Chapter 7 Bankruptcy Georgia: Your Guide to a Fresh Start

Georgia Chapter 7: Quick Summary

- Exemption system: Georgia is an opt-out state—most filers use Georgia exemptions (see O.C.G.A. § 44-13-100). Jump to Georgia exemptions.

- Median income: Use the Georgia median income table (sourced from the U.S. Trustee Program’s means testing data).

- Where you file: Georgia has three federal bankruptcy districts— Northern, Middle, and Southern. Jump to Where you file in Georgia.

- Means test basics: Eligibility is income/expense driven. See our means test overview and the official UST means testing page.

- For the full national walkthrough (process, timelines, courses, and key terms), see Chapter 7 bankruptcy.

If you’d like help applying this information to your own situation, you can review your options below.

If you’re dealing with collection calls, lawsuits, or wage garnishments in Georgia, it can be hard to know where to start. This page is designed to give you a clear, people-first overview of chapter 7 in Georgia—what’s different here (Georgia exemptions, median income figures, and where you file), what the usual steps look like, and where to verify key information using official sources.

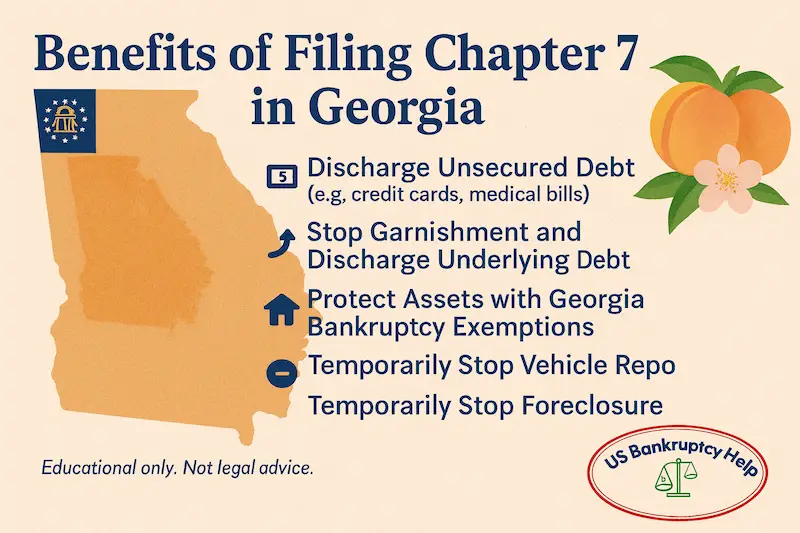

What’s Different in Georgia for Chapter 7

If you’re considering chapter 7 in Georgia, the two things that most often change your experience are (1) which exemption rules protect your property and (2) where your case is filed. This section highlights the Georgia-specific pieces first, then points you to the detailed guides for the broader federal steps and terminology.

- Georgia uses its own exemption system: Georgia is an opt-out state, which generally means Georgia exemptions apply in Georgia-based cases. The main Georgia exemption statute is O.C.G.A. § 44-13-100 (and the federal exemptions framework is in 11 U.S.C. § 522). If you want the practical “what does this protect?” breakdown, start here: Georgia bankruptcy exemptions.

- Your filing location is one of three federal districts: Georgia is divided into the Northern, Middle, and Southern Districts. Where you file is tied to where you live (and sometimes where you lived recently). Jump to Where you file in Georgia to see the official district links.

- Income comparisons use Georgia’s median income figures: A common first checkpoint is whether your household income is below the Georgia median for your household size. You can jump to the Georgia median income table and verify the source data on the U.S. Trustee Program site: justice.gov/ust/means-testing.

- Some cases don’t use the standard means-test pathway: This page already notes two commonly discussed situations—when debts are not primarily consumer debts and certain disabled-veteran circumstances. For plain-language context and definitions, see our means test overview.

- If you moved recently, exemptions can get more complicated: The page mentions the “730-day domicile rule.” In real life, that’s a signal to slow down and double check which state’s exemption rules apply based on timing and residency. For broader background, link out here: national Chapter 7 guide.

If you’re trying to decide what to look at next, a practical order is: (1) review Georgia exemptions, (2) compare your household size to the Georgia median income table, and (3) confirm your filing district. Then use the national Chapter 7 guide for the step-by-step process and common terms.

Georgia Median Income Snapshot

This table is here because it’s part of the chapter 7 means test—a screening tool used to evaluate eligibility. Many people start by comparing their household size to the Georgia median income because it’s a quick first checkpoint. If you’re under the median, you often clear the income portion of the means test. If you’re over the median, that does not automatically mean you can’t file chapter 7—many people still qualify after the full means-test calculation (which accounts for certain allowed expenses), and some cases may fall under exceptions.

How to use this table (and what it does not mean)

- Step 1: Pick your household size and find the matching Georgia median income number below.

- Step 2: Compare it to your 6-month average gross income (the means test looks at a defined income period rather than just “this month”).

- If you’re below: that’s often a strong sign you pass the income checkpoint.

- If you’re above: you may still qualify after applying allowed expenses in the full means-test calculation. You can read the step-by-step explanation here: means test guide.

- Exceptions: some cases may bypass the standard means-test pathway (this page discusses common examples like primarily non-consumer debt and certain disabled-veteran circumstances).

The U.S. Trustee Program publishes the official median income figures used for means testing, and the numbers update periodically. The table below reflects the Georgia thresholds for cases filed on or after November 1, 2025.

| Household Size | Annual Median Income |

|---|---|

| 1 | $66,722 |

| 2 | $82,787 |

| 3 | $98,877 |

| 4 | $120,315 |

| Add per person over 4 | + $11,100 |

Median income figures are based on the U.S. Trustee Program’s Census Bureau Median Family Income by Family Size table for Georgia, effective for cases filed on or after November 1, 2025. For the most current data, see justice.gov/ust/means-testing.

If you want the bigger picture—what happens after filing, common terms, and the usual sequence of steps—see the national Chapter 7 overview.

Exemptions and Chapter 7 in Georgia

A key Georgia-specific issue is what property is protected during a chapter 7 case. The protection rules are called “exemptions,” and in Georgia they come from Georgia law. In practice, people usually start here because exemptions affect common concerns like keeping a home, a car, everyday household items, and retirement funds.

Georgia is an opt-out state—if you’re eligible to use Georgia exemptions, you generally use the Georgia set rather than choosing the federal exemptions. The primary Georgia exemptions statute is O.C.G.A. § 44-13-100. For additional context on how exemptions work within the Bankruptcy Code, see 11 U.S.C. § 522.

If you want a practical, plain-language breakdown of common Georgia exemption categories and how they’re typically used, start here: Georgia bankruptcy exemptions.

Common Georgia Exemption Categories

The list below is a high-level map of what Georgia’s exemptions often cover. Exact eligibility and how exemptions apply can depend on your facts (like ownership, equity, and timing).

- Homestead: protections related to a primary residence (home equity).

- Motor vehicle: protections related to vehicle equity.

- Household goods & clothing: everyday household items up to certain limits.

- Wildcard: a flexible category that can sometimes protect a range of property depending on what you own.

- Retirement accounts: many tax-qualified retirement accounts are commonly treated as protected under bankruptcy rules.

- Personal injury & health aids: certain awards and medically necessary aids may be protected within limits.

If your main concern is a home or car, the next section focuses on those two items first. You can also jump straight to the Georgia exemptions hub here: Georgia bankruptcy exemptions.

Protecting a Home and Car

For many people, the biggest questions are simple: “Can I keep my home?” and “Can I keep my car?” In a chapter 7 case, the answer often depends on equity (the value minus what you owe) and whether that equity fits within Georgia’s exemptions.

Georgia’s exemptions are set out in O.C.G.A. § 44-13-100. For a practical breakdown of the main categories (including home and vehicle), see Georgia bankruptcy exemptions.

Home: What usually matters

- Home equity: Exemptions typically protect up to a certain amount of equity in a primary residence. If your equity is above what the exemption protects, that can raise additional issues in a chapter 7 case.

- Payment status: Separate from exemptions, keeping a home with a mortgage often relates to staying current on the loan and understanding how the lender’s lien works.

- Timing and recent transfers: Big changes right before filing (selling, gifting, or refinancing) can complicate things, so it’s worth checking the details carefully.

Car: What usually matters

- Vehicle equity: If you own the car outright, the exemption typically focuses on how much equity is protected. If you have a loan, equity is usually the car’s value minus the loan balance.

- Loan vs. lien: A discharge eliminates eligible personal liability, but liens on collateral can still matter. Understanding what that means for a car loan is an important step in planning.

- Insurance and registration: In the real world, staying insured and keeping paperwork current can be part of keeping a vehicle usable during and after the case.

Real-life example (simple equity math)

Here’s a simplified example to show how exemptions and equity can connect. Imagine someone in Georgia owns:

- A home worth $260,000 with a mortgage balance of $245,000(about $15,000 in equity), and

- A car worth $14,000 with a loan balance of $11,500 (about $2,500 in equity).

If Georgia’s homestead and vehicle exemptions cover at least those equity amounts, the filer may be able to claim exemptions to protect that equity. If equity is higher than what an exemption protects, that’s when people typically slow down and get clarity on options and tradeoffs—especially for a home.

Note: This is an illustration of how equity is calculated—not a prediction of outcomes. Exemptions and results depend on your exact facts (ownership, valuations, liens, timing, and other details).

If you’d like to compare your property categories against Georgia’s exemption rules, start here: Georgia bankruptcy exemptions. For the broader national overview of how chapter 7 works, see Chapter 7 bankruptcy.

Where You File in Georgia

If you’re trying to figure out “which court do I use?”, you’re not alone. Chapter 7 cases in Georgia are filed in the U.S. Bankruptcy Court, and Georgia is split into three federal districts. The goal of this section is to help you quickly identify the right district and get you to the official court resources (addresses, phone numbers, local rules, filing guidance, and forms).

Step 1: Find your Georgia bankruptcy district

In most situations, your district is based on where you live. If you’ve moved recently, venue can involve additional rules (and this page covers the official starting points below rather than guessing). If you’re unsure, use the court sites to look up locations and contact the clerk’s office.

- Northern District of Georgia — Official court website (local rules, filing locations, clerk contact info, forms)

- Middle District of Georgia — Official court website (local rules, filing locations, clerk contact info, forms)

- Southern District of Georgia — Official court website (local rules, filing locations, clerk contact info, forms)

Step 2: Use the court site for the practical details

Once you’re on the correct court’s website, you can usually find the information people need most, such as:

- Filing locations & hours (where the clerk’s office is and how to reach it)

- Local rules and procedures (district-specific requirements)

- Forms and self-help information (where available)

- Telephonic/video appearance guidance (when the court provides it)

If you want a reliable, plain-language overview of what happens after filing (automatic stay, the trustee’s role, required courses, and the typical sequence of steps), see the national Chapter 7 guide.

What to Expect in a Georgia Chapter 7 Case

People usually feel the most stress when they don’t know what comes next. Below is a practical, plain-language overview of what a typical chapter 7 timeline can look like in Georgia. This is not meant to cover every exception—rather, it’s a “map” so you can understand the usual sequence and know what to read next.

A Straightforward Chapter 7 Roadmap

- Check the means test starting points: Many people begin by comparing their household size to Georgia’s median income table and reviewing means-test basics (income and allowable expenses).

- Identify what property is protected: Review Georgia’s exemption categories (home, car, household goods, retirement) and estimate equity so you understand what’s at stake.

- Confirm where you file: Georgia has three federal districts (Northern, Middle, Southern). The court’s official site is the best source for local procedures and filing information.

- Complete the required courses: Chapter 7 involves a pre-filing credit counseling course and a post-filing debtor education course through approved providers. Official lists are published by the U.S. Trustee Program.

- File the case and get the automatic stay: Filing typically triggers an automatic stay that stops most collection activity while the case is pending (with important exceptions in some situations).

- Work with the trustee: The trustee reviews paperwork and commonly requests documents (often things like pay information, bank statements, and tax returns) so the case can move forward.

- Attend the 341 meeting: This is a required meeting where the trustee asks questions to confirm the information in the filings. Many meetings are brief for straightforward cases, but procedures can vary.

- Finish the debtor education course and wait for the discharge: If the case proceeds without major issues, the court can enter a discharge order after required steps are completed.

Helpful official resources

- U.S. Courts overview of chapter 7: Chapter 7 bankruptcy basics

- U.S. Trustee Program approved course providers: Credit counseling & debtor education info

- U.S. Trustee Program means testing source: Means testing

If you want the complete walkthrough (documents, timelines, common issues, and key terms), see the national Chapter 7 guide.

Georgia Chapter 7 FAQs People Ask Most

These FAQs focus on the questions Georgia residents most commonly ask when they’re trying to understand chapter 7: what it can and can’t do, how long it usually takes, and how exemptions relate to homes, cars, and everyday property. For official background, you can cross-check the process overview at U.S. Courts (Chapter 7 basics).

Do I need a lawyer to file chapter 7 in Georgia?

Some people file without a lawyer (often called “pro se”). Chapter 7 paperwork can be detailed, and Georgia-specific exemptions and local court procedures can matter. If you’re deciding what to do, a practical approach is to compare (1) the complexity of your situation (home equity, car equity, recent moves, taxes, or business income) against (2) your comfort with preparing detailed financial forms and meeting deadlines.

Will I lose my house or car if I file?

Many filers are able to keep essential property, but it depends on equity and how exemptions apply. Georgia is an opt-out state, so Georgia exemptions often control what is protected. A good first step is to estimate equity (value minus what you owe) and then review the main exemption categories here: Georgia bankruptcy exemptions.

How long does a chapter 7 case usually take?

Many straightforward cases run for a few months from filing to discharge, but timing varies by court schedules and case details. For an official baseline overview of the usual sequence, see U.S. Courts (Chapter 7 basics).

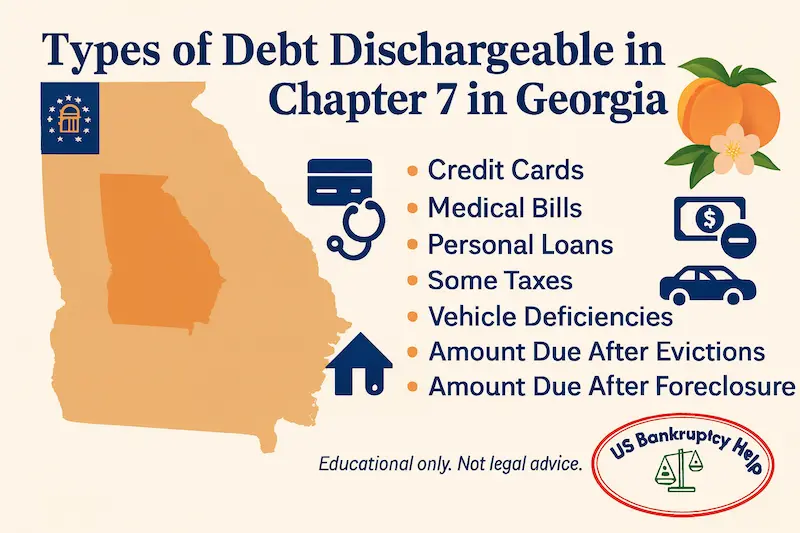

Which debts generally aren’t discharged?

Some categories of debt can be harder to discharge, even in chapter 7. The Bankruptcy Code’s nondischargeability rules are in 11 U.S.C. § 523. Commonly discussed examples include domestic support obligations and certain tax debts, among others.

What are the required courses?

Chapter 7 includes two separate course requirements: a pre-filing credit counseling course and a post-filing debtor education course. The U.S. Trustee Program publishes the approved provider lists here: approved providers.

Where do I file in Georgia?

Georgia has three bankruptcy districts (Northern, Middle, Southern). The most reliable way to confirm the correct court and procedures is to start with the official district sites in Where you file in Georgia.

Want the full walkthrough in one place (process, documents, and key terms)? See the national Chapter 7 guide.

Next Steps and Options

If you’re feeling overwhelmed, it can help to narrow your next step to something concrete and low-friction. The checklist below is designed to help you get organized and focus on the parts of a Georgia chapter 7 case that most often affect outcomes: exemptions, income/means testing, and filing district.

A practical next-step checklist

- Start with exemptions: Make a short list of what you own that matters most (home, car, savings, tax refund expectations, retirement). Then review Georgia exemptions and estimate equity (value minus what you owe).

- Compare income to the Georgia median table: Use the Georgia median income snapshot and, if needed, cross-check the official source at justice.gov/ust/means-testing.

- Confirm where you file: Identify your district (Northern, Middle, or Southern) and use the official court site for procedures and clerk contact info (see Where you file in Georgia).

- Review the means test basics: If you want a plain-language explanation of how income and allowable expenses are considered, see our means test guide.

- Understand required courses (official list): If you’re reading ahead, the U.S. Trustee Program publishes approved providers for credit counseling and debtor education here: approved providers.

If you want the full walkthrough

For a complete, step-by-step explanation of chapter 7 (including what happens after filing, common terms, and the typical sequence of events), visit Chapter 7 bankruptcy.

Reminder: This page is educational and focuses on reliable sources and Georgia-specific differences (exemptions and filing location). Individual outcomes can vary based on facts like equity, timing, and local procedures.

Trust and Source Notes

We aim to make this page easy to verify. Below are the key official sources used for the Georgia-specific numbers and rules on this page, plus the court sites for “where you file.”

Primary sources used on this page

- Georgia exemptions statute: O.C.G.A. § 44-13-100

- Means testing data (official): U.S. Trustee Program — Means Testing

- Approved course providers (official): U.S. Trustee Program — Approved Providers

- Federal court overview: U.S. Courts — Chapter 7 basics

- Bankruptcy Code sections cited on-page: 11 U.S.C. § 362, 11 U.S.C. § 522, 11 U.S.C. § 523 (Cornell LII)

Georgia court sites

Prefer one complete walkthrough? Visit the national Chapter 7 guide.

Explore Our Georgia Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin