What Happens When You File for Bankruptcy

How This Article Was Reviewed▾

How We Review This Educational Content▾

Why You Can Trust This Page▾

When you file a bankruptcy case, the court opens a case, assigns a case number, appoints a trustee, and begins notifying creditors by mail. The automatic stay is usually triggered right away, which can stop many collection actions while the case is pending. After that, what happens depends on whether you file chapter 7 or chapter 13.

Filing starts the bankruptcy process, but the next steps depend on the type of bankruptcy you choose. Some steps are similar in most consumer bankruptcy cases, while others depend on the chapter you file. Here we discuss what generally happens when you file for bankruptcy and what is different in chapter 7 vs chapter 13.

What Happens When You Declare Bankruptcy?

Declaring bankruptcy means filing a bankruptcy petition in bankruptcy court. This is the first formal step in the bankruptcy process. Once the petition is filed, several important things happen quickly.

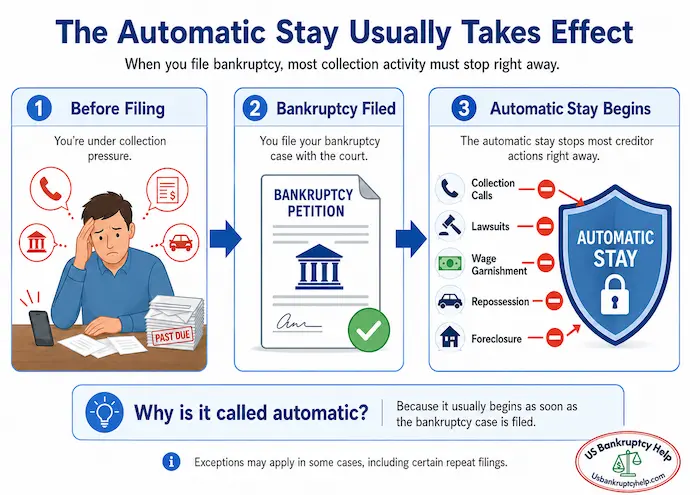

1. The Automatic Stay Takes Effect

The first thing that happens when you file bankruptcy is that the automatic stay takes effect. The automatic stay is a legal protection that stops creditor activity like, collection calls, lawsuits, wage garnishments, repossessions, and foreclosures.

This protection is called “automatic” because it begins automatically when the bankruptcy case is filed. There is no required to get this protection. However, there may be exceptions to this protection, also known as the “stay”, and the stay may be limited if you filed previous bankruptcy cases within a certain period of time.

Example of the Automatic Stay

Assume Ted is behind on his mortgage payments and a foreclosure sale is scheduled for Thursday. Ted files a chapter 13 bankruptcy case on Wednesday, one day before the foreclosure sale, and proper notice is given to the mortgage lender and foreclosure attorney. In many cases, the foreclosure sale must stop because the automatic stay is now in place.

2. A Bankruptcy Case Number Is Assigned

After a bankruptcy case is filed, the bankruptcy court assigns a case number to the case. This number is important because it identifies your bankruptcy case. Creditors, attorneys, the trustee, and the court use the case number to track filings, notices, deadlines, and activity in your case.

If a creditor contacts you after filing, you or your attorney may give the creditor the bankruptcy case number so the creditor can update its records. In many cases, creditors also receive formal notice of the bankruptcy from the court.

3. A Bankruptcy Trustee Is Appointed

Usually within 24 hours of a case being filed, a bankruptcy trustee is assigned to it.

In chapter 7 bankruptcy, the trustee reviews your bankruptcy paperwork and determines whether there are any nonexempt assets that can be administered for creditors.

In chapter 13 bankruptcy, the trustee reviews your proposed repayment plan, collects plan payments, distributes money to creditors under the confirmed plan, and may object to the plan if it doesn't meet bankruptcy requirements.

4. The 341 Meeting of Creditors Is Scheduled

After your case is filed, the court schedules a 341 meeting of creditors. This is called the 341 meeting because it comes from section 341 of the Bankruptcy Code.

The meeting of creditors is conducted by the trustee who is assigned to your case. The trustee asks you questions about your bankruptcy paperwork, income, expenses, assets, debts, transfers, and other financial information, under oath. Creditors are allowed to appear and ask questions, but in the majority of chapter 7 and chapter 13 cases they don't.

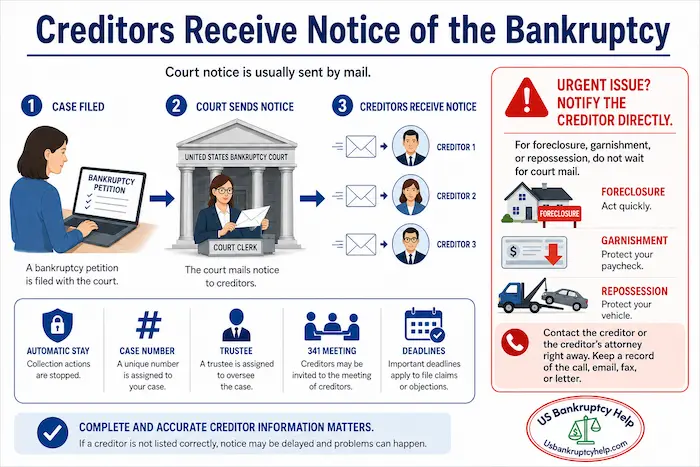

5. Creditors Receive Notice of the Bankruptcy

Creditors listed in your bankruptcy paperwork generally receive notice that the case has been filed. This notice tells creditors about the bankruptcy filing, the automatic stay, the case number, the trustee, the meeting of creditors, and important deadlines.

On your petition, complete and accurate creditor information matters. If a creditor is not properly listed, the creditor may not receive notice of the bankruptcy case. This could lead to complications, such as a debt not being discharged or a creditor continuing collection activity.

6. Your Property, Debts, Income, and Expenses Are Reviewed

The trustee reviews your financial picture. This includes your assets, debts, income, expenses, recent transfers, lawsuits, tax refunds, vehicles, real estate, bank accounts, and other property.

The purpose of this review is to determine what you own, what you owe, what property is protected by exemptions, whether creditors may receive anything, and whether you qualify for the bankruptcy relief you are requesting.

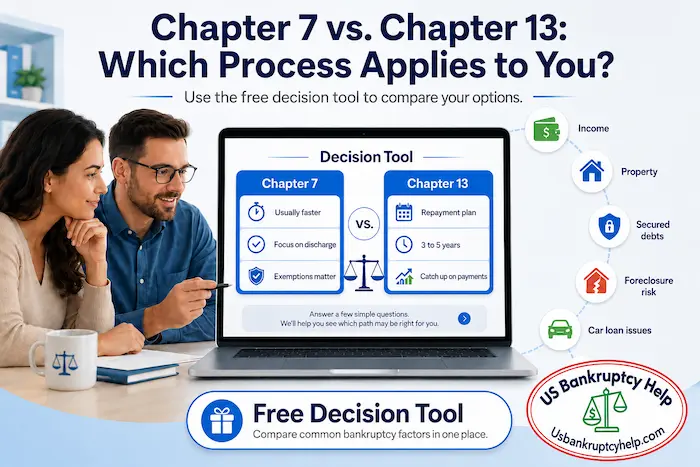

Chapter 7 vs. Chapter 13: Which Process Applies to You?

While chapter 7 and chapter 13 have similar procedures, what happens after you file bankruptcy depends on which chapter you choose. Chapter 7 is usually faster and focuses on discharge, exemptions, and whether the trustee can administer any nonexempt property. Chapter 13 usually lasts longer and focuses on a court-approved repayment plan.

Your choice of chapter 7 or chapter 13 depends on your unique financial situation. If you are not sure which bankruptcy process fits your situation, you can use the free chapter 7 vs. chapter 13 decision tool below. It can help you compare common factors like income, property, secured debts, foreclosure risk, car loan issues, and whether you need time to catch up on missed payments.

Chapter 7 vs Chapter 13 Decision Tool

Answer a few questions to get an educational estimate of which bankruptcy chapter may fit your situation.

Step 1 of 2

Window 1 of 2: Income Snapshot

ZIP lookup is optional and used as a quick state check.

What Happens in Chapter 7 Bankruptcy?

Chapter 7 is usually the faster type of consumer bankruptcy. After the case is filed, the automatic stay begins, a trustee is appointed, the meeting of creditors is scheduled, and the trustee reviews the case.

The Trustee Reviews Whether You Have Nonexempt Property

The chapter 7 trustee reviews your schedules, statements, property, debts, income, expenses, and recent financial activity. This review can include whether you own nonexempt property, whether you made recent transfers, whether you paid family members or other insiders, and whether there are other issues that need to be addressed in the bankruptcy case.

Most Chapter 7 Cases Move Toward Discharge

If there are no issues, most chapter 7 cases move toward discharge after the meeting of creditors and after the deadline passes for objections. A discharge is the court order that eliminates your personal liability for many qualifying debts.

What Happens in Chapter 13 Bankruptcy?

Chapter 13 involves a 3 to 5 year payment plan and discharge isn't entered until this plan is completed.

You Start Making Chapter 13 Plan Payments

In chapter 13, you usually must start making plan payments within 30 days of the case being filed. These payments are made to the chapter 13 trustee, who later distributes funds to creditors according to the confirmed plan.

The Court Reviews Whether the Plan Can Be Confirmed

Chapter 13 includes a confirmation process. Confirmation means the bankruptcy court approves the repayment plan. Before confirmation, the trustee and creditors may object to the plan.

If there are objections, you and your attorney will either modify the plan, negotiate with creditors, or respond to objections. When there are no objections that need to be resolved, the court usually confirms the plan. After this, the case continues and the debtor must keep making plan payments.

Chapter 13 Discharge Usually Comes After Plan Completion

Not every chapter 13 case receives a discharge. For example, some cases pay creditors in full. However, in chapter 13, the discharge usually comes at the end of the case, after the debtor completes all required plan payments. This makes chapter 13 very different from chapter 7, where discharge often happens much sooner.

Explore Urgent Bankruptcy Questions and Answers

What Happens to Your Debts When You File Bankruptcy?

Filing bankruptcy does not instantly erase all debts. The filing starts the case and usually triggers the automatic stay. The discharge, if entered, is what eliminates your personal liability for qualifying debts.

Some debts may be discharged. Some debts aren't dischargeable. Debts like secured debts (mortgages and car loans), may require ongoing payments if you want to keep the property. The result depends on the debt and the chapter filed.

What Happens to Your Property When You File Bankruptcy?

When you file bankruptcy, your property becomes part of the bankruptcy case, called the "bankruptcy estate". This does not automatically mean you lose your property. Many people who file bankruptcy keep all of their property because bankruptcy exemptions protect it.

The risk of losing property depends on the chapter you choose, the value of your property, the liens against it, and available exemptions.

What Happens After the Bankruptcy Case Is Over?

After the case ends, the effect depends on the chapter. In chapter 7, a successful case usually ends with a discharge and case closing. In chapter 13, a successful case usually ends after completion of the repayment plan, entry of discharge, and case closing.

After bankruptcy, you may still need to rebuild credit, maintain payments on debts that survived the case, and keep records of your bankruptcy discharge. Bankruptcy can provide powerful relief, but it is a legal process with deadlines, duties, and consequences.

Frequently Asked Questions About Filing Bankruptcy

What Does Filing for Bankruptcy Mean?

Filing for bankruptcy means submitting a bankruptcy petition to the bankruptcy court to start the legal bankruptcy process. This filing does not automatically mean your debts are wiped out, and it does not mean the case is finished. It means the bankruptcy process has officially started.

Once a bankruptcy case is filed, the court assigns a case number and appoints a bankruptcy trustee. Creditors listed in the case are notified through the mail, and the automatic stay (bankruptcy protection) usually takes effect immediately.

Filing is usually done electronically through the US Bankruptcy Court's electronic filing system (ECF), or can usually be done in person at the clerk's office at your local bankruptcy court.

Do I have to go to court when I file bankruptcy?

The majority of bankruptcy cases don't require an appearance in bankruptcy court. However, most filers are required to attend a meeting of creditors (often called a 341 meeting), where a bankruptcy trustee asks questions about the information in the bankruptcy documents. Currently most of these meetings are held remotely or telephonically.

Will creditors stop contacting me after I file bankruptcy?

When a bankruptcy case is filed, a legal protection called the automatic stay generally stops many debt collection efforts while the case is pending. This may include collection calls, lawsuits, and wage garnishments. However, some types of legal actions may continue, and creditors may request permission from the court to proceed in certain circumstances.

What Disqualifies You From Filing Bankruptcy?

Most people aren't disqualified from filing bankruptcy. However, sometimes there can be issues that could prevent you from receiving a discharge, delay when you can file again, or make one chapter of bankruptcy unavailable. For example, you may have a problem if you recently received a bankruptcy discharge, filed a case in bad faith, hid assets, lied on your bankruptcy paperwork, ignored court requirements, or failed to complete required credit counseling.

There are also rules that are specific to the chapter you choose to file. In chapter 7 for example, if you have a higher income, you may have to pass the means test. In chapter 13, you need regular income to fund the chapter 13 plan, and debt limits also apply. These rules don't mean you can never file bankruptcy, but they may determine which chapter is available, whether the automatic stay is available, and whether the court can grant a discharge.

Final Thoughts on What Happens When You File Bankruptcy

After filing bankruptcy the automatic stay usually takes effect, a case number is assigned, a trustee is appointed, creditors receive notice, and a meeting of creditors is scheduled. What happens next depends on whether you file chapter 7 or chapter 13.

Bankruptcy can be a powerful tool, but it is also a legal process with rules, deadlines, and consequences. Before filing, it is important to understand which chapter may fit your situation, what property may be protected, which debts may be discharged, and what issues could create problems in your case.

If you are trying to decide if bankruptcy is right for you, start by learning the difference between chapter 7 and chapter 13 and consider speaking with an experienced bankruptcy lawyer before you file.

Explore More Bankruptcy Guides and Tools

Explore Bankruptcy Help by State

Browse our state guides to learn exemptions, means test rules, costs, and local procedures. Use these links to jump between states and compare your options.

- Arizona

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Maryland

- Michigan

- New York

- Nevada

- Ohio

- Oregon

- Pennsylvania

- Tennessee

- Texas

- Virginia

- Wisconsin