Understanding Wisconsin Bankruptcy Laws and Procedures

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

When money is tight and bills keep piling up, trying to make sense of Wisconsin bankruptcy laws can feel overwhelming. Yet understanding how bankruptcy works in Wisconsin is one of the most important steps you can take if you’re seriously considering a fresh financial start.

Bankruptcy is a legal tool, not a moral judgment. It exists to give honest people in difficult situations a way to manage or eliminate debts they can no longer afford. Used correctly, it can stop lawsuit threats, collection calls, wage garnishments, and give you breathing room to rebuild.

Because bankruptcy is based on federal law but applied through Wisconsin-specific procedures, the process has layers. These rules are designed to balance the rights of people who need relief (debtors) with the rights of those who are owed money (creditors), so everyone is treated fairly under the law.

Two courts handle almost all bankruptcy Wisconsin cases: the US Bankruptcy Court Western District of Wisconsin and the Wisconsin Eastern Bankruptcy Court. Which court you file in depends on where you live, and each court follows detailed local rules and procedures that affect how your case moves forward.

Before you ever file, it’s critical to understand whether you qualify, which chapter makes sense for your situation, and what the “means test” is looking at. Eligibility, income, household size, and your mix of debts all matter when you’re deciding if, and how, to move ahead.

This guide walks through the major types of bankruptcy available to Wisconsin residents, explains how the courts and trustees fit into the process, and highlights key decisions you’ll face along the way.

By the end, you’ll have a clearer, step-by-step picture of how to file bankruptcy in Wisconsin and what to expect at each stage of the process.

Overview of Wisconsin Bankruptcy Laws

Wisconsin bankruptcy laws create the basic framework for debt relief in the state. They outline how individuals and small businesses can use bankruptcy to manage overwhelming debt, protect essential property, and work toward a financial reset.

Most of the rules come from federal law—Title 11 of the United States Code (the “Bankruptcy Code”)—but every bankruptcy Wisconsin case is also shaped by Wisconsin-specific procedures and exemptions. Many of the state exemption rules are collected in Chapter 815 of the Wisconsin Statutes, including the general personal property exemption statute (Wis. Stat. § 815.18) and the homestead exemption statute (Wis. Stat. § 815.20), which help determine what property you can protect or keep and how certain debts are treated.

What Property Protections Can Be Used in Wisconsin?

Exemptions are the laws that help determine what property you may be able to keep when you file bankruptcy in Wisconsin. Depending on the exemption system that applies, protection may be available for assets such as home equity, motor vehicles, household goods, tools used for work, and many retirement accounts, although limits and conditions still matter.

Wisconsin is not an opt-out state, so many filers may be able to choose between the Wisconsin exemption system and the federal bankruptcy exemptions. That choice can make a meaningful difference in how well your property is protected. Residency history can also affect which exemption rules apply. While people sometimes describe this using a 730-day rule, the actual analysis can be more complicated and depends on your domicile history before filing. For a fuller discussion, see our Wisconsin bankruptcy exemptions guide.

Bankruptcy Options in Wisconsin

For most people, the core choices under Wisconsin bankruptcy laws are between chapter 7 bankruptcy and chapter 13 bankruptcy. Each chapter follows a different process, has different eligibility rules, and leads to different outcomes for your debts and assets. There is also chapter 11, which is used primarily by business entities but is sometimes filed by individuals whose debts or assets are too large for chapter 13 limits.

Chapter 7 Bankruptcy in Wisconsin

For people who want to get rid of debt as quickly as possible, chapter 7 may be the most effective bankruptcy option. A successful chapter 7 case can wipe out many unsecured debts, including credit card balances, medical bills, and personal loans, often in just a few months. Debts tied to collateral, such as a home or vehicle, require a separate analysis because the lender’s rights in the property usually survive unless the collateral is surrendered or the debt is otherwise resolved through the bankruptcy process.

Before deciding whether chapter 7 is the right fit, it is important to look closely at the types of debt involved and whether they are actually dischargeable. Some obligations, such as recent taxes, many student loans, domestic support obligations, and debts arising from fraud or similar misconduct, may not be eliminated in a standard chapter 7 case.

Property issues also matter. In chapter 7, the trustee can review what you own and determine whether any nonexempt equity is available for creditors. If an asset has equity above the amount protected by applicable exemption law, that property could be at risk. That is why anyone considering chapter 7 in Wisconsin should evaluate both discharge issues and exemption planning before filing.

Do You Qualify for Chapter 7 Bankruptcy in Wisconsin?

One of the first steps in determining whether you may qualify for chapter 7 is comparing your household income to the Wisconsin median income for a household of your size. In many cases, if your current monthly income falls below the applicable median, you may pass the first part of the means test and move forward without having to complete the more detailed expense analysis.

For cases filed on or after November 1, 2025, the following Wisconsin median income figures apply:

| Household Size | Annual Median Income (USD) |

|---|---|

| 1 | $71,168 |

| 2 | $90,252 |

| 3 | $108,516 |

| 4 | $133,384 |

| Add $11,100 for each person over 4. | |

Effective for cases filed on or after April 1, 2026. Verify the latest figures here: UST Median Family Income by Family Size.

If your gross monthly average of income is not equal to or below Wisconsin's median income, it doesn't mean that you can't qualify gor chapter 7. It means that you have to move on to the next part of the means test. See our chapter 7 means test guide for more info on how this works.

Quick, low-stress way to start: Pull your last 6 months of income records (pay stubs, benefits statements, etc.). Add them up. The means test looks at a 6-month average and then annualizes it. If you’re unsure what counts as “income,” write that question down for a consultation—it’s common.

Chapter 13 Bankruptcy in Wisconsin

Chapter 13 is a repayment-based form of bankruptcy for people with regular income. Instead of seeking a quick discharge through chapter 7, the filer proposes a court-approved payment plan that usually runs for three to five years. Payments are made to the chapter 13 trustee, who distributes funds according to the terms of the confirmed plan.

In many cases, chapter 13 allows a person to pay only a portion of unsecured debt over time, rather than the full balance. The amount that must be paid depends on several factors, including income, reasonable living expenses, the value of nonexempt property, and the type of debt involved. After the plan is successfully completed, qualifying remaining unsecured debt may be discharged.

Chapter 13 vs. Chapter 7 Bankruptcy in Wisconsin

Chapter 13 can be especially helpful for Wisconsin filers who need time to protect important assets while catching up on missed payments through a court-approved repayment plan. Chapter 7 does not provide that same type of catch-up structure, so it may be a less flexible option for people who are behind on secured debts. For a more detailed comparison, see our chapter 7 vs. chapter 13 guide.

| Topic | Chapter 7 | Chapter 13 | Authority |

|---|---|---|---|

| Often a better fit for | People seeking faster relief from dischargeable unsecured debt, especially when income is lower and there is little or no nonexempt property at risk | People with regular income who need time to deal with arrears, protect property, or pay certain debts through a structured plan | 11 U.S.C. § 101(30); 11 U.S.C. § 109(e) |

| How long the case usually lasts | Usually about three to six months | Usually three to five years | 11 U.S.C. § 727(a); 11 U.S.C. § 1322(d) |

| What happens to property | Property that is not fully protected by applicable exemptions may be sold by the trustee to pay creditors | Filers usually keep their property, but the plan may need to account for any nonexempt value | 11 U.S.C. § 541; 11 U.S.C. § 726; 11 U.S.C. § 1325(a)(4) |

| Can it help you catch up on secured debt? | Not usually. chapter 7 does not provide a repayment plan for curing missed secured payments over time | Yes. Chapter 13 can allow arrears on secured debt to be cured through the repayment plan in many cases | 11 U.S.C. § 1322(b)(5) |

| Who can qualify | Qualification is affected by the means test, which compares income and allowed expenses | Individuals with regular income who meet the debt limits and other eligibility requirements can file chapter 13 | 11 U.S.C. § 707(b); 11 U.S.C. § 1325(b) |

| Main advantages | Can discharge many unsecured debts relatively quickly without requiring years of plan payments | Can help protect assets, address arrears over time, and provide a structured way to deal with debt | 11 U.S.C. § 362; 11 U.S.C. § 1322(b)(5) |

| Main drawbacks | Nonexempt property may be exposed to liquidation | Requires monthly payments for years, along with budget discipline and ongoing court supervision | 11 U.S.C. § 727(a); 11 U.S.C. § 1307 |

