Exploring Chapter 13 Bankruptcy in North Carolina

Navigate Chapter 13 North Carolina bankruptcy easily. Learn filing steps, unique rules, and asset protection to manage debts while keeping property.

Your Guide to Chapter 13 Bankruptcy in North Carolina

Chapter 13 bankruptcy offers a lifeline for those drowning in debt. It allows individuals to reorganize their financial obligations. This process can be complex, especially in North Carolina. Understanding Chapter 13 is crucial for making informed decisions. It involves creating a repayment plan over three to five years. This plan helps manage debts while keeping assets.

Filing Chapter 13 in North Carolina requires meeting specific criteria. Regular income is necessary to qualify. The process also involves credit counseling and court approval. The rules for Chapter 13 bankruptcy in North Carolina are unique. They include specific exemptions and asset protections. Knowing these rules can help protect your financial future.

The benefits of Chapter 13 are significant. It can prevent foreclosure and repossession. However, it also impacts credit scores and requires commitment. Navigating Chapter 13 bankruptcy can be daunting. Legal guidance is often recommended. This article will explore the process, rules, and benefits in detail.

Where Chapter 13 Cases are Filed North Carolina

North Carolina Chapter 13 cases are filed with the U.S. Bankruptcy Court. Depending on where you live, cases are filed in the Eastern (Raleigh, Greenville, New Bern, Wilmington, Fayetteville), Middle (Greensboro, Winston-Salem), or Western District (Charlotte, Asheville, Statesville, Shelby).

341 Meeting of Creditors for North Carolina Cases

Today, §341 Meetings of Creditors are conducted by secure video (Zoom) across all three districts unless a special designation requires otherwise. Once your case is filed, a standing chapter 13 trustee is assigned to administer it: the trustee reviews your petition and proposed plan, presides over the 341 meeting, collects monthly plan payments, disburses funds to creditors under the confirmed plan, monitors compliance, and makes recommendations or objections as needed until discharge.

North Carolina Chapter 13 Trustees (6)

When you file for chapter 13 bankruptcy in North Carolina, a standing trustee is automatically assigned to oversee your case. These trustees play a central role in the process—they review your repayment plan, conduct your 341 meeting of creditors, collect monthly payments, and distribute funds to creditors according to the court-approved plan. North Carolina has six dedicated chapter 13 trustees across its three federal districts (Eastern, Middle, and Western). Each trustee is appointed to ensure cases run smoothly, provide oversight, and help debtors stay on track toward completing their repayment plans. Knowing who the trustees are in your district can give you clarity and confidence as you navigate the bankruptcy process.

- S. Troy Staley — Eastern District (New Bern)

- Michael B. Burnett — Eastern District (Raleigh)

- Anita Jo Kinlaw Troxler — Middle District (Greensboro/Durham)

- Brandi L. Richardson — Middle District (Winston-Salem)

- Steven G. Tate — Western District (Asheville/Bryson City/Statesville/Shelby)

- Jenny P. Holman — Western District (Charlotte)

What Is Chapter 13 Bankruptcy?

Chapter 13 bankruptcy is a legal option for people with regular income. It allows them to reorganize and consolidate their debt. This approach focuses on a structured repayment plan.

Chapter 13 doesn't offer a fast discharge, like chapter 7. Debtors propose a repayment plan to pay creditors over a set period. This period usually ranges from three to five years. You can find out more about the differences between Chapter 7 and Chapter 13 in our comprehensive guide.

Here are key features of Chapter 13 bankruptcy:

- Reorganizes debt rather than liquidating assets.

- Requires a feasible repayment plan approved by the court.

- Protects assets like homes and cars from creditors.

The repayment plan must consider the debtor's income and expenses. This ensures the plan is realistic and sustainable. The bankruptcy court evaluates and confirms it.

Chapter 13 is often a preferred choice for those who can repay part of their debts. It offers a second chance to regain financial stability. Individuals can protect their property while responsibly managing their debt.

Who Qualifies for Chapter 13 in North Carolina?

Qualifying for Chapter 13 in North Carolina primarily requires a regular income. Individuals must demonstrate an ability to make consistent payments. This regular income supports the proposed debt repayment plan.

Debtors must also meet debt limits to qualify. Secured debts, like mortgages, should not exceed a certain threshold. Additionally, unsecured debts, including credit card bills, must also fall below a specific limit.

For eligibility, debtors should not have had a previous bankruptcy dismissed in the past 180 days. This can occur if one fails to comply with court orders. Moreover, it may happen if the filing was deemed frivolous.

Here is a list of the primary qualification criteria for Chapter 13:

- Proof of regular income sufficient to cover debts.

- Total secured and unsecured debts must be below specified limits.

- No recent Chapter 13 dismissal for failure to comply.

- Completion of a credit counseling course pre-filing.

Meeting these qualifications is essential for filing Chapter 13 in North Carolina. Eligibility ensures a sustainable plan for debt management. It is also a requirement for court approval of the bankruptcy plan.

Key Chapter 13 Bankruptcy Rules in North Carolina

Chapter 13 bankruptcy rules in North Carolina are designed to guide debtors through the process smoothly. One core rule is completing credit counseling prior to filing. This step ensures debtors understand their financial options and impacts.

Another rule involves filing necessary documents with the bankruptcy court. This includes a comprehensive list of all assets and liabilities. Debtors must also submit detailed income and expense reports.

The repayment plan is a cornerstone of Chapter 13. It must prioritize certain debts such as child support and alimony. The court reviews and approves this plan to ensure fairness and feasibility.

Key requirements include attending the 341 meeting, also known as the meeting of creditors. Here, creditors may question debtors about their financial situation. Attendance is mandatory for the process to proceed.

To summarize, the fundamental rules of Chapter 13 in North Carolina are:

- Complete credit counseling with an approved agency.

- File detailed financial documentation with the court.

- Propose a feasible repayment plan prioritizing important debts.

- Attend the 341 meeting of creditors for further questioning.

Adhering to these rules is crucial for a successful Chapter 13 filing. They ensure that the process is transparent and equitable. Following the guidelines can lead to a positive outcome for the debtor.

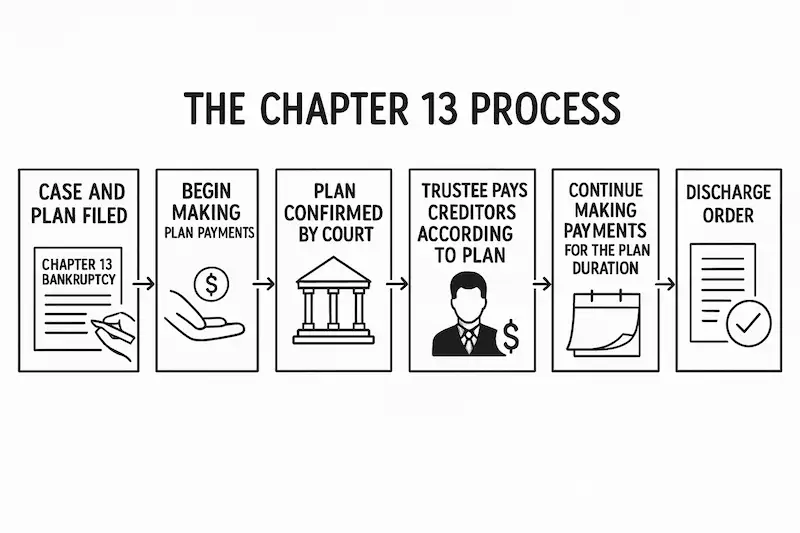

The Chapter 13 Bankruptcy Process: Step-by-Step

The Chapter 13 bankruptcy process in North Carolina involves several detailed steps. Each phase requires careful attention to detail to ensure a successful outcome for the debtor.

The first step is to gather and prepare financial information. This includes details about assets, liabilities, income, and expenses. Complete and accurate records are crucial for the process.

Next, debtors must complete a credit counseling session. An approved agency provides this service to help manage financial challenges. It’s a mandatory part of the process before filing for bankruptcy.

Filing the bankruptcy petition with the court is the next step. This action triggers the automatic stay, halting most collection activities. It provides temporary relief from creditors and collection agencies.

The debtor must then propose a repayment plan to the court. This plan outlines how debts will be repaid over 3 to 5 years. The court must approve the plan for it to proceed.

A trustee is appointed to oversee the case. They ensure that the repayment plan is followed correctly. The trustee also manages the distribution of payments to creditors.

Debtors must attend the 341 meeting, commonly known as the meeting of creditors. At this meeting, creditors and the trustee can ask questions. Attendance is critical to the bankruptcy process.

Finally, after successful completion of the repayment plan, debts are discharged. This discharge signifies the end of the bankruptcy process, providing a fresh financial start.

Key Steps Include:

- Gather and prepare detailed financial information.

- Complete mandatory credit counseling.

- File the bankruptcy petition and propose a repayment plan.

Further Actions Required:

- Attend the 341 meeting of creditors.

- Adhere to the terms of the repayment plan.

- Achieve debt discharge after plan completion.

Navigating each step diligently is crucial for a favorable outcome. This structured approach helps debtors regain control of their finances. Understanding the process can significantly ease the journey through Chapter 13 bankruptcy.

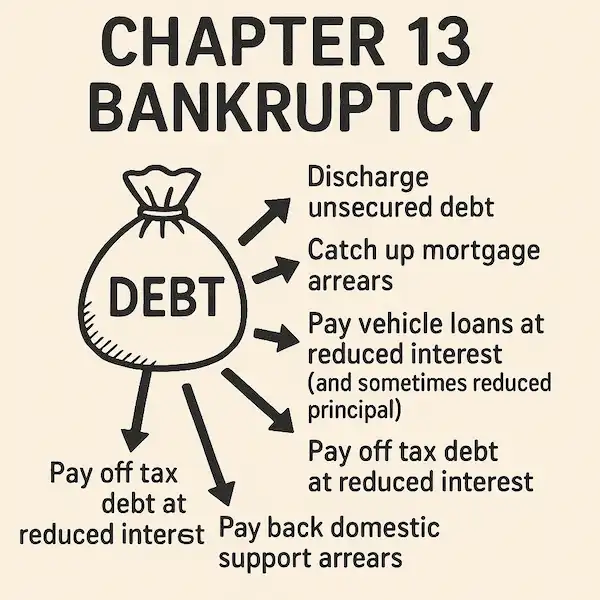

Creating a Chapter 13 Repayment Plan

Creating a Chapter 13 repayment plan is crucial for the bankruptcy process. This plan outlines how debts will be managed and paid off. It's essential for the plan to be realistic and well-structured.

The plan must prioritize certain debts to ensure compliance with bankruptcy rules. Priority debts include taxes, child support, and alimony. These must be paid in full during the repayment period.

Secured debts, like mortgages and car loans, can be restructured under the plan. This can offer lower monthly payments and prevent foreclosure. Retaining property is often a key goal for many debtors.

Unsecured debts, such as credit cards, may not be fully repaid. The plan can propose partial repayment based on the debtor's disposable income. This flexibility can provide much-needed financial relief.

Key Elements of a Repayment Plan:

- Prioritize and pay off priority debts.

- Restructure payments for secured debts.

- Propose manageable payments for unsecured debts.

An effective repayment plan can make a significant difference in achieving financial stability. It requires a careful assessment of current and future income. Consulting with a bankruptcy attorney can be beneficial in designing a successful plan.

North Carolina Bankruptcy Exemptions and Asset Protection

In North Carolina, bankruptcy exemptions play a crucial role in asset protection. These exemptions help safeguard specific assets from liquidation during bankruptcy. Understanding what you can keep is vital for strategic planning.

North Carolina provides specific exemptions which vary in protection levels. These include exemptions for a primary home, certain vehicles, and household goods. Knowing these can help in maintaining stability through the bankruptcy process.

Utilizing exemptions effectively can significantly impact your financial recovery. Exemptions aim to allow individuals to rebuild their lives post-bankruptcy. Having a clear understanding of your exempt assets is essential.

Common Exemptions in North Carolina:

- Homestead exemption for primary residences.

- Motor vehicle exemptions up to a certain value.

- Exemptions for household goods and personal property.

Properly leveraging these exemptions is key to retaining vital assets. Consulting with a bankruptcy attorney ensures you make informed decisions. This can provide peace of mind and facilitate a smoother bankruptcy process.

Benefits and Drawbacks of Filing Chapter 13 in North Carolina

Chapter 13 bankruptcy offers numerous benefits for debtors in North Carolina. One of the most significant advantages is the ability to retain your assets. Unlike Chapter 7, Chapter 13 provides a structured payment plan, allowing you to keep important possessions, like your home or car.

Another benefit is the automatic stay. This rule stops creditors from collecting debts once you file for bankruptcy. It provides immediate relief from creditor harassment, lawsuits, and wage garnishments. This can substantially reduce your stress and financial pressure.

However, Chapter 13 is not without its drawbacks. It requires a long-term commitment to a repayment plan that spans 3-5 years. During this period, you must consistently make payments, which can be challenging for some.

Additional drawbacks include a potential negative impact on your credit score. While bankruptcy can offer a fresh start, it may complicate future credit applications. Weighing these pros and cons is essential when considering Chapter 13 bankruptcy.

Key Benefits and Drawbacks:

- Benefits: Retain assets, automatic stay from creditors.

- Drawbacks: Long repayment commitment, impact on credit score.

Considering these factors will help you make an informed decision. Chapter 13 offers a viable path to financial recovery for many. However, assessing both sides of the coin is crucial before proceeding.

Costs, Fees, and Required Courses

Filing for Chapter 13 bankruptcy in North Carolina involves specific costs and fees. The filing fee for Chapter 13 is approximately $310. This fee can be burdensome, but options like fee waivers or installment plans might be available for those who qualify.

Aside from the filing fee, you will encounter other costs. Credit counseling and debtor education courses are required. These courses must be completed with approved providers to proceed with your case. They offer valuable insights into managing your finances post-bankruptcy.

Below is a summary of typical costs and required courses:

- Filing fee: Around $310

- Credit counseling course: Must be completed before filing

- Debtor education course: Needed before discharge

Considering these financial obligations and educational requirements is crucial. Understanding these can help you prepare adequately for the bankruptcy journey. Proper financial planning can minimize surprises along the way.

Life During and After Chapter 13 Bankruptcy

Living through Chapter 13 bankruptcy requires discipline and careful budgeting. You'll need to adhere to a court-approved repayment plan, which can stretch from three to five years. This means consistently making payments to a trustee who distributes funds to creditors.

Maintaining financial stability during this time is crucial. Many debtors find relief in knowing they can keep their assets, including homes and vehicles. However, it's essential to stay current on secured debts like mortgage or car loans to prevent foreclosure or repossession.

Completing a Chapter 13 plan offers a fresh financial start. It can improve your credit score over time and provide relief from overwhelming debt. Here's what life may look like after successfully completing the process:

- Improved credit score

- Discharge of eligible debts

- Ability to start rebuilding credit

- Freedom from creditor harassment

Filing Chapter 13 bankruptcy provides a structured path to recovery, but it requires commitment and focus.

When to Consult a North Carolina Bankruptcy Attorney

Considering Chapter 13 bankruptcy can be complex and stressful. Consulting a knowledgeable attorney is crucial. This step is especially important if you have intricate financial issues or large debts.

A legal expert can provide valuable guidance. They help in evaluating your situation and planning the best course of action. It ensures that all paperwork is accurate and filed on time. Seeking professional help early in the process can save time and prevent costly mistakes.

Conclusion: Is Chapter 13 Right for You?

Deciding on Chapter 13 bankruptcy is a big decision. It offers a chance to reorganize debt and protect assets. However, it also requires commitment and careful planning.

Evaluate your financial situation thoroughly. Consider your ability to adhere to a repayment plan. Consulting a bankruptcy attorney can provide clarity. They can help assess if this path aligns with your financial goals. Remember, Chapter 13 can offer a fresh start but requires a serious commitment to financial rehabilitation.

North Carolina Chapter 13 Success Stories

Saving a Home From Foreclosure in Raleigh

A Raleigh family facing foreclosure turned to chapter 13 bankruptcy to stop the sale of their home. By filing, they immediately triggered the automatic stay, which halted the foreclosure process. With the help of their trustee and a structured repayment plan, they were able to catch up on missed mortgage payments over five years while continuing to pay current bills. At the end of their plan, the family kept their home, discharged unsecured debts, and rebuilt their credit score with a stronger financial foundation.

Rebuilding After Job Loss in Charlotte

In Charlotte, a small business owner experienced unexpected job loss and mounting credit card debt. Filing chapter 13 allowed them to reorganize payments and protect a reliable vehicle essential for new employment. Their repayment plan restructured secured debts and reduced pressure from unsecured creditors. After successfully completing the plan, they restored their creditworthiness, secured steady employment, and achieved long-term stability while keeping vital assets intact.

Managing Medical Debt in Greensboro

A Greensboro couple burdened with overwhelming medical bills chose chapter 13 bankruptcy to regain control of their finances. Their trustee helped craft a plan that prioritized essential expenses while consolidating unsecured medical debts into manageable payments. Over the course of three years, they consistently made payments, avoided lawsuits from creditors, and preserved their home and personal property. Upon discharge, they were free from crushing medical debt and positioned to build a healthier financial future.

Frequently Asked Questions About Filing Chapter 13 in North Carolina

- Where do I file a Chapter 13 case in North Carolina?Chapter 13 cases are filed in the U.S. Bankruptcy Court for the district where you live—either the Eastern, Middle, or Western District of North Carolina.

- Are Chapter 13 hearings and 341 meetings in North Carolina held in person?Most 341 meetings are currently conducted by secure video conference, though the court can require in-person appearances when necessary.

- How long does a Chapter 13 repayment plan last in North Carolina?Plans typically run three to five years, depending on your income, household size, and the court’s confirmation of your proposed plan.

- Can Chapter 13 stop foreclosure on my North Carolina home?Yes, filing triggers the automatic stay, which halts foreclosure proceedings and allows you to catch up on past-due mortgage payments through your plan.

- What role does the Chapter 13 trustee play in North Carolina?The trustee reviews your petition, oversees the 341 meeting, collects your monthly payments, and distributes funds to creditors according to your confirmed plan.

- Will I lose my car or personal property in Chapter 13?Generally no—North Carolina’s exemption laws and the structure of Chapter 13 allow you to keep essential property while making repayment arrangements.

- Do I need an attorney to file Chapter 13 in North Carolina?While it is legally possible to file without an attorney, Chapter 13 is complex, and most debtors benefit greatly from the guidance of a North Carolina bankruptcy lawyer.

Get Bankruptcy Help for Your City in North Carolina

We’ve compiled helpful resources for individuals in major cities across North Carolina. Click below for localized information:

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin