Understanding Chapter 13 Bankruptcy in Ohio

Every year, thousands of Ohioans use chapter 13 bankruptcy to reorganize their debts under court supervision. Ohio is divided into the Northern and Southern Districts, and while each judge and trustee may handle cases a little differently, the core chapter 13 rules come from the federal Bankruptcy Code and apply statewide.

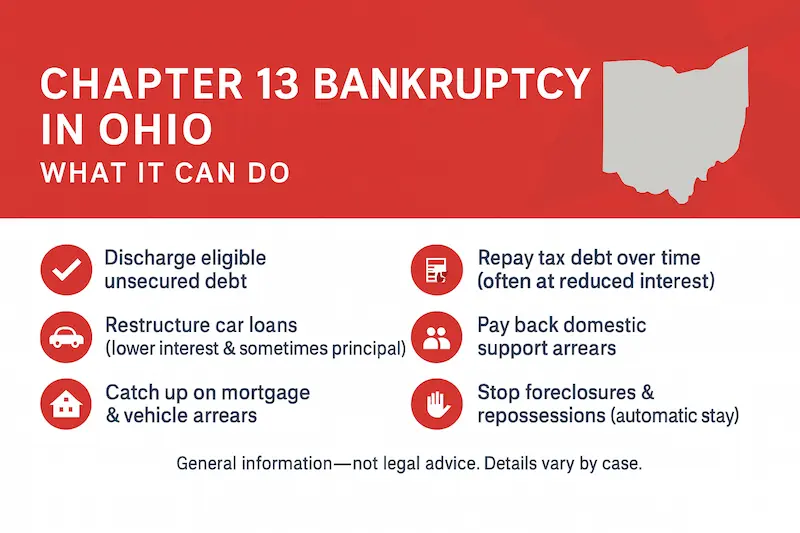

In Ohio, chapter 13 is often used not only to obtain a discharge of qualifying unsecured debts, but also to catch up on mortgage arrears, stop vehicle repossessions, restructure car loans, and pay back priority debts (such as certain taxes and domestic support obligations) that are not easily handled in chapter 7. It can also be a way to keep non-exempt property that might be at risk in a straight liquidation case.

Chapter 13 in Ohio involves proposing a court-approved repayment plan that usually lasts three to five years. Your monthly payment is made to a chapter 13 trustee, who then distributes funds to creditors according to the confirmed plan. In many cases, the automatic stay can stop a pending foreclosure or repossession, and the co-debtor stay may help protect qualifying co-signers on consumer debts while the case is active.

Filing for chapter 13 requires careful preparation. You will need to provide detailed information about your income, expenses, debts, assets, and recent financial history so a feasible plan can be proposed and confirmed by the court. Working with an experienced bankruptcy attorney who regularly practices bankruptcy in Ohio can make the process smoother and help you avoid costly mistakes.

Ohio's specific bankruptcy laws and Ohio bankruptcy exemptions play a major role in chapter 13. They influence how much must be paid to unsecured creditors and whether you can keep certain property while still obtaining a discharge. Understanding how exemptions, your budget, and the chapter 13 “best efforts” and “best interests of creditors” tests all fit together is vital to getting the full benefit of your case. This guide will walk you through the key steps so you can make informed decisions.

What Is Chapter 13 Bankruptcy in Ohio?

In Ohio, Chapter 13 Bankruptcy is a 3 to 5 year payment plan where you pay your "disposable income" to a chapter 13 trustee. The trustee takes your payments, and distributes them according to your confirmed chapter 13 plan that you filed with your petition. After this plan period is over, you are eligible for a discharge of general unsecured debts (like credit cards and medical bills for example).

The chapter 13 plan can propose to pay back certain debts in full, like priority debts (certain taxes and domestic support obligations), and secured debts (like a mortgage or car loan). The plan can also propose to pay back general unsecured debts at a percentage of what is owed, or everything that is owed, or even nothing at all. The amount you pay into your chapter 13 plan is based on your income and expenses. The amount you have to pay to unsecured creditors that are subject to discharge is based on your income, expenses, and the value of non-exempt assets you own.

Key Benefits of Chapter 13 in Ohio

Chapter 13 is a diverse chapter of bankruptcy that offers several key benefits for those who are facing major financial challenges. Here are some of the main advantages:

Stop Foreclosure and Catch Up on Mortgage Arrears

If you are behind on mortgage payments, filing a chapter 13 could stop a foreclosure, and allow you to catch up on payments over the 3 to 5 year plan payment period.

Catch Up on Vehicle Arrears

If you are behind on car payments, Chapter 13 allows you to pay vehicle arrears through your chapter 13 plan.

Pay Back Priority Debts

Many chapter 13 filers use chapter 13 as a way to pay back debts like taxes and domestic support obligations that are not dischargeable in bankruptcy.

Protect Co-Signers

Chapter 13 protection extends to co-debtors on consumer debts, protecting them from creditor actions.

Asset Protection

If you have assets that are not exempt or are partially exempt, chapter 13 allows you to keep these items as you can pay the nonexempt amount through your chapter 13 plan.

Examples of How a Chapter 13 Case Could Work in Ohio

Here are some examples of how a chapter 13 case would work in Ohio:

Example 1: Catching Up on Mortgage Arrears

Steve, a small business owner in Springfield, fell behind on his mortgage payments because of a downturn in business. Steve gets a foreclosure notice from his mortgage lender stating the amount Steve is behind is $25,000. Steve files for Chapter 13 and proposes a plan that pays back the $25,000 mortgage arrears. He and his lawyer file his case a day before the foreclosure date. They properly give notice of filing to the mortgage lender and their attorneys. In this case, not only is Steve able to stop the foreclosure process by filing before the foreclosure date, but Steve was able to pay back the $25,000 arrearage and come out of the plan completely caught up.

Example 2: Paying Back Priority Debts, Vehicle Arrears and Discharging Unsecured Debt

Linda, a realtor in Cincinnati files 3 years of back tax returns and discovers that she owes the IRS $33,000 in non-dischargeable taxes. She is also 2 months behind on her Infiniti payment and has $85,000 in credit card debt. Linda files for chapter 13 protection just before her car is repossessed in front of her townhouse. She proposes a chapter 13 plan that pays back 100% of her tax debt at 0% interest, and pays her car off at the fair market value, rather than the value that is owed, through a Chapter 13 cram down. Her plan proposes payment to her credit cards for approximately 1% of what they are owed. Sue continues making payments for 5 years, and after successfully completing her plan, the court enters a discharge. Linda comes out with a clean vehicle title, owing no taxes and is credit card debt free.

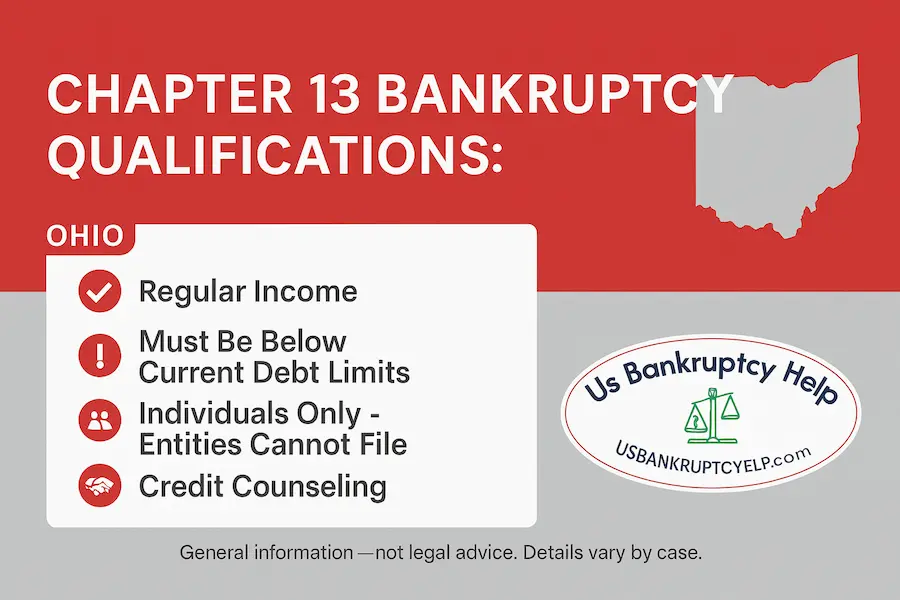

Eligibility Requirements for Chapter 13 in Ohio

To qualify for Chapter 13 Bankruptcy in Ohio, you need to meet specific criteria. Understanding these requirements is essential before proceeding with the filing process.

Regular Income

Chapter 13 can't work without plan payments. If you don't have a regular source of income, you probably won't be able to make plan payments. Therefore, you must have a regular income to make plan payments.

Debt Limits

There are limitations on the amount of secured and unsecured debts you can have in chapter 13. As of April 1, 2025, your secured debts must not exceed approximately $1,580,125, while unsecured debts must be under roughly $526,700.

Tax Filings

You must be current with your tax filings. This means you should have filed all required tax returns preceding your bankruptcy filing.

Credit Counseling

You must have completed a credit counseling course before filing. The counseling course is valid for 180 days and you will be given a certificate of completion that usually has to be submitted with the chapter 13 petition.

Meeting these criteria paves the way for a smoother Chapter 13 bankruptcy process. It positions you for potential financial recovery and stability.

The Chapter 13 Bankruptcy Process in Ohio

Filing chapter 13 bankruptcy in Ohio involves several detailed steps. Each phase is an important step in the process.

Credit Counseling

I know, we may be beating a dead horse here, but you have to do credit counseling within 180 days before you file. Moving on!

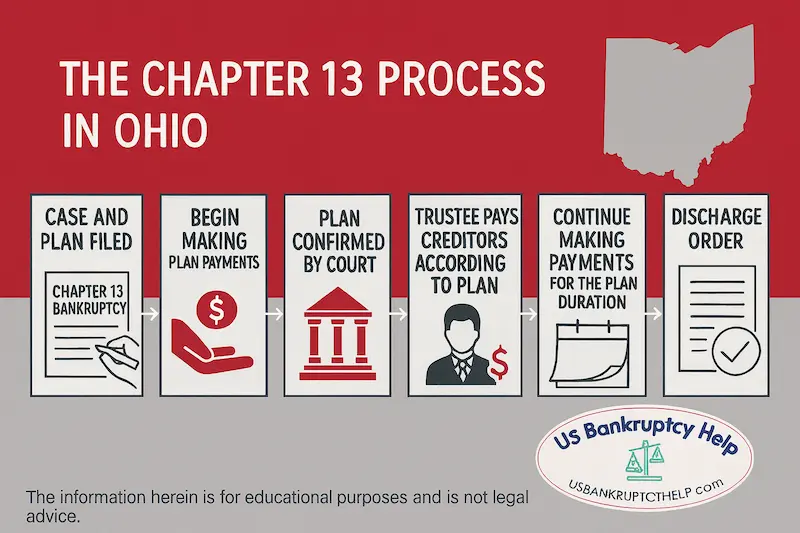

Filing the Petition, Plan and the Automatic Stay

You and your Ohio bankruptcy lawyer should have done a lot of work up to this point. Most chapter 13 cases file the chapter 13 plan with their petition. This starts the entire process, and also gives you the automatic bankruptcy protection (the "automatic stay") that stops creditors and allows you to reorganize.

341 Meeting - AKA the Meeting of Creditors

This is a meeting that you and your bankruptcy attorney will have with your chapter 13 trustee who is assigned to your case. While it's called "meeting of creditors", it is rare for creditors to attend the meeting. These meetings are usually conducted remotely (over the phone or via Zoom).

Plan Confirmation

After you file your plan, creditors and the trustee have an opportunity to review it and object to anything in it. Once this time period is over, you either file a stipulation with the court to have your plan confirmed, or there is a confirmation hearing on the plan, and the court confirms it. In the vast majority of cases, the trustee and any creditors who object to the plan stipulate to confirmation, once objections are resolved.

Making Plan Payments

Plan payments usually begin 30 days after the case is filed, and continue for the duration of the plan. When you make the final plan payment the trustee usually notifies the court of the plan's completion. At that point you are eligible for discharge (if your plan calls for it).

Discharge

After you make all plan payments, you are eligible for a discharge of any remaining unsecured debt that is subject to discharge. You must also complete a debtor education course (almost like the credit counseling course) before you can receive your discharge.

If you are considering chapter 13 in Ohio, keep these steps in mind so you can mentally prepare for what lies ahead. Understanding each phase can reduce stress and increase your confidence in successfully navigating the chapter 13 bankruptcy process.

Essential Ohio Bankruptcy Information & Resources

Discover how bankruptcy in Ohio can help you eliminate debt, protect your property, and move toward financial stability under Ohio and federal law.

Chapter 13 vs. Chapter 7 Bankruptcy in Ohio: What’s the Difference?

When considering chapter 13 bankruptcy, you probably want to know the difference between it and Chapter 7, the most widely filed chapter of bankruptcy. In Ohio, these two types of bankruptcy serve distinct purposes and suit different financial situations.

Chapter 7 provides you with a fast discharge of unsecured debts (like credit cards and medical debt). In chapter 7, if you have an asset that is not exempt, the chapter 7 trustee must reconcile that asset, by selling the asset, or settling the asset. The proceeds from this process are distributed to creditors to mitigate their losses. In contrast, in Chapter 13 bankruptcy you can pay what is not exempt over the 3 to 5 year plan period and avoid losing anything.

Both chapters have their pros and cons. Obviously in chapter 13 you also get the benefits we've discussed above. It's important to understand these differences so that you can make an informed decision that works best for you and your family.

You can find out more about the the differences between chapter 7 and chapter 13 by readings some of our other resources on the topic.

The Role of the Bankruptcy Trustee and the Court

In Chapter 13 Bankruptcy, the trustee plays a crucial role. They oversee the entire process, ensuring compliance with the repayment plan. This impartial figure is responsible for collecting payments and distributing them to creditors according to the approved plan.

The bankruptcy court is equally important. It approves your repayment plan and monitors the case's progress. Here's what the trustee and court do:

- Review your financial documents

- Conduct the meeting of creditors

- Ensure compliance with the Chapter 13 plan

Both the trustee and the court work to balance debtor relief with creditor rights, ensuring a fair and legal process.

Ohio Chapter 13 Trustees & Contact Information

Ohio has separate Chapter 13 standing trustees by district and division. Your assigned trustee depends on where your case is filed (Northern or Southern District, by division). Always follow the instructions in your official Notice of Bankruptcy Case.

Northern District of Ohio

| Division | Trustee | Website |

|---|---|---|

| Cleveland | Lauren A. Helbling — Chapter 13 Trustee | 13trusteecleveland.com |

| Akron | Keith L. Rucinski — Chapter 13 Trustee | chapter13info.com |

| Canton | Dynele L. Schinker-Kuharich — Chapter 13 Trustee | chapter13canton.com |

| Toledo | Elizabeth A. Vaughan — Chapter 13 Trustee | chapter13toledo.com |

| Youngstown | Michael A. Gallo — Chapter 13 Trustee | chapter13youngstown.com |

Southern District of Ohio

| Division | Trustee | Website |

|---|---|---|

| Columbus | Faye D. English — Chapter 13 Trustee | ch13columbus.com |

| Columbus / Eastern Division | Edward A. Bailey — Chapter 13 Trustee | ch13.org |

| Cincinnati | Margaret A. Burks — Chapter 13 Trustee | 13Network — Cincinnati Trustee |

| Dayton | John G. Jansing — Chapter 13 Trustee | dayton13.com |

Common Ohio Trustee Procedures

- • Plan payments usually start 30 days after your case is filed (even before confirmation).

- • Payments are often made through TFS Bill Pay (online portal/eWage) or by mailing to the trustee’s lockbox shown on your notice.

- • Never mail cash; use a cashier’s check or money order and include your full name and case number.

- • Keep tax returns, pay stubs, and insurance current; promptly provide any documents your trustee requests.

- • 341 meetings are commonly held by phone or video; your notice provides exact connection instructions.

Always adhere to your specific trustee's requirements. If anything is not clear, contact your attorney or visit the trustee's website. For the most current list of Ohio Chapter 13 standing trustees, see the U.S. Trustee Program – List of Chapter 13 Standing Trustees.

Is Chapter 13 Bankruptcy Right for You?

Getting through Chapter 13 Bankruptcy in Ohio involves commitment and careful financial management. Making those plan payments is tough. Daily life might involve budgeting more diligently. However, you'll not only get the relief you need, but learn some important financial skills along the way.

If you can tough it out in chapter 13, you're most likely going to be the beneficiary of substantial economic relief. With determination, you can emerge in a stronger financial position.

Deciding whether Chapter 13 bankruptcy is suitable for you involves careful consideration. Evaluate your current financial situation and long-term goals. Consulting with an Ohio bankruptcy attorney who can provide clarity on your best options. This process can be a strategic move towards regaining financial stability and protecting your vital business operations.

Ohio Chapter 13 Bankruptcy FAQs

What Is Chapter 13 in Ohio and Who Does It Help?

Chapter 13 in Ohio is a court-supervised repayment plan that lets individuals with regular income reorganize debt over three to five years. It’s often a fit for people who need to stop a foreclosure, catch up on a mortgage or car, pay priority debts like certain taxes or domestic support, and still keep important assets while working toward a discharge of eligible unsecured debt at the end of the plan.

Can Chapter 13 Stop a Foreclosure in Ohio and Help Me Catch Up?

Yes. Filing chapter 13 triggers the automatic stay, which generally pauses foreclosure activity. Your plan can spread past-due mortgage amounts over the life of the case while you resume regular payments going forward. Many Ohio homeowners use chapter 13 specifically to cure arrears and save their homes.

How Are Chapter 13 Plan Payments Calculated in Ohio?

Plan payments are based on your disposable income (what’s left after reasonable living expenses), the type of debts you owe (priority, secured, and unsecured), and the value of any non-exempt property under Ohio bankruptcy exemptions. The trustee reviews your budget and documents, and the court confirms a payment amount that’s feasible and compliant with the Bankruptcy Code.

What Are the Current Eligibility Limits for Chapter 13 in Ohio?

Chapter 13 has debt caps that apply nationwide. As of April 1, 2025, unsecured debts must be under roughly $526,700 and secured debts must be under approximately $1,580,125. These amounts are adjusted periodically, so verify the latest figures before filing.

Will I Keep My Business, Home, and Car in an Ohio Chapter 13?

In many cases, yes. Chapter 13 is designed to protect assets while you repay. You can keep operating a small business, cure mortgage arrears, and address vehicle arrears or even pay a car through the plan. How much you must pay unsecured creditors can be influenced by Ohio exemption amounts and your budget.

What Should I Expect at the 341 Meeting and Who Is My Trustee in Ohio?

The 341 “meeting of creditors” is an interview with your chapter 13 trustee about your finances and plan; creditors rarely appear. In Ohio, your trustee is assigned by district and division (Northern or Southern District). Many divisions conduct these meetings by phone or video—your official notice provides the exact instructions.

How Do I Make Chapter 13 Payments in Ohio and What Happens After I Finish?

Most Ohio trustees accept electronic payments through approved services (such as online portals) or via a designated lockbox—never send cash, and always include your full name and case number. After you complete all plan payments and required courses, you’re typically eligible for a discharge of remaining eligible unsecured debts, giving you a fresh financial start.

Explore Our Ohio Bankruptcy Guides

Explore Some of Our National Bankruptcy Guides

- Chapter 7 Bankruptcy: National Guide

- Chapter 13 Bankruptcy: National Guide

- Chapter 7 vs Chapter 13 Bankruptcy: National Guide

- Can Just One Spouse File Bankruptcy?

- Can You File Bankruptcy and Keep Your House?

- Can You File Bankruptcy and Keep Your Car?

- How Often Can You File Bankruptcy?

- Chapter 13 Vehicle Cramdown