| How nondischargeable debts are treated | Debts such as child support, many taxes, and most student loans usually survive the case | These debts usually are not discharged, but some may be paid over time through the plan | 11 U.S.C. § 523(a) |

| Debt limits | No debt limits | Unsecured debts less than $526,700; secured debts less than $1,580,125 | 11 U.S.C. § 109(e); adjusted effective April 1, 2025 |

| Court filing fee | $338 | $313 | 28 U.S.C. § 1930; U.S. Courts fee schedule |

| When a prior bankruptcy can affect eligibility | Prior discharge timing rules can affect eligibility, often including an 8-year gap after a prior chapter 7 discharge and, in some situations, a 6-year gap after a prior chapter 13 discharge, subject to statutory exceptions. | Usually four years after a prior chapter 7 discharge, and two years after a prior chapter 13 discharge | 11 U.S.C. § 727(a)(8); 11 U.S.C. § 727(a)(9); 11 U.S.C. § 1328(f) |

The Role of Bankruptcy Courts in Wisconsin

When you file bankruptcy in Wisconsin, your case is handled in federal court, not state court. Every bankruptcy Wisconsin case is assigned to a U.S. Bankruptcy Court judge whose job is to apply federal law fairly to both debtors and creditors.

Two primary bankruptcy courts serve the state: the U.S. Bankruptcy Court for the Western District of Wisconsin and the U.S. Bankruptcy Court for the Eastern District of Wisconsin. Each court covers a specific group of counties and follows its own set of local rules and procedures, but both apply the same federal Bankruptcy Code.

Bankruptcy judges in these courts do much more than simply “approve” or “deny” a case. They review petitions, rule on motions, decide disputes, and make sure everyone follows the law—from debtors and creditors to attorneys and trustees.

Here is a brief breakdown of what the bankruptcy courts in Wisconsin typically do:

- Adjudicating bankruptcy petitions: Reviewing your filing, making sure it meets legal requirements, and entering key orders like the discharge or confirmation of a chapter 13 plan.

- Overseeing the bankruptcy estate: Working with the trustee on how assets are handled, how claims are treated, and whether proposed repayment plans comply with the law.

- Resolving disputes: Deciding disagreements between debtors and creditors, including objections to exemptions, plan terms, or the treatment of particular debts.

Understanding which Wisconsin bankruptcy court will handle your case—and what that court actually does—makes it easier to follow the process and communicate with your attorney. In the next sections, we’ll look more closely at the Western District and the Eastern District so you can see how each one is organized and where your case is likely to be filed.

Key Takeaways: Bankruptcy Courts in Wisconsin

- All bankruptcy Wisconsin cases are handled in federal court, by specialized U.S. Bankruptcy Courts rather than state courts.

- Wisconsin has two bankruptcy courts—the Western District and the Eastern District—and which one you use depends on where you live.

- Bankruptcy judges apply the federal Bankruptcy Code and related jurisdiction statutes, such as 28 U.S.C. § 1334 and 28 U.S.C. § 157, to hear and decide bankruptcy cases and related disputes.

- Knowing which court will oversee your case, and what that court does, is a key part of understanding how to file bankruptcy in Wisconsin and what to expect after your case is filed.

US Bankruptcy Court Western District of Wisconsin

The U.S. Bankruptcy Court for the Western District of Wisconsin handles bankruptcy Wisconsin cases for residents in the western half of the state, including areas around Madison, Eau Claire, La Crosse, and Wausau.

The court maintains staffed clerk’s offices in Madison and Eau Claire. Each location follows federal law as well as local rules and procedures published on the court’s official website: U.S. Bankruptcy Court — Western District of Wisconsin. Understanding where to file, how to contact the clerk’s office, and how to access hearing information is an important part of preparing to file bankruptcy in Wisconsin.

| Office | Address & Phone | Website |

|---|---|---|

| Madison (Main Office) | U.S. Bankruptcy Court Western District of Wisconsin 120 North Henry Street, Room 340 Madison, WI 53703-2559 Main Phone: (833) 758-0380 Case Information (VCIS): (866) 222-8029 | Court Locations — Western District |

| Eau Claire | U.S. Bankruptcy Court Western District of Wisconsin 500 South Barstow Street, Room 223 Eau Claire, WI 54701-3608 Main Phone: (833) 758-0380 In-person filing only — no mail accepted at this location. | Eau Claire Location — Official Site |

Filing in the Western District means following the court’s local rules, forms, and filing procedures, which are all available on the official website. Working with an experienced Wisconsin bankruptcy attorney can help you avoid common filing mistakes and make sure your case is filed in the correct division with the right supporting documents.

Wisconsin Eastern Bankruptcy Court

The U.S. Bankruptcy Court for the Eastern District of Wisconsin manages bankruptcy cases for residents in the eastern part of the state, including the Milwaukee metro area, Green Bay, the Fox Valley, and surrounding counties. Like the Western District, it handles cases under chapters 7, 11, 12, and 13 of the Bankruptcy Code.

The court’s main bankruptcy clerk’s office is in downtown Milwaukee, with additional hearing locations in Green Bay (and, in some instances, Oshkosh). County-by-county coverage is shown on the court’s jurisdiction map, which is a helpful tool for figuring out whether your case belongs in the Eastern District or the Western District.

The Eastern District follows the federal Bankruptcy Code and its own local rules and procedures, all available on the official website: U.S. Bankruptcy Court — Eastern District of Wisconsin. Before you file, it’s important to understand where to send documents, how to contact the clerk’s office, and which locations accept filings.

| Office | Address & Phone | Website |

|---|---|---|

| Milwaukee (Main Office) | U.S. Bankruptcy Court Eastern District of Wisconsin U.S. Federal Courthouse – Milwaukee 517 East Wisconsin Avenue, Room 126 Milwaukee, WI 53202 Main Phone: (414) 297-3291 Toll-Free: (866) 582-3156 Case Information (VCIS): (866) 222-8029 | Court Locations — Eastern District |

| Green Bay (Hearings Only) | U.S. Bankruptcy Court Eastern District of Wisconsin U.S. Federal Courthouse – Green Bay 125 S Jefferson Street Green Bay, WI 54301 Hearings only — no filings accepted at this location. Use the Milwaukee address for mail and in-person filings unless your attorney instructs otherwise. | Court Locations — Eastern District |

Filing in the Eastern District means following both national and local bankruptcy rules, using the correct forms, and paying close attention to filing instructions from the clerk’s office. An experienced Wisconsin bankruptcy attorney can help you determine whether the Eastern District is the right venue for your case and guide you through the specific procedures this court requires.

Key Takeaways: Wisconsin Eastern Bankruptcy Court

- The Eastern District of Wisconsin Bankruptcy Court handles cases from Milwaukee, Green Bay, and many surrounding counties, as shown on the court’s jurisdiction map.

- The main bankruptcy clerk’s office—and the place to file documents—is located in Milwaukee at 517 East Wisconsin Avenue, Room 126, with hearings also held at the Green Bay federal courthouse.

- Office hours, phone numbers, and filing instructions are kept current on the court’s official site at wieb.uscourts.gov, which should be your primary source for procedural updates.

Step-by-Step: How to File for Bankruptcy in Wisconsin

The filing process in Wisconsin starts in a similar way for both Chapter 7 and Chapter 13.

Step 1. Complete Credit Counseling

Before filing bankruptcy in Wisconsin, you generally must complete a credit counseling course from a provider approved by the U.S. Trustee Program. In most cases, the course must be completed within the 180 days before your case is filed. You should also use this stage to make sure you are practically prepared for the filing, including making arrangements for stable housing, reliable transportation, and a bank account that is not at risk of disruption during the case.

Step 2. Assemble Financial Documents

The next step is gathering the financial records needed to prepare your bankruptcy forms accurately. In most Wisconsin cases, that includes items such as recent pay stubs, tax returns, bank statements, creditor information, and other records showing your income, expenses, assets, and debts. Taking time to collect complete and up-to-date documents at the beginning can make the filing process smoother and reduce the risk of mistakes or missing information later.

Step 3. File in the Correct Wisconsin District

Once your forms are ready, file your case in the correct Wisconsin bankruptcy court. Depending on where you live, that will usually be either the Eastern District of Wisconsin or the Western District of Wisconsin. After filing, the automatic stay usually takes effect and can stop many collection actions.

Step 4. Attend the 341 Meeting of Creditors

After filing, you must attend the 341 meeting of creditors. You also must complete a debtor education course before you can receive a discharge. If you file Chapter 13, you must also complete the plan confirmation process and make the required plan payments.

Step 5. Receive the Discharge

If all required steps are completed, the court may enter a discharge order that eliminates eligible debts.

Step 6. After Filing for Bankruptcy in Wisconsin

After bankruptcy, the focus usually shifts to rebuilding financial stability. That may include reviewing your credit report, paying current bills on time, and building emergency savings so you are in a stronger position going forward.

The Role of the Bankruptcy Trustee and Other Key Players

After a bankruptcy case is filed in Wisconsin, a trustee is appointed to help administer the case. In Chapter 7, the trustee reviews your paperwork, conducts the 341 meeting, and determines whether any nonexempt property may be available for creditors. In Chapter 13, the trustee also reviews the repayment plan and helps administer plan payments.

Other important participants include the debtor, the debtor’s attorney, creditors, and the bankruptcy judge. Each has a different role, but together they move the case from filing through discharge or plan completion. Understanding who these parties are can make the Wisconsin bankruptcy process easier to follow and less intimidating.

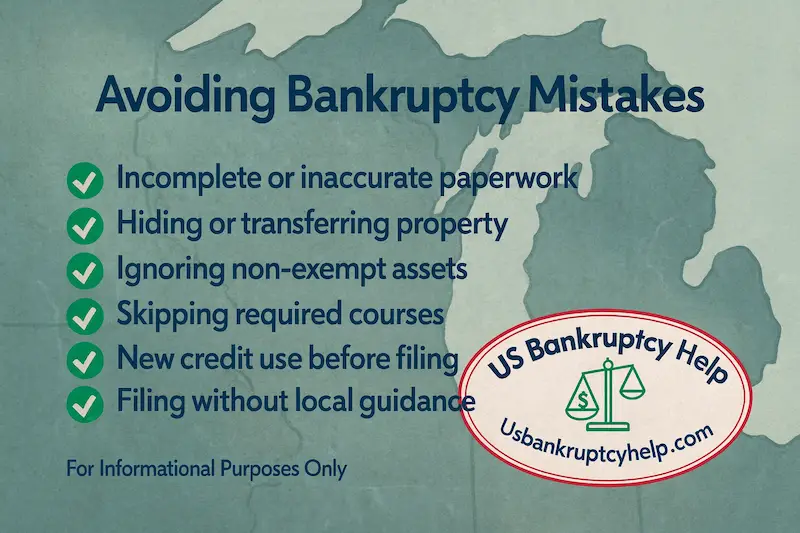

Common Mistakes and How to Avoid Them

Bankruptcy is a powerful tool, but small mistakes can cause big problems in a Wisconsin bankruptcy case—delays, extra hearings, or even dismissal. The good news is that most issues are preventable if you know what to watch out for and work closely with an experienced Wisconsin bankruptcy attorney.

Some of the most common mistakes include:

- Incomplete or inaccurate paperwork: Forgetting a creditor, leaving out an asset, or guessing at income and expenses can cause serious trouble. Everything in your petition and schedules is signed under penalty of perjury, so accuracy matters.

- Hiding or transferring property: Giving away assets, putting them in someone else’s name, or “selling” property for far less than it’s worth right before filing can be viewed as a fraudulent transfer. That can lead to objections, loss of exemptions, or even denial of discharge.

- Ignoring non-exempt assets: Assuming “no one will notice” something you own is risky. Your attorney needs a complete list of everything you own to correctly apply either Wisconsin or federal exemptions and to anticipate any issues with the trustee.

- Skipping required courses: The pre-filing credit counseling course and post-filing debtor education course are mandatory. If you miss them or fail to file the certificates, your case can be dismissed or you may not receive a discharge.

- Using credit or taking loans right before filing: Running up cards, taking cash advances, or financing big purchases immediately before a Wisconsin bankruptcy can lead to creditor challenges and claims of fraud, especially on luxury items or recent cash advances.

- Filing without local guidance: Trying to file pro se (without an attorney) in the Western or Eastern District of Wisconsin, while possible, can be overwhelming. Local rules, forms, and trustee expectations are detailed, and missing something simple can derail an otherwise good case.

Careful preparation, complete honesty with your attorney, and following the instructions from the Wisconsin bankruptcy court and trustee will prevent most of these problems. Before you file, talk openly with a Wisconsin bankruptcy lawyer about your assets, debts, and recent financial moves so they can help you avoid costly mistakes and keep your case on track.

Costs, Legal Help, and Resources for Bankruptcy in Wisconsin

Filing bankruptcy in Wisconsin usually involves court filing fees, required credit counseling and debtor education courses, and, if you hire one, attorney’s fees. The filing fees are set by federal law, and some filers may qualify to pay in installments or, in limited Chapter 7 cases, request a fee waiver.

Legal advice can be especially important if you have valuable property, higher income, recent transfers, tax issues, or questions about which exemption system to use. Some people may also qualify for free or lower-cost help through legal aid programs, lawyer referral services, approved counseling providers, and official bankruptcy court resources.

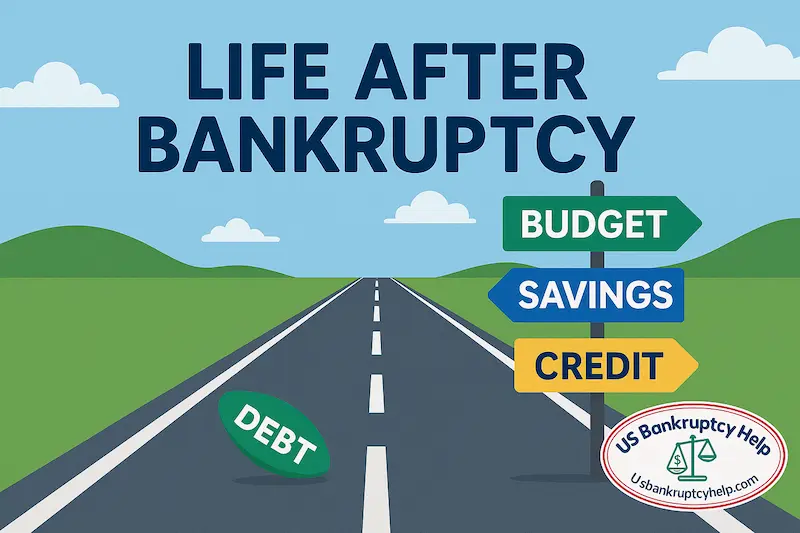

Life After Bankruptcy: Rebuilding and Moving Forward

Life after bankruptcy in Wisconsin is not about starting from zero—it’s about starting from a cleaner slate. The calls slow down, the pressure eases, and you finally have room to rebuild. The key is to be intentional about what you do with that fresh start so you don’t slip back into the same stress that led you to consider bankruptcy in the first place.

Your credit report will still show your bankruptcy for a number of years, but that doesn’t mean you are “locked out” of financial opportunities. Many people begin seeing offers for credit, car loans, and even mortgages sooner than they expect—what matters is how you handle new credit and your day-to-day money decisions after your case is over.

Some practical steps to rebuild after a Wisconsin bankruptcy include:

- Create a realistic, written budget: Track your income and essential expenses first (housing, utilities, food, transportation), then plan carefully for discretionary spending so you don’t drift back into using credit to fill gaps.

- Build a small emergency fund: Even a modest savings cushion in a separate account can help you handle surprise car repairs, medical bills, or seasonal expenses without reaching for a credit card.

- Monitor your credit reports: Check your reports regularly to confirm that discharged debts are reported correctly and to watch your progress as your score slowly improves over time.

- Rebuild credit slowly and intentionally: Many people start with a secured credit card or small credit-builder loan, use it for limited purchases, and pay the balance in full each month to show responsible use of new credit.

- Keep good records going forward: Saving pay stubs, tax returns, and key financial documents makes it easier to apply for housing, financing, or even future legal advice if you ever need it again.

A Wisconsin bankruptcy filing is not the end of your financial story; it is a turning point. With a clear budget, a focus on savings, cautious use of new credit, and guidance from professionals when you need it, it is possible to move from constant crisis back to stability and eventually to long-term financial goals like homeownership, retirement savings, and greater peace of mind.

Key Takeaways: Life After Bankruptcy in Wisconsin

- Bankruptcy gives you breathing room, but rebuilding requires new habits—especially around budgeting, saving, and using credit carefully.

- Monitoring your credit reports and starting small with secured credit or credit-builder tools can help you steadily improve your credit profile after a Wisconsin bankruptcy case.

- With time, patience, and consistent good decisions, many people are able to move from the stress that led them to bankruptcy toward a far more stable—and hopeful—financial future.

Frequently Asked Questions About Wisconsin Bankruptcy Laws

Bankruptcy in Wisconsin raises a lot of practical questions: Which court do I file in? Can I keep my house or car? How long will this stay on my credit? The answers depend on your specific situation, but these common questions can help you understand the basics before you talk with a Wisconsin bankruptcy attorney.

Do I file in the Western District or the Eastern District of Wisconsin?

Which Wisconsin bankruptcy court you use depends on where you live. The Western District of Wisconsin and the Eastern District of Wisconsin each have their own jurisdiction maps showing which counties they cover. Your attorney will confirm the correct court and file your case electronically in that district.

Can I keep my home or car if I file bankruptcy in Wisconsin?

Many people do keep their home and vehicle in a Wisconsin bankruptcy case, especially if they stay current on payments and use exemptions correctly. Whether you can protect these assets depends on:

- The amount of equity you have in the property.

- Whether you use Wisconsin exemptions under Chapter 815 of the Wisconsin Statutes or the federal exemptions under 11 U.S.C. § 522(d).

- Which chapter you file under (chapter 7 versus chapter 13) and whether you are curing arrears through a repayment plan.

A Wisconsin bankruptcy attorney will walk through your equity, loan balances, and exemption options before you file so you understand what is likely to happen with your home and vehicles.

How long will a Wisconsin bankruptcy stay on my credit report?

In general, a chapter 7 bankruptcy can appear on your credit report for up to 10 years, and a chapter 13 for up to 7 years, under national credit reporting standards. That does not mean your score is “frozen” the whole time—responsible use of new credit, on-time payments, and steady income can help your score improve well before those time periods expire.

Do both spouses have to file bankruptcy together in Wisconsin?

No. In Wisconsin, you can file individually or as a married couple, but because Wisconsin is a marital property state, the decision is more complex than simply “one or both.” How your assets and debts are titled, when they were incurred, and how Wisconsin marital property rules apply can all affect whether a joint or individual filing makes more sense. This is a key issue to discuss with a Wisconsin bankruptcy lawyer before you file.

Will I have to go to court in person?

Most people never appear in front of a bankruptcy judge. In a typical Wisconsin consumer case, your only required appearance is the “meeting of creditors” (also called a 341 meeting), which is conducted by the trustee, not the judge. Depending on current procedures in the Western or Eastern District, that meeting may be held by phone, video, or in person. Your attorney will tell you when and how to appear and what to expect.

Do I really need a Wisconsin bankruptcy attorney?

The law does not require you to hire an attorney, but the Bankruptcy Code, Wisconsin exemption choices, and local court rules are complex. An experienced Wisconsin bankruptcy lawyer can:

- Help you decide whether chapter 7, chapter 13, or another option is appropriate under Wisconsin bankruptcy laws.

- Make sure your case is filed in the correct Wisconsin bankruptcy court with complete and accurate schedules.

- Protect as much property as possible using the exemption system that best fits your assets.

A short consultation with a Wisconsin bankruptcy attorney can often save you from costly mistakes and give you a much clearer picture of what bankruptcy would look like in your specific situation.

Navigating Bankruptcy in Wisconsin

Learning how bankruptcy works in Wisconsin is an important step toward making a more informed decision about your financial future. Whether you are considering Chapter 7 or Chapter 13, the process involves federal law, exemption rules, and local court procedures that can affect the outcome of your case.

Good information and careful planning can make the process easier to understand and help you avoid costly mistakes. For many people, getting advice about eligibility, exemptions, assets, and chapter choice is an important part of protecting a fresh start.

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin