The Fair Debt Collection Practices Act - Understand your Rights

Learn how the Fair Debt Collection Practices Act protects you from unfair or harassing debt collection tactics.

Understanding the Fair Debt Collection Practices Act

The Fair Debt Collection Practices Act (FDCPA) is a crucial law for consumers. It protects against abusive debt collection practices. Understanding this law can empower you. Debt collectors must follow specific rules. They cannot harass or deceive you. Knowing your rights is essential.

Can bill collectors come to your house? Can they call on Sunday? These are common questions. The FDCPA provides clear answers.This guide will help you navigate debt collection. Learn what collectors can and cannot do. Protect yourself from unfair practices. Stay informed and assert your rights. The FDCPA is here to help.

What Is the Fair Debt Collection Practices Act (FDCPA)?

The Fair Debt Collection Practices Act (FDCPA) was enacted in 1977. Its goal is to protect consumers from abusive debt collection practices. It applies to personal, family, and household debts.

Under the FDCPA, collectors must adhere to ethical standards. They are prohibited from using deceptive, unfair, or abusive tactics. This promotes transparent and fair collection practices.

The FDCPA covers several types of debts. These include credit cards, mortgages, and medical bills. It does not apply to original creditors collecting their own debts.

Key protections provided by the FDCPA include:

- Restrictions on call times

- Prohibition against harassment

- Required validation of debts

Understanding the FDCPA empowers consumers. It provides legal measures to counter unfair practices. The act is a vital part of consumer protection in the U.S.

Is Bankruptcy a Good Option for You?

Take this 60-second assessment to see which options people commonly explore based on debt, income, and urgency.

About how much total debt do you have?

Who Is Protected by the FDCPA?

The FDCPA aims to safeguard consumers from harmful debt collection practices. It specifically covers individuals with personal, family, and household debts. These protections do not extend to businesses.

Consumers dealing with various debt types are protected. This includes medical bills, mortgages, and credit card debts. The act provides a framework that restricts third-party debt collectors.

However, the FDCPA does not protect all individuals. It applies only to those dealing with collection agencies or third-party collectors. Original creditors collecting their debts are not subject to the FDCPA restrictions.

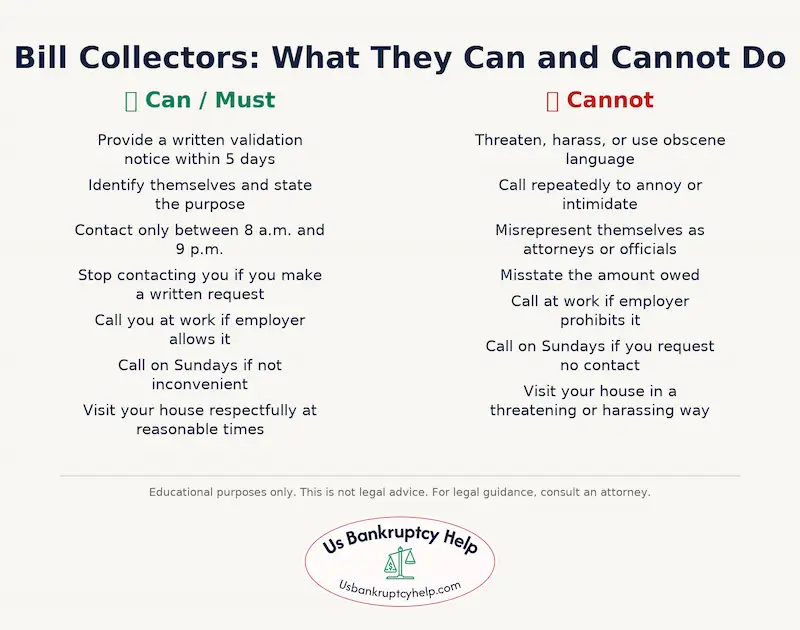

What Debt Collectors Can and Cannot Do

Debt collectors have specific guidelines they must follow when contacting you. The FDCPA prohibits the use of deceptive, unfair, or abusive tactics. Understanding these limits can help you respond appropriately.

Collectors must identify themselves and the purpose of their contact. They cannot misrepresent the amount owed or claim false affiliations. It's crucial that they provide accurate information without using misleading methods.

Harassment or abuse by collectors is not allowed. This means they cannot threaten violence or use obscene language. Furthermore, repeatedly calling to annoy or provoke you is strictly prohibited.

Here’s what debt collectors can and cannot do:

- Must Provide: Written validation notice within five days.

- Cannot: Threaten, use violence, or harass.

- Must Cease: All communication if you request in writing.

- Cannot: Misrepresent themselves as attorneys or government agents.

- Can: Contact you within specified hours unless otherwise agreed.

Knowing these rules ensures that you can assert your rights confidently. It also informs you about pursuing any necessary action against unfair practices.

When and How Debt Collectors Contact You?

Debt collectors must abide by specific communication guidelines under the FDCPA. They are allowed to call you only between 8 a.m. and 9 p.m., your local time. However, these restrictions may change if you agree to different hours.

Collectors are not allowed to contact you if it's known to be inconvenient or forbidden by your employer. That means they need to respect any boundaries you set on methods of communication. You have the right to specify when and how you wish to be contacted, provided you communicate this to them.

Understanding these rules is vital to protect your peace and privacy. Keep track of any calls or contacts you receive to ensure compliance. Missteps by collectors can be grounds for complaint or further action.

Here’s how and when they can contact you:

- Allowed: Between 8 a.m. and 9 p.m.

- Not Allowed: If inconvenient or employer disapproves.

- Respect Requests: Follow preferred methods or times.

Bankruptcy and Debt Collectors

Once a bankruptcy case is filed an automatic stay goes into place that bars bill collectors from making any contact with you whatsoever, until your case has concluded, or until the bankruptcy court gives them permission to resume collecting. In chapter 7 bankruptcy cases this protection usually concludes when a discharge is ordered by the court. However, in most chapter 7 cases the underlying debt that the bill collector was trying to collect is wiped out by this discharge order. In chapter 13 bankruptcy cases this protection ends at the end of the chapter 3 plan, or, while rare, until the court grants the collector permission to resume collections. In most chapter 13 cases a discharge is entered buy the court as well, so the underlying debt is also discharged.

Can Bill Collectors Come to Your House?

Yes, bill collectors can visit your home. However, they must adhere to respectful, non-threatening behavior. They cannot visit at inconvenient times or repeatedly.

Collectors must always identify themselves and the purpose of their visit. Any inappropriate behavior can be a violation of the FDCPA. If you feel uncomfortable, you have the right to request they leave.

- Allowed: Respectful visits at appropriate hours.

- Prohibited: Threatening or harassing visits.

Can Bill Collectors Call on Sunday?

Collectors may call on Sundays. However, it should not be at times considered inconvenient for you. You can specify Sunday as a day not to be contacted.

The FDCPA obligates them to respect your preferences. If you find such calls troublesome, inform them accordingly. Collectors must comply with your request, ensuring they contact you on suitable days.

- Allowed: Yes, if not inconvenient.

- Can Request: To exclude Sundays.

How Many Times a Day Can a Bill Collector Call?

Generally, collectors should not call you more than once a day per debt. Multiple daily calls may cross into harassment. They must respect your request to limit contacts.

If you receive excessive calls, document each instance. This documentation can assist in filing a complaint. Remember, repeated calls intended to annoy or intimidate are violations.

- Limit: Typically once per debt, per day.

- Prohibited: Repeated, harassing calls.

Can Bill Collectors Call You at Work or Call Your Job?

Collectors can call you at work unless they know your employer disallows it. If you inform them it is not allowed, they must stop. They are bound to these restrictions under the FDCPA.

You should communicate any prohibitions directly to collectors. Protecting your work privacy is your right. If they continue after being notified, it can be a breach of regulations.

- Allowed: If work allows.

- Not Allowed: If employer disapproves.

- Must Honor Requests: To cease work calls.

Your Rights Under the FDCPA

The Fair Debt Collection Practices Act provides clear protections for consumers. You have the right to be treated with respect and fairness by debt collectors. This includes being free from harassment and abuse in any form.

Collectors must inform you of the debt details within five days of initial contact. This written notice includes the amount owed, creditor's name, and your rights. If you dispute the debt, they must verify it before continuing with collections.

You also hold the right to limit or stop contact by writing a request to the collector. They must acknowledge your request and comply, except for limited circumstances. Legal avenues are available if your rights are violated.

Your key rights under the FDCPA include:

- Information: Written notice of debt within five days.

- Dispute: Challenge the debt's validity and demand verification.

- Request: Cease communication via a written request.

- Legal Action: Sue for harassment or violations.

How to Respond to Debt Collectors

Facing a debt collection call can be daunting. Your response should always be calm and informed. Knowing your rights helps in dealing with collectors effectively.

Start by verifying the legitimacy of the debt and the collector. Request a written validation notice and review it carefully. This step ensures you are not falling prey to scams.

It's wise to keep records of all communications. Document dates, times, and the content of every interaction. These records protect you if disputes arise.

You can negotiate terms if you're unable to pay in full. Propose a feasible payment plan and ensure any agreements are confirmed in writing. Remember, legal assistance is a right if you feel overwhelmed.

Key steps when responding to debt collectors:

- Verify: Request a validation notice and check details.

- Document: Keep detailed records of all interactions.

- Negotiate: Discuss and document feasible payment plans.

- Seek Help: Consider legal advice if necessary.

What to Do If a Debt Collector Violates the FDCPA

If a debt collector breaches the FDCPA, act promptly. Note every violation with detailed records. Documentation strengthens your case.

Start by contacting the debt collection agency to address the issue. Clearly state your grievances and the violations noted. Sometimes, they may rectify the situation immediately.

Should these actions not resolve the matter, escalate by filing a complaint. You can reach out to the Consumer Financial Protection Bureau (CFPB) or your state’s Attorney General's office. Legal intervention may be necessary if the violation continues unchecked.

Key steps if FDCPA is violated:

- Record Violations: Keep meticulous evidence.

- Contact Collector: Address issues directly.

- File Complaint: Involve CFPB or Attorney General.

Can You Sue a Bill Collector for Harassment?

If harassment persists, consider legal action. The FDCPA allows you to sue within one year of the violation. Legal recourse can offer both damages and emotional closure.

When deciding to sue, consult an attorney specializing in consumer rights. They will evaluate the strength of your case and guide you on proceedings. Be mindful of statutes of limitations.

Actions if considering a lawsuit:

- Consult Lawyer: Seek specialized legal advice.

- Evaluate Case: Assess evidence and situation.

- Proceed Carefully: Understand legal implications.

Additional Protections: State Laws and Other Resources

While the FDCPA provides robust protection, state laws may offer additional safeguards. These laws can vary widely, offering extra layers of consumer rights.

Apart from state laws, numerous resources exist for consumers facing aggressive debt collectors. The Consumer Financial Protection Bureau (CFPB) is a valuable resource. It provides tools and guidance to better understand and exercise your rights.

Helpful resources for additional protection:

- State Laws: Check specific protections.

- Consumer Organizations: Seek assistance and advice.

- CFPB Resources: Utilize tools and support.

Key Takeaways and Final Tips

The Fair Debt Collection Practices Act empowers you with vital protections. Understanding your rights ensures you can respond effectively to debt collectors. Knowing what is and isn’t allowed helps maintain control.

Here are essential points to remember:

- Bill collectors must respect your communication preferences.

- You can dispute debts in writing within 30 days.

- For violations, reporting to the CFPB can be fruitful.

Stay vigilant and informed to safeguard your rights. If harassment occurs, take legal action promptly. Awareness is your best tool against unfair practices. Keep informed, and you'll manage debt challenges with confidence.

FDCPA FAQs: What Bill Collectors Can and Cannot Do

What is the FDCPA and who does it protect?

The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects consumers with personal, family, or household debts from abusive, deceptive, or unfair collection practices. It generally applies to third-party debt collectors, not original creditors collecting their own debts.

What times can debt collectors call me?

Collectors may call only between 8:00 a.m. and 9:00 p.m. in your local time zone, unless you and the collector agree to different hours.

Can debt collectors call me at work?

Collectors can call at work unless they know your employer does not allow such calls or you tell them your employer prohibits it. Once informed, they must stop contacting you at work.

Can debt collectors call me on Sunday?

They may call on Sundays, but not at times that are inconvenient for you. You can request that Sundays be excluded from contact.

Can bill collectors come to my house?

Collectors may visit your home but must behave respectfully and avoid threatening or harassing conduct. Visits at unreasonable or inconvenient times, or repeated visits intended to harass, are not allowed.

What information must a collector provide after first contacting me?

Within five days of the initial communication, a collector must send a written validation notice stating the amount of the debt, the name of the creditor, and information on your right to dispute the debt.

What counts as harassment or abuse by a debt collector?

Threats of harm, obscene or abusive language, or repeated phone calls intended to annoy, abuse, or harass are prohibited.

Can a collector misrepresent who they are or the amount I owe?

No. Collectors may not claim to be attorneys or government officials if they are not, and may not misstate the amount, status, or legal consequences of a debt.

Can I make a debt collector stop contacting me?

Yes. You can send a written request asking the collector to stop contacting you. After receiving it, they may contact you only to confirm they will stop or to notify you of specific actions, such as a lawsuit.

What should I do if I believe my FDCPA rights were violated?

Document what happened and consider filing a complaint with the Consumer Financial Protection Bureau (CFPB) or your state Attorney General. You may also consider speaking with an attorney about your options.