Chapter 7 Bankruptcy California: A Practical Guide

- What this page covers: California-specific points that commonly matter in Chapter 7, including choosing between California’s two exemption systems (703 vs. 704), a California median-income snapshot used in the means test starting point, and where cases are filed in California’s federal bankruptcy courts.

- Primary sources used: We link to official sources whenever possible—such as the U.S. Trustee Program median-income tables, California courts forms (including exemption amount references), and controlling federal code sections when residency/domicile rules apply.

- Keep data current: Some figures (like median income and exemption limits) can change. We provide effective dates and link out to the official source tables and statute/form pages so you can verify the latest information.

Chapter 7 in California — Summary

This California page focuses on the parts that are most state-specific—especially choosing between California’s two exemption systems (703 vs. 704), the California median-income snapshot used in the means test starting point, and where cases are filed in California’s federal bankruptcy courts. For the federal overview and nationwide rules, see the Chapter 7 bankruptcy national guide.

- Exemption system: California generally requires choosing one of two exemption systems (703 or 704), which affects what property may be protected.

- Median income jump: Go to California median income snapshot for the current table by household size and the official source link.

- Where you file jump: See where you file in California for the official court/venue info by district.

- State exemptions link: Use California bankruptcy exemptions for the current categories and official references.

- National guide link: For process basics, discharge overview, and common FAQs, visit Chapter 7 bankruptcy.

See if your property is protected by California exemptions →

What’s Different in California for Chapter 7

If you’re trying to figure out whether Chapter 7 makes sense in California, the “California part” usually comes down to three practical questions: do I qualify, what property can be protected, and where would a case be filed. This section keeps the focus on those real-world decision points and links to official sources for anything that can change.

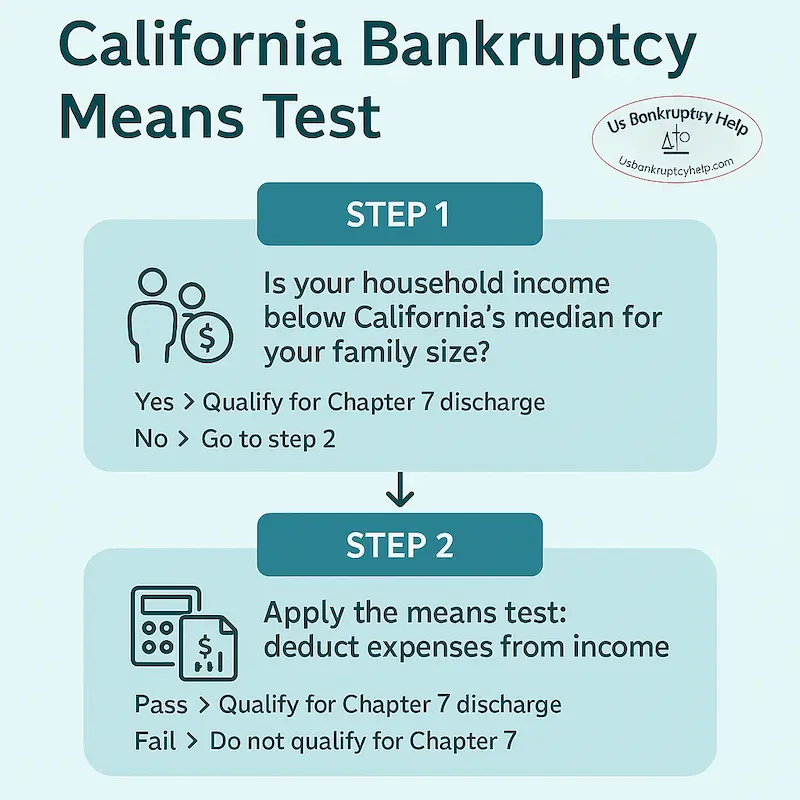

- Do I qualify? California median income is the first checkpoint: A common starting point is comparing income to California median-income figures published by the U.S. Trustee Program (these tables are updated over time). Use the official table here: U.S. Trustee Program median income table (cases filed on or after Nov 1, 2025). For the table on this page, jump to California median income snapshot.

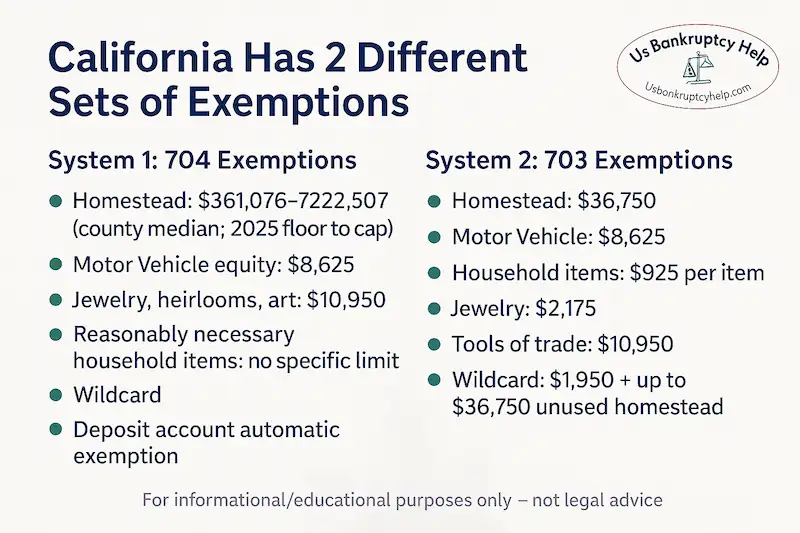

- You must choose an exemption system (703 or 704): California has a two-system exemption setup. The system you pick affects what property may be protected—especially for homeowners vs. renters and for people who need more flexibility for personal property. Official starting points include CCP § 704.730 and the California courts exemption amounts reference Form EJ-156. If you want the plain-English breakdown by category, see California bankruptcy exemptions.

- Home and car protection depends on that choice: The homestead and vehicle exemptions can work differently under 703 vs. 704. Because exemption limits can be updated, any specific number you see on this page should be paired with an effective date and an official statute or court-form link so you can verify it.

- Residency can affect which state’s exemptions apply: If you moved recently, federal law has a look-back rule that may affect which state’s exemptions you use. For the controlling language, see 11 U.S.C. § 522(b)(3)(A).

- Where you file depends on your California district: Chapter 7 cases are filed in federal bankruptcy court within the correct California district. Jump to Where You File in California for official court links and district tools.

California Median Income Snapshot

If you’re asking “do I qualify for Chapter 7 in California?”, the first quick check many people start with is the California median income for your household size. The U.S. Trustee Program updates these figures over time, so the most helpful approach is to use the table that matches your filing-date range and confirm it using the official source link below.

Important: Being above the median income does not automatically mean you can’t file Chapter 7. Median income is a starting point, and the means test includes additional steps and allowed deductions that may still apply. For the full overview, see our Chapter 7 bankruptcy guide and our means test guide.

Effective for cases filed on or after November 1, 2025. Source: U.S. Trustee Program median income table

| Household Size | Annual Median Income (USD) |

|---|---|

| 1 | $77,221 |

| 2 | $100,161 |

| 3 | $113,553 |

| 4 | $135,505 |

| Add $11,100 for each person over 4. | |

For the latest table links and effective dates, see U.S. Trustee Program — Means Testing.

Exemptions in Chapter 7 in California

One of the biggest worries people have is, “Will I lose my stuff?” Exemptions are the rules that answer that question. They describe what property can be protected in a Chapter 7 case—things like household items, a vehicle, retirement accounts, and (for many people) some home equity, depending on the exemption system used.

California generally uses its own exemption rules instead of the federal exemption list (often called the “opt-out” approach). Because exemption limits can change, we link to official sources and effective dates so you can double-check the current numbers.

- California uses California exemptions (opt-out): Official reference: CCP § 703.130.

- Two exemption systems (choose one): California has two exemption “packages,” commonly referred to as 703 and 704. The choice can change how home equity, car equity, and personal property are treated, and the systems aren’t designed to be mixed.

- Where official amounts and effective dates are listed: California courts publish a reference document listing exemption dollar amounts and effective dates. See Form EJ-156.

- California exemptions by category (plain-English overview): For a quick breakdown of the main categories people ask about (home, car, household goods, retirement, and more), see California bankruptcy exemptions.

- Keep information current: Exemption limits and court reference documents can be updated. When this page lists a specific number, it should be paired with an effective date and an official source link so readers can verify the latest figures.

Protecting a Home and Car

For many people, the two biggest questions are: “Can I keep my home?” and “Can I keep my car?”In California Chapter 7 cases, the answer usually depends on (1) the equity you have and (2) which California exemption system you choose (703 vs. 704). Because exemption limits can change, we link to official sources so you can verify the current rules and amounts.

- Home (homestead): California’s homestead protection is in the California Code of Civil Procedure. A key official starting point is CCP § 704.730. If you see a specific dollar figure on any page, confirm the current limit and effective-date details using an official source.

- Car (vehicle): Vehicle exemptions can differ depending on whether you use 703 or 704. One official reference point is CCP § 704.010. For the 703-system amounts and effective dates commonly referenced by courts, see Form EJ-156.

- Choosing 703 vs. 704 changes what “fits” best: The two systems are different exemption packages. If you’re trying to compare how each one treats home equity, car equity, and personal property, start here: California bankruptcy exemptions.

- Keep the numbers current: Exemption limits can be updated. When a page lists specific amounts, it should include the effective date and link back to the official statute or court form so you can confirm the latest figures.

Where You File in California

Bankruptcy cases are filed in federal bankruptcy court. California is divided into four bankruptcy court districts, and the right district depends on where you live. The court sites below include official district maps, division locations, and (in some districts) tools to look up the correct filing location.

- Northern District of California: canb.uscourts.gov (official site) — use the Locations Map to find the correct divisional office by county.

- Eastern District of California: caeb.uscourts.gov (official site) — see District Map and Court Locations for courthouse addresses and division information.

- Central District of California: cacb.uscourts.gov (official site) — use the Court Locator to find the correct division and filing location.

- Southern District of California: casb.uscourts.gov (official site) — the court provides district information and location details on its website.

- Looking up a bankruptcy case: PACER Case Locator can be used to search federal court cases (account required).

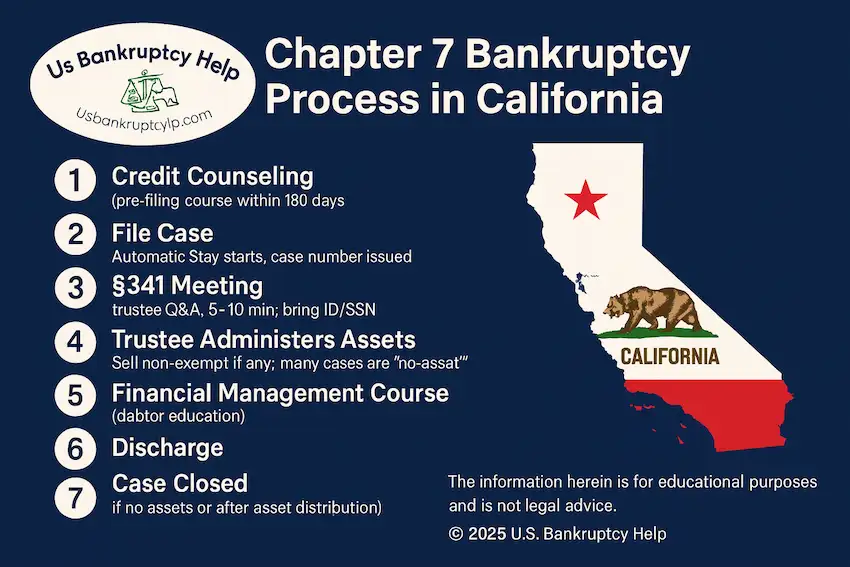

Chapter 7 Bankruptcy in California: The Process Overview

Chapter 7 is a federal court process with standard steps nationwide. Below is a quick, people-first overview so you know what to expect, followed by a link to our full guide for the longer explanations and current details.

- Prepare and file: A case starts by filing bankruptcy forms that list income, debts, assets, and recent financial history.

- Automatic stay: Filing typically triggers an automatic stay that stops many (but not all) collection actions while the case is pending.

- Trustee review: A court-appointed trustee reviews the paperwork and looks for non-exempt property (property not protected by exemptions).

- 341 meeting: Most filers attend a short “meeting of creditors” where the trustee asks questions to confirm the filing is accurate.

- Discharge (when applicable): If the case moves forward without issues, the court can enter a discharge order for eligible debts after required steps are completed.

For a deeper walkthrough (including required courses, common exceptions to discharge, and what can happen with non-exempt property), see our Chapter 7 bankruptcy guide.

California Chapter 7 FAQs

These FAQs highlight common California-specific questions people ask when researching Chapter 7—especially around timing, exemptions, home protection, and how filing affects collections.

How long does a Chapter 7 case usually take in California?

Many Chapter 7 cases move from filing to discharge in a matter of months, but timing can vary based on court workload, whether additional documents are requested, and whether any issues are raised in the case.

Will I lose my home if I file for Chapter 7 in California?

Whether a home is protected usually depends on your home equity and which California exemption system you use (703 vs. 704). California’s homestead rules are set out in the California Code of Civil Procedure (see CCP § 704.730), and the specific amounts can change over time.

What property is protected under California’s Chapter 7 exemptions?

Exemptions commonly cover categories like household goods, clothing, some vehicle equity, retirement accounts, and (in many cases) home equity—depending on whether you use the 703 or 704 system. For a category-by-category overview, see California bankruptcy exemptions. For official exemption amounts and effective dates used for the 703 system, see Form EJ-156.

Do both spouses have to file Chapter 7 together in California?

No. A married person can file individually, and some couples file jointly. In California, community property rules can affect what is considered part of the bankruptcy estate and how debts and assets are treated, so filings can look different depending on how property and debts are held.

How does Chapter 7 affect my credit in California?

A Chapter 7 bankruptcy can remain on a credit report for a number of years under credit reporting rules, and the practical impact varies by person. Many people focus on rebuilding by checking reports for accuracy, keeping current accounts in good standing, and building a realistic budget after the case.

Can Chapter 7 stop wage garnishments in California?

Filing a Chapter 7 case typically triggers an automatic stay that can stop many collection actions, including many wage garnishments, while the case is pending. Some actions may be exempt from the stay depending on the type of debt and the circumstances.

What debts cannot be discharged in a California Chapter 7?

Some debts are commonly not discharged in Chapter 7, such as certain recent taxes, domestic support obligations, and many student loans. The full list depends on the type of debt and the facts of the case. For a federal overview of common discharge exceptions, see our Chapter 7 bankruptcy guide.

Next Steps and Options

If you’re researching Chapter 7 bankruptcy in California, the most helpful next step is usually to confirm two things: (1) which California exemption system fits your situation (703 vs. 704) and (2) which California federal court district you would file in. The resources below are designed to help you verify the current rules using reliable sources.

- Review California exemptions (703 vs. 704): California bankruptcy exemptions.

- Verify the current California median-income table: U.S. Trustee Program — Means Testing.

- Full federal overview of Chapter 7: Chapter 7 bankruptcy guide.

- Alternative option: If Chapter 7 isn’t a fit, learn how Chapter 13 works here: Chapter 13 bankruptcy guide.

About This California Chapter 7 Guide

Our goal is to make this page helpful, reliable, and people-first. We prioritize primary sources and clearly mark information that can change (like median income tables and exemption amounts), so readers can verify the latest details.

- Author and updates: This page includes a named author and a visible “Last updated” date above.

- Primary sources we rely on: We link to official sources such as the U.S. Trustee Program and California court and statute pages whenever possible.

- Median income (official tables + effective dates): U.S. Trustee Program — Means Testing (includes current median-income tables and effective dates).

- California exemption law (official statute reference): California Legislative Information — Codes.

- Exemption amounts reference (official court material): California Courts — Form EJ-156.

Explore Our California Bankruptcy Guides

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin