Understanding Michigan Bankruptcy Exemptions: A Guide

Michigan bankruptcy exemptions are your shield. Used well, they can protect home equity, a vehicle, everyday necessities, and retirement savings. Below, we map the rules, compare Michigan and federal options, and show how to maximize protection.

When people talk about “exemptions,” they mean the laws that decide what you’re allowed to keep—your home equity, car, household goods, retirement funds, and more—while you work through a bankruptcy case. In Michigan, you can choose between Michigan’s exemption set and the federal set, and that choice can meaningfully shape your outcome (see MCL 600.5451; 11 U.S.C. § 522(b)).

Michigan Bankruptcy Exemptions at a Glance

- Two Playbooks, One Choice: Michigan lets you elect either state or federal exemptions—whichever protects more of your assets.

- Homestead Protection: Michigan’s homestead exemption safeguards equity in your primary residence (subject to statutory caps and eligibility rules).

- Personal Property Coverage: Furniture, clothing, basic household goods, and tools of the trade have specific protections so you can maintain daily life.

- Vehicle + Wildcard: A car exemption helps you keep reliable transportation; the federal system adds a flexible wildcard to “top up” gaps.

- Retirement & Benefits: Most tax-advantaged retirement accounts and core public benefits are protected by statute.

- Petition-Date Math: Values and caps are applied as of your filing date; realistic used-market values matter.

- Per-Debtor Caps: Many limits apply per filer; in a joint case some protections can effectively double (facts/titling control).

- Domicile Rule: To use Michigan’s scheme you generally must have lived in Michigan for 730 days (2 years) before filing.

Key statutes: MCL 600.5451 (Michigan exemptions), 11 U.S.C. § 522, § 541, § 362. See the table below for current caps.

Because exemptions are the backbone of asset protection, selecting the right system (Michigan vs. federal) matters more than most realize. The “best” choice depends on the shape of your estate—home equity vs. vehicle equity, retirement balances, tools/equipment, and any unique assets you need to shield. We’ll walk through those trade-offs and cite the controlling law so you can make an informed, Michigan-specific decision. To be able to use the Michigan bankruptcy exemption scheme you must have lived in Michigan for at least 730 days (2 years).

Quick note on scope: this page focuses on exemptions. If you’re comparing how exemptions play inside a chapter 7 case—timelines, means test, trustee process—see our dedicated guide instead: Michigan chapter 7 guide. We’ll avoid repeating that material here to keep this page laser-focused on maximizing protection.

As with any statute-driven topic, figures and caps can change over time. We reference Michigan’s exemption statute (MCL 600.5451) and the federal Bankruptcy Code (including 11 U.S.C. § 522) throughout; always apply the most current amounts to your facts. When in doubt, professional guidance helps ensure you’re using the most favorable and up-to-date protections for your situation.

What Are the State of Michigan Bankruptcy Exemptions?

Michigan bankruptcy exemptions are the legal rules that let you keep certain property even after you file. In bankruptcy, almost everything you own initially becomes part of the “estate” (see 11 U.S.C. § 541), and exemptions are how you pull protected items back out (11 U.S.C. § 522).

How Michigan Chapter 7 Bankruptcy Exemptions Work

In chapter 7, exemptions are the line between what you keep and what may be administered by the trustee. If an asset is fully covered by an exemption, you typically keep it. If there’s non-exempt equity, the trustee can seek to administer that equity for creditors unless there’s a practical or legal reason not to. Exemptions are therefore the central tool for protecting home equity, a vehicle, tools, and household goods in a straight discharge case.

- Goal: Cover as much equity as possible with the best-fitting system (Michigan vs. federal).

- Non-exempt equity risk: Assets with value above the cap can be at risk of administration.

- Timing/valuation: Values and caps are applied as of the petition date; documentation helps.

- Lien avoidance (plain-English): In some situations you can ask the court to remove certain liens that block your exemption—typically a judgment lien or a non-purchase-money security interest in household goods, tools, or sometimes a vehicle—if that lien “impairs” (reduces) your exemption (see 11 U.S.C. § 522(f)). It’s limited and fact-specific, but when it applies, it can restore your exemption protection.

Quick example: If your car has $6,000 in equity and your chosen vehicle exemption covers $5,025, the $975 difference is “non-exempt.” The trustee can consider administering that value—unless there’s a practical or legal reason not to—or you resolve it another way (e.g., negotiate or redeem).

For even more info on chapter 7, visit our national chapter 7 article.

How Chapter 13 Bankruptcy Exemptions Work in Michigan

In chapter 13, you generally keep your assets and repay creditors over time through a plan. Exemptions still matter—just differently. They help set the plan’s minimum payout through the “best-interests of creditors” test: unsecured creditors must receive at least what they would have received in a hypothetical chapter 7. Non-exempt equity isn’t lost; it’s typically offset by paying that value over the plan term.

- Asset retention: Keep assets and address any non-exempt value via plan payments.

- Best-interests test: Plan must pay unsecured creditors at least the non-exempt amount they’d get in a chapter 7 case.

- Strategy: Picking Michigan vs. federal exemptions can lower the non-exempt total and, in turn, reduce the necessary plan payout.

- Practical tip: Accurate valuations (home, car, tools) are crucial—small differences can move plan feasibility. (Values and caps are measured as of the petition date.)

How to Read This Table

- Michigan vs. federal: You choose one system—you can’t mix and match. Pick the column that protects more of your assets.

- Per-debtor math: Several caps apply per filer. In a joint case, some protections can effectively double.

- Who gets which cap: Some Michigan amounts increase for seniors or people with disabilities—see the homestead row.

- Always current: Michigan amounts come from posted state sources; federal figures reflect the current Judicial Conference update.

| Category | Michigan (MCL 600.5451) — posted amounts (effective Apr 1, 2023) | Federal (11 U.S.C. § 522(d)) — as of Apr 1, 2025 |

|---|---|---|

| Homestead (Primary Residence) | $46,125 equity (standard); $69,200 if 65+ or disabled Source: Michigan Treasury notice (Apr 1, 2023 effective) | $31,575 equity (per debtor) — §522(d)(1) |

| Motor Vehicle | $4,250 equity in one vehicle | $5,025 equity in one vehicle — §522(d)(2) |

| Household Goods & Furnishings | Up to $700 per item, $4,625 aggregate (includes typical household goods; some jewelry often treated within this category) | Up to $800 per item, $16,850 aggregate — §522(d)(3) |

| Jewelry | Included within household goods limits above (no separate posted dollar cap) | $2,125 total — §522(d)(4) |

| Wildcard (Any Property) | No separate general wildcard in posted Michigan scheme | $1,675 + up to $15,800 of unused homestead — §522(d)(5) |

| Tools of the Trade | $3,075 | $3,175 — §522(d)(6) |

| Retirement Accounts | Generally protected for tax-qualified plans under MI law and federal non-bankruptcy law (no set dollar cap in many cases) | Generally protected (ERISA plans fully; IRAs subject to §522(n) cap); also §522(d)(12) / §522(b)(3)(C) |

| Public Benefits (e.g., Social Security) | Protected under Michigan and federal law | Protected under federal law (various provisions) |

Figures current as of Nov 1, 2025. Michigan amounts reflect posted values under MCL 600.5451; federal amounts reflect 11 U.S.C. § 522(d) (adjusted Apr 1, 2025). Always confirm current caps before filing.

Exemptions exist so you can preserve essentials—housing, transportation, basic household items, and retirement security—while you reset your finances. If you’re new to the topic and want a big-picture primer, start with our Michigan bankruptcy overview.

Michigan allows you to choose between the Michigan exemption scheme and the federal scheme, but you cannot mix and match. The election you make can meaningfully change your outcome (see MCL 600.5451; 11 U.S.C. § 522(b)).

Here’s what bankruptcy exemptions commonly protect:

- Equity in your primary residence (homestead protection subject to statutory caps)

- Motor vehicles and personal property needed for daily life

- Retirement accounts and pensions (often fully protected under federal and state law)

- Household goods and furnishings at reasonable values

- Tools of the trade you rely on to earn a living

Which system fits best depends on your household—home equity vs. vehicle equity, the value of your personal property, and your retirement balances. Throughout this guide we’ll compare Michigan and federal protections, cite the controlling statutes, and flag practical trade-offs so you can choose the stronger fit for your situation.

Michigan vs. Federal Bankruptcy Exemptions: Which Should You Choose?

Choosing between the Michigan and federal exemption systems isn’t about which one is “better” in the abstract—it’s about which one protects your mix of assets on the petition date. You must elect one system (no mixing), and in joint cases spouses generally have to use the same system. The right call can swing thousands of dollars of protected value.

For a broader walk-through on when you can file for bankruptcy and keep your house—covering both chapters with examples—see our national guide: Can You File for Bankruptcy and Keep Your House?

How the Choice Works

- One system per case: Elect either Michigan or federal exemptions—you can’t combine them (see 11 U.S.C. § 522(b); MCL 600.5451).

- Measured on the petition date: Caps and valuations lock in as of filing; careful, supportable values matter.

- Per-debtor math: Many caps apply per filer; in a joint case, some protections can effectively double.

- Domicile rule (moving states): If you recently moved, special look-back rules can affect which state’s system you’re allowed to use (11 U.S.C. § 522(b)(3)).

When Michigan Usually Wins

- Home-equity heavy households: Michigan’s homestead structure can be attractive for homeowners with meaningful equity (see MCL 600.5451).

- Michigan-specific categories: Your facts line up well with Michigan’s itemized protections for household goods, tools, and certain benefits under state law.

- Joint filing with a home focus: Two filers may leverage per-debtor homestead math depending on facts and titling.

When Federal Usually Wins

- Stronger vehicle coverage: The federal vehicle exemption is typically higher than Michigan’s posted amount.

- Wildcard flexibility: Federal §522(d)(5) lets you protect “odd-ball” assets or top up categories that are otherwise short on coverage.

- Renter / low home equity: If you don’t need a bigger homestead, the federal household-goods + wildcard combo is often more flexible overall.

Quick Scenario Guide

- Own a home with solid equity, modest car value: Michigan may edge out federal.

- No home equity, higher car value, a few valuables: Federal often wins (vehicle + wildcard).

- Tools/equipment for work: Compare the Michigan tools cap to federal §522(d)(6); then consider whether the federal wildcard can “top up.”

- Retirement heavy: Most tax-qualified retirement is protected under either system; the choice then turns on home/vehicle/household mix.

Fine Print (Worth Knowing)

- No mixing & matching: Once you elect a system, you’re generally bound to that system for all categories.

- Title & liens matter: How an asset is titled (solo, joint) and whether liens exist can change the analysis—especially for homes and vehicles.

- Numbers change: Both Michigan and federal amounts adjust periodically. Always apply the most current posted caps to your specific facts.

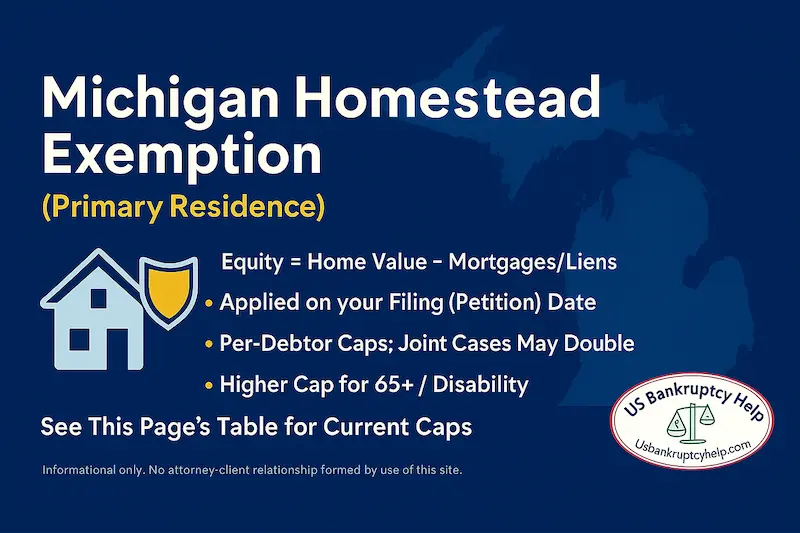

Michigan Bankruptcy Homestead Exemption

Michigan’s homestead exemption protects a portion of the equity in your primary residence so you aren’t forced to give up your home when you file. It applies in both chapter 7 and chapter 13, but it functions differently in each: in chapter 7 it can keep your home out of administration if equity is fully covered; in chapter 13 it helps lower the “non-exempt” number that would otherwise increase your plan payment. See MCL 600.5451 for the controlling statute and the current dollar caps listed in the table above.

Who Qualifies As a Homestead

- Primary residence: House, condo, or a manufactured/mobile home you actually occupy as your main home.

- Ownership + occupancy: You must have a legal interest and use it as your principal residence on the petition date.

- Michigan residence: The exemption is tied to Michigan law—domicile/look-back rules can apply if you recently moved (see 11 U.S.C. § 522(b)(3)).

How To Calculate Your Equity

- Start with value: Use a supportable fair-market value (recent appraisal/CMA, assessor data, comps).

- Subtract liens: First mortgage, HELOCs, property tax liens, and other consensual liens recorded on the home.

- Compare to the cap: If your equity is at or under the Michigan cap (see the table above), the equity is generally exempt.

- Per-debtor math: In a joint case, some protections can effectively double depending on titling and facts.

Special Enhancements & Edge Cases

- Senior/Disability enhancement: Michigan law provides a higher cap for filers who are 65+ or meet disability criteria (see the table and MCL 600.5451).

- Tenancy by the entirety (TBE): If spouses hold title as TBE and only one spouse files, creditor type matters. Michigan recognizes TBE, but the analysis in bankruptcy can be nuanced—facts and creditor mix drive outcomes.

- Mixed-use property: If part of the property is non-residential (e.g., rental or business use), courts can limit how much qualifies as homestead.

Documentation That Helps

- Proof of occupancy: Driver’s license address, voter registration, utility bills, homestead/property tax classification.

- Supportable value: Recent appraisal or CMA; photos and comps if needed.

- Clean lien picture: Current payoff statements for mortgages/HELOCs; recorded lien history if unsure.

Common Pitfalls

- Using the wrong cap: Amounts adjust periodically. Always use the current posted caps (see the table above).

- Overlooking co-owner interests: Titling (solo, joint, TBE) affects how much of the equity you can claim as your exemption.

- Underdocumented value: A weak valuation can create a dispute about “non-exempt” equity—document early.

Choosing between the Michigan and federal systems isn’t just a math exercise—it’s a strategy call that affects your home, timeline, and plan feasibility. A knowledgeable Michigan bankruptcy attorney can pressure-test valuations (appraisal vs. comps), verify titling (solo, joint, TBE), spot lien issues, apply the correct homestead cap, and confirm domicile/look-back rules so nothing gets missed. If you’re comparing your numbers to the table above, this is the moment to get a quick attorney review to make sure your filing fully leverages the protection you’re entitled to.

Personal Property Exemptions in Michigan

Personal property exemptions let you keep everyday essentials while you reset—think furniture, clothing, appliances, a workable computer, and the tools you need to earn a living. Michigan’s scheme defines categories and caps, and you can elect either the Michigan system or the federal system (you can’t mix). The right pick depends on your mix of household items, vehicle value, and whether you need the flexibility of a wildcard.

Household Goods and Personal Effects

Michigan’s personal property protections are designed to keep the basics in your home so life remains functional during and after the case. Typical covered items include:

- Reasonable furniture and household items (beds, tables, sofas, cookware)

- Clothing and personal belongings at everyday values

- Appliances necessary for daily living (refrigerator, washer/dryer, basic electronics)

Caps are applied to fair-market value (what an item would sell for used), not what you paid new. That matters: most household goods appraise far lower than purchase price, which helps coverage go farther.

Additional Personal Property Protections

Beyond core household goods, Michigan and federal law recognize categories that matter to work and daily life:

- Tools of the trade: Equipment and tools reasonably necessary for your occupation or trade.

- Books and educational materials: Reasonable value, especially where used for work or schooling.

- Modest jewelry and keepsakes at everyday values (see the table for how federal handles jewelry separately).

Choosing the federal system can add flexibility via the wildcard to “top up” items that run over a category cap; the Michigan system does not include a general wildcard. That’s a key reason renters or folks with higher-value personal items sometimes prefer the federal set.

How To Value Personal Property (So Your Exemptions Work)

- Use used-market value: Thrift/yard-sale/Craigslist pricing is closer to bankruptcy fair-market value than retail.

- Group where appropriate: Everyday dishes, linens, and smallwares can be valued as reasonable sets.

- Document simply: A quick spreadsheet with item, condition, and value; add a few comps or photos if something is borderline.

- Remember per-item vs. aggregate caps: Some systems cap both per-item and total—track each.

Lien Issues on Personal Property (Quick Plain-English)

If a creditor has a lien on personal items (for example, a judgment lien that attached to household goods or a non-purchase-money security interest in tools), that lien can “impair” your exemption. In limited scenarios, you may be able to ask the court to avoid that lien so your exemption counts the way the law intended (see 11 U.S.C. § 522(f)). It’s narrow and fact-specific, but it’s there when you need it.

Common Pitfalls (And Easy Fixes)

- Using retail prices: Overstating value can make items look non-exempt; use used-market numbers.

- Forgetting per-item limits: If a single item is near a per-item cap, consider whether the federal wildcard (if you elect federal) solves it.

- Skipping proof: A few photos and 2–3 comps for borderline items prevent disputes and speed reviews.

- Overlooking work gear: Don’t miss tools/equipment you actually use—those caps exist to keep you earning.

Mini Example

Example: You list a sofa ($150), dining set ($200), bed frames/mattresses ($350), everyday electronics ($250), and clothing ($250). Total $1,200 at used-market value. Under either system, that bundle typically fits within household-goods caps; if one item (say, a high-end tool) bumps a per-item limit, compare the Michigan tools cap to the federal tools cap and consider the federal wildcard.

Bottom line: match your facts to the table above, decide whether Michigan or the federal set fits your mix of items, and document values like a sensible seller would. If anything is close to a cap—or you have a few higher-value pieces—a quick attorney review can make sure your exemptions are maximized and undisputed.

Motor Vehicle Exemption in Michigan

Reliable transportation is essential in Michigan, and the law recognizes that. The motor vehicle exemption lets you protect equity in one car per filer up to the posted cap (see the table above). If your equity is fully covered, you generally keep the car in both chapter 7 and chapter 13.

How Vehicle Exemptions Work (and What To Watch)

- Per-debtor protection: The exemption applies per filer. In a joint case where both spouses are on title, protection can effectively double.

- Equity math: Equity = fair-market value (used-market) minus the loan payoff and other valid liens. If equity ≤ the cap, it’s typically exempt.

- If equity is over the cap: In chapter 7, the trustee may consider administering the non-exempt portion; in chapter 13, you usually keep the car and address the non-exempt value through plan payments.

- Upside-down loans: If you owe more than the car is worth, there’s no equity to protect—and exemptions are usually a non-issue. Your strategy becomes: keep and pay, surrender, or (in limited cases) redeem or negotiate.

- Valuation matters: Use realistic used-market values (private-party sales/comps). Overstating value can make a car look non-exempt unnecessarily.

Quick Examples

- Example A: Car FMV $8,000; loan $4,200 → equity $3,800. Under Michigan’s posted cap (see table), equity is fully exempt; you keep the car.

- Example B: Car FMV $10,500; loan $3,500 → equity $7,000. If that’s above Michigan’s cap, compare the federal vehicle cap (often higher) and consider electing the federal system; in chapter 13 you can keep the car and cover any non-exempt amount in the plan.

In chapter 13, some vehicles with high balances and older vintages may qualify for value-based repayment (“cramdown”) depending on the facts and the 910-day rule—see our vehicle cramdown in chapter 13 overview for details.

Wage and Insurance Exemptions in Michigan

Michigan law and the Bankruptcy Code work together to protect core income streams—your paychecks and certain insurance benefits—so you can cover essentials while your case moves forward. The details differ by chapter and by the type of benefit, so it helps to separate wages from insurance.

How Wage Protection Works (Chapter 7 vs. Chapter 13)

- Chapter 7: Wages you earn after filing are generally not part of the bankruptcy estate, so they remain yours. Wages earned before filing (even if paid after) are typically estate property, but they are rarely a focus unless unusually large and unpaid.

- Chapter 13: Post-petition earnings are part of the estate and fund your plan payment, but you keep working and keep receiving your paychecks. The plan amount accounts for necessities and is designed to be affordable.

- Stopping garnishments: The automatic stay usually halts most wage garnishments once your case is filed. If a creditor kept garnishing after the stay, your attorney can move to enforce the stay and, in some cases, recover recent garnishments.

Garnishment Limits vs. Bankruptcy Protection (Quick Clarifier)

Michigan and federal non-bankruptcy laws cap how much of a paycheck can be garnished outside bankruptcy. Bankruptcy protection is different: the automatic stay stops most garnishments entirely, and exemptions help protect other property from administration. If you’re filing primarily to stop a wage garnishment, the stay is often the most immediate relief.

Insurance Exemptions

Some insurance values and benefits receive protection so a filing doesn’t wipe out critical safety nets. The exact coverage can depend on policy type, ownership, and beneficiaries.

- Life insurance benefits: Proceeds payable to certain beneficiaries are commonly protected under state and/or federal law. Cash-value in whole-life policies may have limits—check your system (Michigan vs. federal) and beneficiary designations.

- Health insurance benefits: Reimbursements and rights under health coverage are typically protected; you can keep using your insurance while your case is pending.

- Disability insurance proceeds: Short-term and long-term disability benefits are generally protected so you can meet basic needs during a period of reduced income.

- Other protected benefits: Many public benefits—like Social Security and unemployment—have separate federal protections. Keep them identifiable in your accounts (don’t commingle excessively) to avoid confusion.

Documentation That Helps

- Wages/pay stubs: Last 60–90 days of pay stubs; note any garnishment line-items or voluntary deductions.

- Policy paperwork: Declarations pages, beneficiary forms, recent statements for any life policy with cash value.

- Benefit letters: Award letters for disability, unemployment, or Social Security; keep direct-deposit statements handy.

Common Pitfalls (and Easy Fixes)

- Confusing caps and exemptions: Non-bankruptcy garnishment limits aren’t the same as bankruptcy exemptions. Filing triggers the stay; exemptions protect property.

- Commingling protected funds: Mixing exempt benefits with other deposits can complicate tracing. If possible, keep protected benefits identifiable.

- Unlisted policies: Forgetting to list a life or disability policy can create headaches. List all policies—even those with no cash value.

Bottom line: between the automatic stay, the chapter you choose, and the exemptions you elect, most filers keep their paychecks flowing and preserve vital insurance benefits. If you rely on disability income or have a life policy with cash value, a quick attorney review can confirm the cleanest way to disclose and protect those funds.

Retirement Accounts: What’s Protected (and What Isn’t)

Most Michigan filers keep their tax-qualified retirement savings. Federal law provides powerful protection for employer plans, and both the Michigan and federal exemption systems recognize retirement as a core necessity. Here’s how it breaks down.

- Employer plans (ERISA-qualified): 401(k), 403(b), profit-sharing, and similar ERISA plans are generally excluded/protected under federal non-bankruptcy law. Practically, these funds are not available to pay creditors.

- IRAs and Roth IRAs: Protected up to the federal cap under 11 U.S.C. § 522(n), as adjusted for inflation. Courts also recognize protection for “rollover” amounts transferred from ERISA plans (traceability helps). The Michigan system likewise protects many tax-qualified retirement benefits—compare systems if you hold large IRA balances.

- Government and public-employee pensions: Typically protected by specific statutes and plan terms; these are usually fully exempt.

- Inherited IRAs (flag this): Federal case law treats inherited IRAs differently than your own retirement funds; protection is more limited and fact-specific. Michigan law offers its own retirement protections, but inherited IRAs remain a “talk to a lawyer” item.

Contributions, Rollovers, and Tracing

- Normal payroll contributions: Ordinary pre-petition deductions are usually fine. Very large, last-minute contributions can draw scrutiny—especially if atypical for your income/history.

- Rollovers: Rolling an old 401(k) into an IRA remains protected so long as you can trace the funds. Keep the rollover statement and account history.

- Don’t commingle unnecessarily: Maintain a clean paper trail (e.g., separate statements) so it’s obvious which funds came from an ERISA plan vs. ongoing IRA contributions.

Loans, Hardship Withdrawals, and Plan Access

- 401(k) loans: The outstanding loan is not a “debt” you can discharge; it’s a plan obligation. If you stop paying, it may be deemed a distribution with tax consequences.

- Hardship withdrawals: Pulling cash before filing can create tax issues and reduce protected balances. If you’re contemplating a withdrawal, get advice before acting.

- Access limits help you: The fact that you can’t freely access a pension/plan before retirement is part of why it’s protected—don’t convert protected assets to cash without a plan.

Documentation That Makes Review Easy

- Most recent statements for each plan (401(k), 403(b), IRA, Roth IRA).

- Rollover proof (distributions and deposit confirmations) if funds moved from an employer plan.

- Beneficiary/plan summaries for pensions and public plans (confirm plan type and restrictions).

Bottom line: retirement accounts are usually safe if they’re tax-qualified and properly documented. The finer points—large IRAs near the federal cap, inherited IRAs, and mixed ERISA/IRA histories—are where a Michigan bankruptcy attorney adds real value by selecting the right exemption system and presenting clean tracing so your savings stay protected.

How Exemptions Are Applied in Practice (Michigan)

Exemptions aren’t just theory—they’re applied through specific disclosures and choices you make on filing day. Here’s how it works in real life, and why getting it right matters.

The Snapshot You Create on Filing Day

- Pick your system: You elect either the Michigan or federal exemptions (no mixing). That choice governs every category.

- List assets + values: Schedules A/B capture what you own at used-market value as of the petition date (the snapshot that counts).

- Claim exemptions: Schedule C lists the statute for each item (e.g., MCL 600.5451 or 11 U.S.C. § 522(d)) and the amount you’re claiming.

Making the Numbers Work

- Supportable valuations: Appraisal/CMA for the home; KBB/private-party comps for vehicles; thrift/yard-sale pricing for household goods.

- Paper the file: Attach/retain payoffs for mortgages/HELOCs, vehicle loan statements, and proof of benefits to show net equity clearly.

- Per-debtor math: In a joint case, some caps effectively double—titling and facts control how much each spouse can claim.

What Happens After You File

- Trustee review: The trustee checks valuations and exemptions. If something’s borderline, documentation speeds approval.

- Objection window: Creditors/trustee have a brief period to object. Clean values + correct statutes usually mean no issues.

- Fixes if needed: You can amend schedules to correct a value, add a payoff, or clarify a statute cite.

- Special motions: If a lien “impairs” an exemption (e.g., a judgment lien on household goods), counsel may file a § 522(f) motion to avoid it.

Why a Michigan Bankruptcy Attorney Helps

- Strategy on systems: Run both Michigan vs. federal scenarios to maximize protection (home vs. vehicle vs. personal property).

- Valuation discipline: Use defensible numbers and the right evidence so exemptions “stick.”

- Edge cases: Tenancy by the entirety, mixed-use property, senior/disability homestead, and benefit tracing need careful handling.

Bottom line: exemptions do the heavy lifting—if they’re claimed precisely. A short review with a Michigan bankruptcy attorney can validate your system choice, tighten valuations, and ensure every protection you’re entitled to is actually captured on your schedules.

Chapter 7 vs. Chapter 13: One-Minute View

In chapter 7, exemptions determine what the trustee can administer vs. what you keep. In chapter 13, you typically keep assets and exemptions help set the plan’s floor through the best-interests test. Your choice between the Michigan and federal systems changes how much is non-exempt—and therefore changes risk (chapter 7) or plan math (chapter 13).

- Chapter 7: Use exemptions to cover equity and minimize what a trustee could administer.

- Chapter 13: Keep assets; pay at least the non-exempt amount over 36–60 months.

Want details and examples? See our Michigan chapter 7 guide, our Michigan chapter 13 guide, and the national overview chapter 7 vs. chapter 13.

Common Questions About Michigan Bankruptcy Exemptions

What assets are fully protected?

It depends on the system you elect (Michigan vs. federal) and your values on the petition date. Many filers fully protect household goods, basic clothing, most retirement, and modest vehicle/home equity within the caps.

Should I choose Michigan or federal exemptions?

Choose the system that protects your mix of assets: homeowners with meaningful equity often prefer Michigan; renters or filers needing a wildcard or stronger vehicle coverage often prefer the federal set. You can’t mix systems. See the comparison section above and run your numbers against both columns before filing.

Can I switch exemption systems after I file?

Generally no. You elect one system for the case and stick with it. That’s why petition-date values and a pre-filing comparison matter. If something is off, amendments can fix typos or add citations—but not usually a wholesale switch of systems.

How often do exemption amounts change?

Federal § 522(d) amounts adjust periodically for inflation; Michigan amounts are updated on a state schedule. Always use the most current posted figures at filing—your table above reflects today’s numbers, but confirm caps if you’re filing later.

What does the trustee actually look at?

- Whether each asset is listed and realistically valued (used-market numbers).

- Which statute you cited for each exemption (Michigan vs. federal).

- Liens/payoffs (to compute equity) and any edge cases (e.g., tenancy by the entirety).

Do exemptions work the same in chapter 7 and chapter 13?

No. In chapter 7, exemptions draw the line between what you keep and what a trustee can administer. In chapter 13, exemptions help set the plan’s “best-interests” floor. For deeper dives, see the Michigan guides: chapter 7 and chapter 13, or the national overview chapter 7 vs. chapter 13.

Are retirement accounts protected?

Most tax-qualified retirement (401(k), 403(b), pensions) is protected under federal/non-bankruptcy law; IRAs are protected up to a federal cap (plus special treatment for rollovers). See the “Retirement Accounts” section in this article for how tracing and documentation work.

What about jewelry, collections, and “odd-ball” items?

Small amounts are typically protected within category caps. If you elect the federal system, the wildcard (§ 522(d)(5)) can “top up” items that exceed a limit. Michigan’s scheme doesn’t include a general wildcard, so compare systems if you own higher-value personal items.

Will a wage garnishment stop when I file?

Usually yes—the automatic stay halts most garnishments. Wages you earn after filing (in chapter 7) are typically yours; in chapter 13, post-petition earnings fund the plan, but you keep working and receiving paychecks. See “Wage and Insurance Exemptions” above for details.

Does a Michigan bankruptcy attorney really make a difference?

Yes—because small valuation/titling choices can swing thousands of dollars of protected value. A Michigan attorney can compare systems, confirm the correct caps, trace retirement funds, address liens, and ensure your Schedule C claims every protection you’re entitled to—cleanly and defensibly.

Tips for Maximizing Your Exemptions and Protecting Your Assets

Great results come from doing a few simple things exactly right: pick the right system (Michigan vs. federal), use realistic values, and claim every category cleanly on Schedule C. Here’s a practical playbook.

Before You File: Set Up the Win

- Run both systems: Compare Michigan caps to federal caps for your mix (home, vehicle, household goods, tools, retirement). Choose the system that protects the most value overall.

- Use petition-date values: Think used-market/“what it would sell for,” not what you paid. Appraisal/CMA for home, private-party comps for vehicles, yard-sale pricing for household goods.

- Map liens/payoffs: Gather current mortgage/HELOC/auto payoffs so equity math is undisputed.

- Decide wildcard strategy: If you need flexibility for “odd-ball” items, note that the federal system includes a wildcard while Michigan’s posted scheme does not—plan accordingly.

As You Prepare Schedules

- Claim every category: On Schedule C, cite the correct statute for each item (MCL 600.5451 or 11 U.S.C. § 522(d) subsection).

- Group wisely: Reasonable sets (dishes, linens, smallwares) can be valued together; list standout items separately.

- Per-debtor math: In joint cases, check whether caps effectively double and confirm titling aligns with your claim.

- Document borderline items: Add 2–3 comps/photos or an appraisal where a value is close to a cap.

After Filing: Keep It Clean

- Trustee review ready: Bring statements, payoffs, and any appraisal/CMA to the meeting of creditors.

- Amend if needed: Fix typos or add supporting detail quickly if questions arise.

- Address impairing liens: If a judgment lien or certain non-purchase-money liens block an exemption, discuss a targeted 11 U.S.C. § 522(f) motion with counsel.

Quick Checklist

- Compare Michigan vs. federal using your numbers

- Use realistic used-market values (home/vehicle/household)

- List liens and current payoffs for clean equity math

- Claim every category with the correct statute cite

- Add proof for any value near a cap

If any item is close to a cap—or if you’re juggling home equity, a higher-value vehicle, or mixed retirement histories—a short review with a Michigan bankruptcy attorney can lock in the right system and ensure every protection you’re entitled to actually sticks.

When to Seek Legal Advice for Bankruptcy in Michigan

If you are preparing to file—or even considering filing—talk to a Michigan bankruptcy attorney first. Exemptions, titling, domicile look-backs, homestead caps, retirement tracing, and lien issues can swing thousands of dollars of protection. A short attorney review up front prevents costly mistakes later.

Always Get Counsel If You’re Filing (or Close To It)

- You’re within weeks of filing: You need petition-date valuations, the right system election (Michigan vs. federal), and clean Schedule C citations.

- Your home/vehicle equity is close to a cap: Strategy and documentation decide whether equity is exempt, administered, or paid through a chapter 13 plan.

- There are liens or judgments: An attorney can evaluate whether a judgment or non-purchase-money lien impairs an exemption and, if so, pursue targeted § 522(f) relief.

- You rely on retirement or benefits: Proper tracing (ERISA rollover vs. IRA contributions) and non-commingling keep these protections intact.

- Married or recently moved: Tenancy by the entirety and the federal domicile look-back can change which system you’re allowed to use and how much you can claim.

What a Michigan Bankruptcy Attorney Will Do

- Run side-by-side Michigan vs. federal scenarios using your real numbers.

- Validate petition-date values (home CMA/appraisal, KBB/private-party for vehicles, used-market pricing for household goods).

- Confirm titling (solo, joint, TBE), lien payoffs, and the correct homestead cap.

- Prepare a clean, defensible Schedule C and address any needed lien-avoidance motion.

Bottom line: If you are losing ground to debt or planning to file, get a Michigan bankruptcy attorney involved early. It’s the surest way to maximize exemptions, keep critical assets, and file once—correctly.

Staying Up to Date: Changes in Michigan Bankruptcy Exemption Laws

Exemption amounts don’t stand still. Both Michigan and the federal system adjust caps on a schedule, and your protections are measured on your petition date. That means the “right” numbers are the ones in effect the day you file—not last year’s article or a generic checklist.

How Often Do Amounts Change?

- Federal (§ 522(d)): Adjusted for inflation on a regular cadence (most recently effective April 1, 2025).

- Michigan (MCL 600.5451): Posted by the state and updated periodically; Michigan last published new figures effective April 1, 2023, with subsequent legislative activity to modernize caps.

- Petition-date control: The amounts in effect on your filing date govern your case.

Where to Check the Current Numbers

- The Michigan statute posting for MCL 600.5451 (official state figures).

- Judicial Conference/official notices for the latest federal § 522(d) amounts.

Timing Tips (Practical)

- File with the best set: If a known update is imminent, compare “now” vs. “after update” numbers before filing.

- Document the snapshot: Appraisals/CMA, vehicle comps, and payoff statements anchored to your petition date reduce disputes.

- Confirm right before you file: A Michigan bankruptcy attorney can sanity-check caps and citations the week you file so Schedule C is bulletproof.

We monitor changes and refresh this page so the numbers you see match what courts and trustees use. If you’re close to filing—or if your equity is near a cap—get a quick Michigan-specific review to make sure you’re using the most favorable, current protections.

Your Fresh Start With Michigan Bankruptcy Exemptions

Michigan bankruptcy exemptions are the engine that lets you keep what matters—your home equity (within the cap), reliable transportation, everyday household goods, and protected retirement—while you reset your finances. Used well, they turn a stressful moment into a structured plan.

You’ve seen how to choose between the Michigan and federal systems, how the numbers work on filing day, and how exemptions play differently in chapter 7 and chapter 13. The final step is simple: match your facts to the table above, use realistic values, and claim every protection cleanly on Schedule C.

Where to Go Next

- Need chapter-specific detail? See Michigan chapter 7 or Michigan chapter 13, or compare both in chapter 7 vs. chapter 13.

- New to the process? Start with the Michigan bankruptcy overview.

One last thought: picking the right system, confirming caps, and documenting values can swing thousands of dollars of protection. A quick review with a Michigan bankruptcy attorney ensures your filing captures every advantage the law allows—so your fresh start actually feels like one.

Explore Our Michigan Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin