payments; tell your attorney early.

- • Tax refunds: Michigan trustees often have rules for refunds—some must be turned over or partially applied. Read your confirmation order.

- • Completion requirements: Make all payments, keep insurance in force, file required certifications, and complete debtor education to receive your discharge.

Plan Math at a Glance

| Debt Type | What the Plan Must Do | Common Michigan Notes | Where It Shows Up |

|---|---|---|---|

| Trustee Fees & Approved Attorney Fees | Paid inside the plan from your monthly payment. | Trustee percentage varies; attorney fees per local norms/approval. | Administrative section of plan |

| Priority Debts (recent taxes, Domestic Support Obligations (DSOs)) | Generally must be paid in full over the plan term. | Trustees often require current proof of filings; (DSOs) must remain current post-petition. | Priority claims section |

| Mortgage — Ongoing | Stay current on the ongoing payment (conduit or direct). | Some divisions use conduit (trustee pays ongoing when curing arrears); others allow direct pay. | Secured/ongoing mortgage section |

| Mortgage — Arrears | Cure pre-petition arrears over 36–60 months. | Follow local trustee guidance on escrow/fees; proof of insurance required. | Arrearage cure section |

| Vehicle Loans | Pay per plan; interest adjusted to a reasonable rate; early “adequate protection.” | The 910-day rule limits cramdown on newer personal-use vehicles. | Secured claims section |

| Unsecured Debts (cards, medical) | Receive only what your budget and legal tests require; eligible remainder may be discharged at completion. | Best-interest test: must pay at least what creditors would get in a hypothetical Chapter 7. | Unsecured pool/dividend section |

| Co-Signed Consumer Debts | Plan can provide for the account; co-debtor stay may protect the co-signer during the case. | Applies to qualifying consumer debts; stay can lift if the plan doesn’t adequately provide. | Designated claim treatment |

Notes: Details can differ by Michigan division and trustee (e.g., conduit mortgage policy, tax refund handling, document delivery). Always follow your confirmation order and trustee instructions.

In Summary: A confirmable plan isn’t about paying everything—it’s about paying the right things, in the right order, with numbers the court believes you can sustain for 36–60 months.

Common Challenges and How to Overcome Them

Chapter 13 is doable—but it’s a marathon, not a sprint. Here are the snags Michigan filers hit most often and the fixes that keep cases on track.

1) Staying Perfect on Payments

- • The challenge: A surprise expense (brakes, medical bill) collides with your trustee payment.

- • Fix it fast: Use payroll deduction so the trustee payment leaves automatically. Build a mini-buffer ($300–$600) in a separate account. If income changes, ask counsel about a plan modification before you miss a payment.

2) Mortgage Logistics (Conduit vs. Direct)

- • The challenge: In some MI divisions, ongoing mortgages are paid through the trustee when you’re curing arrears; in others you pay them directly—misses can trigger stay-relief motions.

- • Fix it fast: Follow your trustee’s local guidance exactly. If direct pay is allowed, set auto-pay for the regular mortgage and calendar the due date. Keep homeowners insurance current and escrow notices handy.

3) Vehicle Claims & the 910-Day Rule

- • The challenge: Expecting a cramdown on a newer personal-use vehicle (purchased <910 days before filing) or missing early “adequate protection” payments.

- • Fix it fast: Budget for adequate protection from month one. If the car is <910 days old, discuss interest reduction (not cramdown) and term stretching with counsel.

4) Documents Don’t Match the Schedules

- • The challenge: Pay stubs, bank statements, or tax returns conflict with the numbers in your plan—leading to trustee objections or continuances.

- • Fix it fast: Upload fresh stubs/bank statements promptly. If income varies (overtime, commissions), provide a short written explanation and averages; adjust the plan if needed.

5) Tax Returns & Refunds

- • The challenge: Missing returns stall confirmation; refunds may need to be turned over depending on your order.

- • Fix it fast: File any outstanding returns ASAP. Read your confirmation order—some MI trustees require all or part of refunds; plan accordingly with adjusted withholdings.

6) Insurance Lapses on Home or Vehicle

- • The challenge: A coverage lapse invites stay relief from the lender/servicer.

- • Fix it fast: Put policies on auto-pay and calendar renewal dates. Keep proof of insurance handy for the trustee and secured creditors.

7) Creditor or Trustee Objections

- • The challenge: Disputes over collateral value, plan feasibility, or best-interest/disposable-income tests.

- • Fix it fast: Respond within deadlines. Provide Kelley Blue Book/NADA printouts, payoff letters, appraisals, or budget support. Small plan tweaks often resolve objections by consent.

8) New Debt or Income Shifts During the Plan

- • The challenge: A job change, reduced hours, or an emergency expense hits mid-plan.

- • Fix it fast: Tell your attorney immediately. Consider a temporary suspension, plan modification, or adjusted withholding—don’t skip payments and hope for the best.

Red-to-Green Playbook (Quick Wins)

- • Payroll deduction for trustee payments

- • Auto-pay for ongoing mortgage (if direct) and insurance

- • Keep a 1-month mini-reserve for car/medical surprises

- • Upload requested docs within 48–72 hours

- • Review confirmation order—know the refund/insurance rules

Bottom line: Most Michigan chapter 13 setbacks are fixable—fast—when you pay on time, keep insurance current, reply to trustee requests quickly, and adjust the plan when life changes. The sooner you surface an issue, the smoother your case runs.

Michigan Chapter 13 Success Stories

Realistic examples; identifying details changed for privacy. Outcomes vary by facts and local practice.

Detroit Home Saved, Budget Stabilized

Five months behind on a mortgage, this Detroit family filed Michigan chapter 13. The plan cured arrears over 48 months while the ongoing payment resumed. With payroll deduction, trustee payments stayed perfect; foreclosure activity paused after filing, and the case confirmed on the first setting.

Grand Rapids Car Rework & Tax Plan

A high-APR auto loan was reduced to a reasonable rate and stretched over the plan; recent IRS/Michigan income taxes (priority) were placed on a fixed schedule. The trustee requested a small budget tweak; once provided, the plan confirmed and the driver kept the car.

Ann Arbor Co-Signer Protected

A parent co-signed a consumer card. The co-debtor stay protected them while the account was provided for inside the plan. With on-time trustee payments and current insurance, the case stayed on track to discharge.

Flint Medical Debt Under Control

Large hospital bills shifted into the unsecured pool. The plan paid exactly what the confirmed budget required; the eligible remainder is scheduled for discharge at completion, freeing cash flow for essentials.

What These Cases Had in Common

- • Realistic plan payment based on verified income and expenses

- • Payroll deduction for trustee payments; auto-pay on direct mortgage (if not conduit)

- • Current home/auto insurance and fast responses to trustee requests

- • Local practice alignment (conduit rules, tax refund handling) followed exactly

Note: Every case is unique. For a strategy tailored to your facts, speak with an experienced Michigan chapter 13 attorney.

Frequently Asked Questions About Michigan Bankruptcy Chapter 13

How long does a Michigan chapter 13 take?

Most cases run 36–60 months. The length depends on your income, plan design, and whether creditors or the trustee require a longer term to satisfy legal tests.

Can I keep my house in chapter 13?

Usually, yes. Chapter 13 lets you cure past-due mortgage payments over time while staying current on the ongoing payment. Some Michigan divisions require “conduit” (trustee pays ongoing mortgage when you’re curing arrears); others allow direct pay—follow your trustee’s local guidance.

What happens to my car loan?

You can restructure interest to a reasonable rate and stretch payments across the plan. The “910-day rule” limits cramdown on newer personal-use vehicles; if the car was purchased within ~2.5 years before filing, you typically must pay the full balance, not just the value.

How is my monthly plan payment calculated?

It’s based on your verified income, reasonable living expenses, plan length, and the amounts the law requires you to pay (trustee/attorney fees, priority taxes/support, secured claims you’re keeping). Unsecured debts receive the remainder required by the legal tests.

Do I have to pay all my credit cards and medical bills in full?

Not necessarily. In many Michigan cases, unsecured debts receive only what your confirmed budget and the legal tests require. Any eligible remainder can be discharged at completion.

When is my first payment due?

About 30 days after filing—before plan confirmation. Many filers use payroll deduction so the trustee payment is automatic and on time every month.

What if I can’t make a payment during the plan?

Tell your attorney immediately. Depending on the situation, you may request a short suspension, modify the plan, or adjust withholdings. Don’t simply skip a payment—misses can trigger dismissal or creditor action.

Will chapter 13 protect a co-signer?

Often, yes. The co-debtor stay can protect a co-signer on qualifying consumer debts while your plan provides for that account. If the plan doesn’t adequately protect the creditor, the stay can be lifted.

How are tax refunds handled in Michigan chapter 13?

It depends on your confirmation order and trustee policy. Some trustees require turning over all or part of refunds. Your attorney will tailor the plan and withholdings to match local practice.

Do I need to complete courses?

Yes. You must complete pre-filing credit counseling (within 180 days before filing) and a post-filing debtor-education course before discharge. Keep the certificates handy.

Will chapter 13 ruin my credit forever?

No. It appears for up to 7 years from filing, but scores can improve much sooner with on-time payments, low utilization on any new credit, and steady income. Many filers see progress within the first year after filing.

Can I move or change jobs during my plan?

Usually yes, but coordinate with your attorney and the trustee. A job change or relocation can affect payroll deduction, budget, and venue issues; your plan may need a small adjustment.

Is Michigan Chapter 13 the Right Move?

If your budget keeps playing whack-a-mole, Michigan chapter 13 can turn chaos into one predictable payment, protect what matters, and put past-due balances on a schedule the court will actually honor. It’s not magic—and it isn’t easy—but with the right plan, it’s a practical path to steady ground.

Success in chapter 13 comes from realism: numbers you can live with, documents that match your story, and fast follow-through with your trustee. A Michigan bankruptcy attorney can pressure-test your budget, apply the current §109(e) debt limits, and tailor a plan that fits local practice in your division.

Your Next Three Steps

- • Verify eligibility: Confirm the current Chapter 13 debt caps and make sure your totals fit for the date you plan to file.

- • Assemble today’s numbers: Recent pay stubs, last tax return, mortgage/auto/bank statements, insurance proof, and a complete creditor list.

- • Pressure-test the payment: Build a plan amount you can hit every month for 36–60 months (payroll deduction helps keep it perfect).

When you’re ready, have a short strategy call with a Michigan chapter 13 attorney. In 15–30 minutes you’ll know if the plan math works, what your trustee will expect, and how quickly you can move from “barely treading water” to a confirmed, court-approved roadmap.

Explore Our Michigan Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin