Understanding Chapter 13 Bankruptcy in Virginia

When bills are piling up and you are worried about losing your home or car, it can feel like you are out of options. Chapter 13 bankruptcy in Virginia is designed for people with income who need a structured way to catch up on debt without walking away from everything they have worked for.

Instead of wiping out qualifying debts all at once, bankruptcy chapter 13 in Virginia uses a court-approved repayment plan that usually lasts three to five years. During that time, you make one consolidated payment, which can help stop foreclosure, deal with past-due car or mortgage payments, and bring order to overwhelming unsecured debts.

Chapter 13 Bankruptcy in Virginia — At a Glance

- What Chapter 13 Does: A court-supervised repayment chapter under Title 11, Chapter 13 of the U.S. Code that lets eligible Virginia filers catch up mortgage arrears, stabilize car loans, pay priority debts (like certain taxes and domestic support), and obtain a discharge of remaining eligible unsecured debts at the end of a 3–5 year plan.

- Who Chapter 13 Helps in Virginia: Individuals with regular income who are behind on a house or car, need time to pay priority taxes or support, or do not fit well into Chapter 7 but still need powerful federal protection from collection and a structured path to a fresh start.

- Plan Length and Payments: Most Virginia Chapter 13 plans last three to five years. You make a single monthly payment to the Chapter 13 trustee, who then disburses funds to creditors under the confirmed plan, while the automatic stay usually keeps most collection activity on hold.

- Basic Eligibility Requirements: You must have predictable income, keep secured and unsecured debts within the Chapter 13 limits of 11 U.S.C. § 109(e) (amounts adjusted periodically), and complete required credit counseling within 180 days before filing. A Virginia bankruptcy attorney can help verify current limits and eligibility before you file.

- Virginia Exemptions and the Best-Interests Test: Virginia Chapter 13 exemptions—primarily from Title 34 of the Code of Virginia —do not usually decide what you keep, but they do matter under the best interests of creditors test in 11 U.S.C. § 1325(a)(4): your plan must pay unsecured creditors at least as much as they would receive if you filed Chapter 7 and non-exempt property were sold.

- Mortgages, Cars, and Cramdowns: Chapter 13 can stop a foreclosure and allow you to cure past-due mortgage payments over time while keeping up ongoing payments. Many car loans can be restructured, and in some cases you may pay only the vehicle’s current value at a more reasonable interest rate through a Chapter 13 vehicle cram down.

- Life During the Plan: You live on a court-approved budget, make regular plan payments, and typically cannot take on new credit or use general-purpose credit cards without trustee or court approval. Many plans require turning over part or all tax refunds to the trustee; your confirmed plan and local trustee practices control the details.

- Chapter 13 Bankruptcy Virginia Cost: You pay a federal court filing fee for Chapter 13, pay for required counseling courses, and attorney fees that for many Virginia consumer cases often range roughly from $3,500–$5,500 or more, depending on complexity. Most attorney fees are usually paid through your plan payments and reviewed/approved by the court.

- How Often You Can File Chapter 13: Federal timing rules control how soon you can receive another discharge after a prior Chapter 7 or Chapter 13. For a deeper breakdown of these waiting periods, see our guide on how often you can file bankruptcy and discuss your specific filing history with a Virginia bankruptcy attorney.

- Key Pros and Cons vs. Chapter 7: Pros include keeping important assets, catching up secured debts over time, and handling priority debts in one organized plan. Cons include a 3–5 year commitment, the need for steady income, limits on new credit, and the risk of dismissal if you fall behind. Chapter 13 is often best for Virginia filers who want structure, protection, and time to fix secured and priority debt problems.

- Why a Virginia Chapter 13 Attorney Matters: Chapter 13 in Virginia blends federal law, state exemptions, local trustee practices, and court-specific procedures. An experienced Virginia Chapter 13 lawyer can test your numbers, design a feasible plan, anticipate trustee concerns, and guide you from filing through confirmation and discharge.

Filing chapter 13 bankruptcy in Virginia is not just about filling out forms. You must meet certain eligibility rules, complete required credit counseling, and be able to support a realistic payment plan. You will also work closely with a chapter 13 trustee in Virginia, who collects your payments and distributes them to creditors according to the court’s order.

This guide walks through how filing bankruptcy chapter 13 in Virginia actually works in real life—what to expect, common pitfalls to avoid, and the questions you should be asking before you commit. The goal is to give you clear, practical information so you can talk with a qualified bankruptcy attorney and make confident decisions about your next step.

What Is Chapter 13 Bankruptcy in Virginia?

Chapter 13 bankruptcy in Virginia is the repayment chapter of the federal Bankruptcy Code (chapter 13 of Title 11 of the United States Code). It is designed for individuals with regular income who need time and structure to deal with debt while keeping key property like a home and vehicle.

Key Features of Chapter 13 Bankruptcy in Virginia

Under bankruptcy chapter 13 in Virginia, you propose a court-approved repayment plan that usually lasts three to five years. During that plan, you can use federal chapter 13 tools together with bankruptcy laws in Virginia to solve several problems at once: catching up on mortgage arrears, restructuring car loans, and paying back priority debts that would not simply disappear in chapter 7.

How Chapter 13 Helps You Catch Up and Protect Essentials

Filing chapter 13 bankruptcy in Virginia can allow you to cure a past-due home loan over time, keep a vehicle you rely on, and in some cases pay only the current value of the car at a reasonable interest rate through a chapter 13 vehicle cram down. You can also use the plan to pay non-dischargeable taxes and domestic support obligations, such as child support or alimony, in an organized and enforceable way.

How Virginia Exemptions Affect a Chapter 13 Plan

Virginia law still matters inside this federal framework, but not because chapter 13 expects you to surrender property. In a chapter 13 case, Virginia exemption laws — found primarily in Title 34 of the Code of Virginia — are used in the “best interests of creditors” test. Your plan must pay unsecured creditors at least as much as they would receive if you filed chapter 7 and a trustee liquidated non-exempt property. In practice, you generally keep your property in chapter 13 as long as you complete the plan, and the exemptions help determine how much certain creditors must be paid for the plan to be confirmable and feasible. For a detailed breakdown of the current exemption amounts and statutes, see our Virginia bankruptcy exemptions reference guide, which is our primary resource on how Virginia exemptions work in both chapter 7 and chapter 13.

Quick Summary: What Chapter 13 in Virginia Does

To summarize, filing bankruptcy chapter 13 in Virginia typically involves:

- A court-approved repayment plan lasting three to five years.

- Keeping key assets while catching up on mortgages and car loans.

- Using the plan to pay priority debts like certain taxes and support, then discharging remaining unsecured debts.

Eligibility Requirements for Filing Chapter 13 Bankruptcy in Virginia

Not everyone can file chapter 13 bankruptcy in Virginia. This chapter is built around a court-approved repayment plan, so the law focuses on whether you have enough income and the right kind of debt profile to make a realistic plan work.

Regular Income to Support a Repayment Plan

To file for chapter 13 bankruptcy in Virginia, you need a regular, predictable income. That can come from wages, self-employment, Social Security, pensions, or a combination of sources. The key is that you can make consistent monthly payments under your proposed plan after covering reasonable living expenses like housing, food, and transportation.

Debt Limits Under Chapter 13

Chapter 13 is only available if your debts stay within certain limits set by federal law. Under 11 U.S.C. § 109(e), there are separate caps for secured and unsecured debts, and those figures are adjusted periodically. Instead of relying on old numbers, it is important to have a bankruptcy attorney or trusted advisor confirm the current chapter 13 debt limits before filing chapter 13 bankruptcy in Virginia.

Mandatory Credit Counseling Before You File

Before filing bankruptcy chapter 13 in Virginia, you must complete a credit counseling session through an approved agency, usually within 180 days before your case is filed. This session is meant to review your budget, discuss alternatives, and confirm that chapter 13 is an appropriate way to address your debt. You will receive a certificate of completion that must be filed with your case.

In practical terms, here are the primary eligibility criteria for chapter 13 bankruptcy in Virginia:

- Having a regular income source sufficient to fund a repayment plan.

- Keeping secured and unsecured debts within the chapter 13 limits under 11 U.S.C. § 109(e).

- Completing a pre-filing credit counseling session with an approved provider.

| Requirement | What It Means | Legal / Practical Basis |

|---|---|---|

| Regular Income | You must have predictable income (wages, self-employment, Social Security, pensions, etc.) to support monthly plan payments after basic living expenses. | Core feature of chapter 13’s repayment structure and feasibility requirement. |

| Debt Within Chapter 13 Limits | Your secured and unsecured debts must fall within the current chapter 13 caps. Exact numbers change periodically. | 11 U.S.C. § 109(e); limits adjusted from time to time, so current figures must be confirmed. |

| Credit Counseling | You must complete a credit counseling session from an approved agency within 180 days before filing and file the completion certificate with the court. | Mandatory pre-filing requirement under the Bankruptcy Code and local court practice. |

The Chapter 13 Bankruptcy Process in Virginia: Step-by-Step Overview

Filing chapter 13 bankruptcy in Virginia is a structured but detailed process. What follows is a high-level overview of the typical steps in a Virginia chapter 13 case, not a complete roadmap or a substitute for legal advice. Because local rules and practices in the Virginia bankruptcy courts can be technical, it is usually a smart move to work with an experienced Virginia chapter 13 bankruptcy attorney to guide you through the details.

Filing Your Petition and Starting the Automatic Stay

The journey begins with filing a bankruptcy petition and related forms at your local Virginia bankruptcy court. These documents list your income, expenses, debts, property, and recent financial history. Once your case is filed, an automatic stay goes into effect, which generally halts most collection actions against you, including many lawsuits, garnishments, and foreclosure efforts. For many people filing chapter 13 bankruptcy in Virginia, this immediate pause in creditor pressure is a critical first step.

Proposing a Chapter 13 Repayment Plan

Early in the case, you or your attorney will submit a chapter 13 repayment plan. This plan explains how you intend to pay secured, priority, and unsecured creditors over a three- to five-year period. The plan must be feasible based on your actual income and living expenses and must meet the legal requirements of chapter 13 and any applicable local rules in Virginia. The better your plan is drafted on the front end, the smoother the rest of the process tends to be.

The 341 Meeting of Creditors

After your case is filed, you will attend a meeting of creditors, also called a 341 meeting. This is usually a short, mandatory hearing where you answer questions under oath about your finances, your paperwork, and your proposed plan. A chapter 13 trustee in Virginia conducts this meeting, and creditors may appear to ask questions, although many do not. Bringing complete, accurate information helps keep this part of the process straightforward.

Plan Confirmation and Ongoing Payments

The bankruptcy court then reviews your chapter 13 plan. The judge looks at whether the plan is feasible, proposed in good faith, and compliant with the Bankruptcy Code and chapter 13 bankruptcy laws in Virginia, including the “best interests of creditors” and “disposable income” tests. If the plan is confirmable, the court will enter an order approving it. You make regular payments to the chapter 13 trustee in Virginia, and the trustee distributes funds to creditors according to the confirmed plan.

Throughout the process, a chapter 13 trustee in Virginia plays a vital administrative role — reviewing your documents, conducting the 341 meeting, and overseeing payment distribution — while your attorney (if you have one) helps you navigate legal strategy, plan modifications, and any issues that arise. Because filing bankruptcy chapter 13 in Virginia involves both federal law and local practice, having local legal guidance can be the difference between a dismissed case and a successful discharge at the end of your plan.

Here are the key steps in summary:

- File a chapter 13 bankruptcy petition and schedules with the Virginia bankruptcy court.

- Propose a repayment plan that meets feasibility and legal requirements.

- Allow the automatic stay to take effect and temporarily halt most collection activity.

- Attend the 341 meeting of creditors conducted by the chapter 13 trustee in Virginia.

- Obtain court approval (confirmation) of your plan, if it meets the legal tests.

- Make ongoing plan payments to the trustee, who distributes funds to creditors.

| Step | What Happens | Who Is Involved |

|---|---|---|

| 1. File the Case | You file a chapter 13 petition and schedules with the Virginia bankruptcy court, disclosing income, expenses, debts, and property. The automatic stay usually begins here. | You (and your attorney, if represented), bankruptcy court clerk. |

| 2. Propose the Plan | You submit a chapter 13 repayment plan that explains how secured, priority, and unsecured creditors will be paid over three to five years. | You, your attorney, chapter 13 trustee in Virginia. |

| 3. Automatic Stay | Most collection activity stops while the case is pending, including many lawsuits, garnishments, and foreclosure actions. | Creditors, bankruptcy court, chapter 13 trustee. |

| 4. 341 Meeting of Creditors | You attend a short, mandatory meeting, answer questions under oath about your finances, and address trustee or creditor concerns about your plan. | You, chapter 13 trustee in Virginia, any creditors who appear. |

| 5. Plan Confirmation | The judge decides whether to confirm your plan based on feasibility, good faith, and compliance with the Bankruptcy Code and chapter 13 bankruptcy laws in Virginia. | Bankruptcy judge, chapter 13 trustee, you and your attorney. |

| 6. Plan Payments & Discharge | You make regular payments to the trustee. If you complete the plan and meet all requirements, the court enters a discharge of qualifying remaining debts. | You, chapter 13 trustee in Virginia, bankruptcy court. |

Key Benefits and Drawbacks of Chapter 13 Bankruptcy in Virginia

Chapter 13 bankruptcy in Virginia can be a powerful tool if you are behind on payments but still have steady income and want to keep important property. Instead of facing scattered collection actions, you bring everything into one court, one plan, and one monthly payment that is designed around your budget.

Like any major financial decision, filing chapter 13 bankruptcy in Virginia comes with trade-offs. The same structure that protects you and gives you time to catch up also requires discipline, transparency, and the ability to stay on track for several years. Understanding both sides of the equation can help you decide whether this chapter is a good fit for your situation.

Benefits of Chapter 13 Bankruptcy in Virginia

For many people, the most attractive feature of bankruptcy chapter 13 in Virginia is the chance to protect assets while solving multiple problems in one plan. You can stop a foreclosure, deal with car loans, pay priority debts, and still work toward a discharge of remaining eligible unsecured debts at the end of the case.

Benefits:

- Stops foreclosure and gives you time to catch up overdue mortgage payments through the plan.

- Allows you to keep key assets, such as a home and vehicle, while making structured payments over three to five years.

- Uses the automatic stay to pause most collection actions, lawsuits, and garnishments while the case is pending.

- Provides a single, court-supervised repayment structure instead of juggling multiple creditors and payment arrangements.

Drawbacks and Challenges of Chapter 13

The same structure that makes chapter 13 bankruptcy laws in Virginia helpful can also make this chapter demanding. A plan that lasts three to five years requires consistent income and a willingness to live within a carefully managed budget. If your financial situation changes significantly, you may need to modify the plan or consider other options.

Drawbacks:

- Requires regular, reliable income to make monthly plan payments for up to five years.

- Limits your financial flexibility while the plan is in place, because missed payments can jeopardize your case.

- Failure to follow the plan or meet legal requirements can lead to dismissal or conversion to another chapter.

Because these benefits and drawbacks play out differently for each person, talking with an experienced Virginia chapter 13 bankruptcy attorney can help you understand how the chapter 13 framework would apply to your specific income, assets, and goals.

Chapter 13 Bankruptcy Laws and Exemptions in Virginia

Chapter 13 bankruptcy laws in Virginia work within the federal Bankruptcy Code, but Virginia’s exemption statutes still play an important role. In a chapter 13 case, exemptions do not usually decide which property you keep. Instead, Virginia exemptions help determine how much unsecured creditors must be paid for the plan to be confirmable.

How Virginia Exemptions Affect a Chapter 13 Plan

When you file chapter 13 bankruptcy in Virginia, the court must apply the “best interests of creditors” test under 11 U.S.C. § 1325(a)(4). The court compares what unsecured creditors would receive if you filed a hypothetical chapter 7 case, using Virginia exemption laws to see how much equity would be non-exempt and available for liquidation. Your chapter 13 plan must pay unsecured creditors at least that much over the life of the plan.

Virginia exemption laws — found primarily in Title 34 of the Code of Virginia — reduce the amount of non-exempt equity that would be available in that chapter 7 comparison. The more value that is properly protected by exemptions, the lower the minimum payout that unsecured creditors must receive through your chapter 13 plan. In this way, exemptions influence plan design and feasibility rather than forcing you to surrender property.

Key Virginia Exemptions That Influence Your Plan

Some of the most important Virginia exemptions in a chapter 13 best-interests analysis include:

- Homestead Exemption: Protects a certain amount of equity in your primary residence, reducing the non-exempt home equity that would have to be paid to unsecured creditors.

- Wildcard Exemption: Allows you to protect additional personal property or equity, giving flexibility to shield assets that matter most and potentially lowering the required payout to unsecured creditors.

- Vehicle Exemption: Safeguards equity in one motor vehicle up to the allowed amount, which can limit how much non-exempt vehicle equity factors into the best-interests test.

- Household Goods Exemption: Protects everyday household items, further reducing the pool of non-exempt property that would otherwise increase the minimum required plan payment.

By understanding how Virginia exemptions interact with chapter 13 bankruptcy laws in Virginia, you can see how careful exemption planning can make a chapter 13 plan more manageable while still satisfying the best-interests test for unsecured creditors. Because exemption rules and dollar amounts can change, and because the analysis can be technical, it is wise to review your situation with a knowledgeable Virginia bankruptcy attorney before filing.

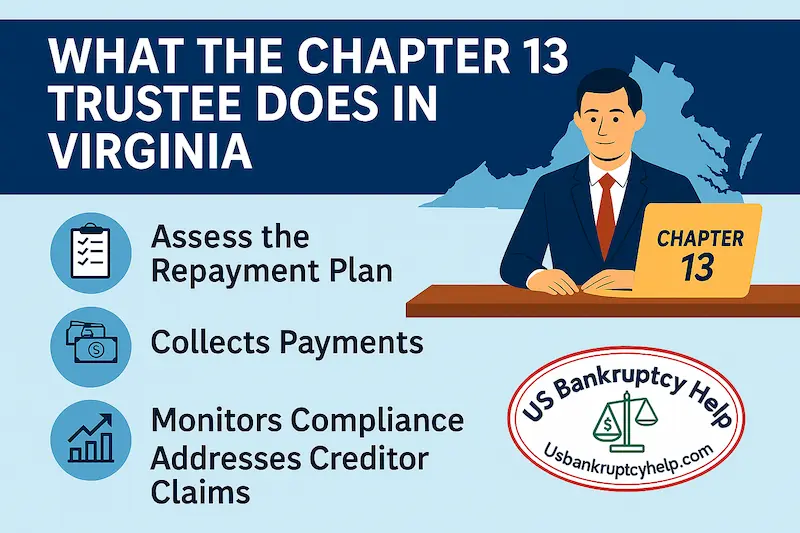

The Role of the Chapter 13 Trustee in Virginia

In a Virginia chapter 13 case, the chapter 13 trustee is the person who stands between your plan on paper and how it actually works in real life. The trustee is not your lawyer or the judge, but a court-appointed fiduciary who reviews your proposed plan for feasibility, helps make sure it complies with the Bankruptcy Code, and then administers payments to your creditors once the plan is confirmed.

Reviewing Your Plan for Feasibility and Confirmation

After you file chapter 13 bankruptcy in Virginia, the trustee reviews your petition, schedules, and proposed repayment plan. They look at your income, reasonable expenses, and debt structure to decide whether the plan is feasible and meets the statutory requirements, including the best interests of creditors test and disposable income test under chapter 13 bankruptcy laws in Virginia.

If the trustee believes your plan meets those requirements, they will typically recommend or stipulate to confirmation, allowing the judge to approve the plan. If there are problems — such as unrealistic payment amounts, missing information, or failure to meet legal standards — the trustee may object and require changes before the plan can be confirmed.

Collecting Payments and Distributing Money to Creditors

Once the court confirms your plan, the chapter 13 trustee in Virginia becomes your primary payment hub. You send regular plan payments to the trustee, usually monthly. The trustee then disburses those funds to creditors according to the terms of your confirmed plan — secured creditors, priority claims like certain taxes and domestic support, and then unsecured creditors.

This centralized payment system is one of the biggest practical benefits of bankruptcy chapter 13 in Virginia. Instead of juggling multiple due dates and collectors, you work with one trustee payment schedule that is supervised by the court.

Monitoring Your Case and Filing Motions to Dismiss

The trustee’s job does not end at confirmation. Throughout your chapter 13 repayment period, the trustee monitors whether you are staying current on plan payments and complying with other plan requirements. Most Virginia chapter 13 plans require you to provide copies of your tax returns each year and, in some cases, to turn over part or all of your tax refunds to help fund the plan.

If you fall behind on plan payments, fail to provide required tax returns, or otherwise do not follow the confirmed plan, the trustee may file a motion to dismiss your case (or in some circumstances seek conversion to another chapter). Often, problems can be addressed through communication and, when appropriate, a plan modification, but ignoring trustee notices almost always makes things worse.

How Many Chapter 13 Trustees Serve Virginia?

Virginia has two bankruptcy districts — the Eastern District of Virginia and the Western District of Virginia — and chapter 13 cases are assigned to standing trustees based on where you file.

- Eastern District of Virginia (EDVA): There are five standing chapter 13 trustees serving different divisions of the Eastern District. The official court website provides a current list and links to each trustee’s site on its Chapter 13 Trustee Websites page.

- Western District of Virginia (WDVA): There are two chapter 13 standing trustees serving the Western District. The Roanoke trustee’s office (Christopher Micale) maintains a trustee website with contact information and resources, and the Charlottesville trustee’s office (Angela Scolforo) maintains its own site for cases assigned to that office.

You can usually confirm which chapter 13 trustee is assigned to your case by checking your official Notice of Bankruptcy Case, reviewing the Eastern or Western District bankruptcy court websites, or asking your attorney. Knowing who your trustee is — and understanding their role — makes it easier to stay in compliance and successfully complete your plan.

Life During a Chapter 13 Repayment Plan

Life during a chapter 13 repayment plan in Virginia is structured, but it does not have to be miserable. If you are honest about your finances, stick to your budget, and avoid living beyond your means, day-to-day life can be relatively stable. Many people find that chapter 13 becomes a built-in financial coaching system that teaches discipline and long-term money skills.

Living on a Court-Approved Budget

Your chapter 13 plan is built around a budget the court and trustee have seen and effectively signed off on. You make regular plan payments, keep up with housing, utilities, food, transportation, and other necessary expenses, and avoid unnecessary splurges. When you treat the plan payment like a non-negotiable bill, the rest of your financial life often becomes simpler and more predictable.

During the plan, you generally cannot freely take on new debt or use unsecured credit cards the way you did before filing. The expectation in a chapter 13 case is that you live within your means, pay your household expenses, and send the agreed amount to the chapter 13 trustee each month.

New Credit and Big Purchases During Chapter 13

As a rule, you should assume that you cannot get new credit or open new credit cards during your chapter 13 case without permission. Incurring new debt without court or trustee approval can put your plan at risk and may lead to objections or a motion to dismiss. If you truly need new credit for a legitimate reason, there is a proper way to ask.

Real life still happens during a three- to five-year plan. Cars break down, families grow, and sometimes a move makes sense. If something happens to your vehicle during the case and you legitimately need to replace it, it is often possible to finance a different car while you are in chapter 13. The chapter 13 trustee's permission is required.

In some circumstances, people in a chapter 13 repayment plan even purchase a home before the case is over. Again, this typically requires court and/or trustee approval, a clear explanation of how the new mortgage payment fits your income and budget, and sometimes an adjustment to your plan. The key is transparency and getting permission first, not asking for forgiveness later.

Making Chapter 13 Work for You

If your natural approach is to be truthful, organized, and conservative with money, chapter 13 can actually feel easier over time. You know what you owe each month, you are protected from most collection pressure, and you have a clear finish line. For many people, the structure of a chapter 13 plan becomes an opportunity to reset spending habits, build better financial routines, and come out of the case with stronger money skills than they had going in.

Staying on track with your repayment plan brings peace of mind and a realistic path to a fresh start. Here are key habits to keep in mind during a chapter 13 repayment plan:

- Stick to your budget and treat the plan payment like a top-priority bill.

- Prioritize necessary expenses (housing, utilities, food, transportation) over discretionary spending.

- Do not take on new credit or loans without first talking to your attorney and obtaining trustee or court approval.

- Provide required documents on time, including annual tax returns and any tax refunds if your plan requires them.

- Keep communication open with your chapter 13 trustee and your attorney if your income or expenses change.

Frequently Asked Questions About Chapter 13 Bankruptcy in Virginia

Navigating chapter 13 bankruptcy in Virginia naturally raises a lot of practical questions about how life will work during your case. The answers below are general information, not legal advice, but they should give you a clearer picture of what to expect before you talk with a Virginia chapter 13 bankruptcy attorney about your specific situation.

Will I Have to Turn Over My Tax Refunds During My Chapter 13 Plan?

In many Virginia chapter 13 cases, you are required to provide copies of your tax returns each year and turn over some or all of your tax refunds to the chapter 13 trustee. The exact rule depends on your local trustee’s practice and what your confirmed plan and confirmation order say. Some plans allow you to keep part of a refund for necessary expenses, while others require the entire refund to be paid into the plan. It is critical to read your plan carefully and ask your attorney how tax refunds are treated in your case.

Can I Catch Up My House in Chapter 13?

Yes. One of the biggest advantages of filing chapter 13 bankruptcy in Virginia is the ability to cure mortgage arrears over time. As long as you can afford to make your regular mortgage payment plus the catch-up amount through your chapter 13 plan, you can often bring a past-due home loan current over three to five years while the foreclosure process is stopped by the automatic stay. Your ongoing mortgage payment is usually paid directly, and the arrears are paid through the trustee.

Can I Keep a Credit Card in Chapter 13?

In most chapter 13 cases, your existing general-purpose credit cards are closed or unusable once you file. Even if a card technically remains open, using it to borrow more money while you are in chapter 13 can create serious problems with your plan and your discharge. The expectation in chapter 13 is that you live on your income and budget, not on new unsecured credit, so you should not plan on keeping or using traditional credit cards during your case.

Can I Get a Credit Card While I Am in Chapter 13?

Usually, you cannot take on new credit during a chapter 13 case without permission. If there is a legitimate reason to obtain new credit — for example, a small secured card to rebuild credit near the end of your plan — your attorney can request trustee or court approval and show that the new payment will not jeopardize your existing chapter 13 obligations. The key rule is simple: do not apply for or use new credit during chapter 13 unless your attorney and the trustee sign off on it first.

How Much Does Chapter 13 Bankruptcy Cost in Virginia?

Attorney fees for chapter 13 bankruptcy in Virginia are typically structured so that most or all of the fee is paid through your plan payments rather than all up front. For a straightforward case, total attorney fees often fall in the range of roughly $3,500 to $5,500, but they can be higher if the case involves significant motion practice, objections, or plan modifications. The court usually reviews and approves these fees, and the chapter 13 trustee then pays your attorney from the funds you send into the plan. You will also have out-of-pocket costs like the court filing fee and required counseling courses.

How Often Can You File Chapter 13 in Virginia?

The rules about how often you can file chapter 13 are set by federal law, not just Virginia practice. The timing depends on what kind of case you filed before and whether you received a discharge. For a deeper dive into the waiting periods between bankruptcies and how they work in real life, see this detailed guide on how often you can file bankruptcy. A Virginia bankruptcy attorney can help you apply those timing rules to your specific filing history.

Can I Modify My Repayment Plan If Circumstances Change?

Yes. If your income goes down, necessary expenses go up, or something significant changes in your life while you are in chapter 13, it may be possible to modify your plan. Your attorney can file a motion to modify and propose new plan terms that still meet the requirements of chapter 13 bankruptcy laws in Virginia. In some cases, a change in circumstances may also lead to discussions about converting to another chapter or, if appropriate, seeking a hardship discharge. The important thing is to communicate early rather than simply falling behind on payments.

How Chapter 13 Has Helped Virginians in Real Life

The examples below are simplified, anonymized scenarios based on common patterns in Virginia Chapter 13 cases. Every case is different and results can vary, but they show how Chapter 13 bankruptcy in Virginia can work in practice.

- Richmond Homeowner Catching Up a Mortgage: A family in Richmond was more than six months behind on their mortgage and facing a foreclosure sale. By filing Chapter 13 bankruptcy in Virginia, they stopped the foreclosure, spread roughly $18,000 in arrears over a 60-month plan, kept making their regular mortgage payment, and paid back a small tax debt. At the end of the plan, the loan was current and remaining credit-card balances were discharged.

- Virginia Beach Driver Restructuring Car Debt: A Virginia Beach filer owed more on a car than it was worth and was behind on payments. In Chapter 13, they used a Chapter 13 vehicle cram down to pay the car’s current value at a reduced interest rate through the plan, caught up past-due amounts, and still received a discharge of several credit-card accounts.

- Roanoke Filer Managing Tax and Support Obligations: In Roanoke, a self-employed debtor had several years of priority income taxes and a domestic support arrearage. Their Chapter 13 plan focused on paying those priority debts in full over five years while keeping their vehicle and tools of the trade. Unsecured business and credit-card debts received only a small percentage and were discharged at the end of the case.

- Northern Virginia Household Choosing Structure Over Chaos: A Fairfax-area family with steady income but heavy unsecured debt used Chapter 13 to consolidate multiple lawsuits, garnishments, and collection accounts into one payment to the Chapter 13 trustee. They committed to a strict budget, turned over tax refunds as required, and completed a 36-month plan that left them with a single, affordable mortgage and no remaining unsecured balances.

These examples do not guarantee any particular outcome in your case, but they highlight how filing bankruptcy Chapter 13 in Virginia can be customized to your income, assets, and goals when you work with an experienced Virginia bankruptcy attorney.

Is Chapter 13 Bankruptcy in Virginia Your Next Step?

Deciding whether to file chapter 13 bankruptcy in Virginia is less about finding a perfect option and more about choosing the most realistic path forward. This chapter can help you catch up a home, stabilize car loans, deal with priority taxes and support, and still work toward a discharge of remaining unsecured debts — but only if the plan fits your income, your budget, and your long-term goals.

Chapter 13 works best for people who are willing to be transparent about their finances, live within a court-approved budget, and commit to making steady plan payments. If that sounds like you, chapter 13 can function as both a legal protection and a financial reset, giving you structure, breathing room from collection pressure, and a clear finish line if you stay the course.

On the other hand, if your income is unstable, you are not ready to make hard choices about spending, or you are hoping for a quick fix, filing bankruptcy chapter 13 in Virginia may feel more like a burden than a solution. In those cases, it is especially important to explore all options — including chapter 7, non-bankruptcy workouts, or simply waiting until your situation changes.

Because chapter 13 bankruptcy laws in Virginia blend federal rules, state exemptions, local trustee practices, and court-specific procedures, getting personalized advice matters. A conversation with an experienced Virginia chapter 13 bankruptcy attorney can help you test your numbers, understand your trustee’s expectations, and see exactly how a plan would look in your real life. Armed with that information, you can decide whether chapter 13 is the right tool to move you toward the fresh start you are looking for.

Explore Our Virginia Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin